EUR/USD alone exceeds 1,500,000 yen in unrealized loss… Can it endure until the Mercury retrograde period ends on September 5?

There are more and more stories about social lending lately, and is it a withdrawal from FX suffering from unrealized losses?

Some people might think so, but the main thing is still FX, and we are facing the market without逃げる, without running away (・_・;)

Right now, the risk-off vibe continues with a disturbing market of sharp rises and falls, so let's keep pushing forward together

Now, during this Mercury retrograde period, the market tends to be volatile, and it will end on September 5.

Mercury retrograde began on August 13, and this time the euro's independent strength and dollar weakness stood out.

In the late summer market, the Nikkei 225 continued to slide, and with the euro surging, the short position in EUR/USD that I held expanded losses further.

In reality, the euro hadn't done much yet, but I didn't expect it to exceed 1.2 based on future expectations…

Thanks to that, I have unrealized losses of over 1.5 million yen in EUR/USD

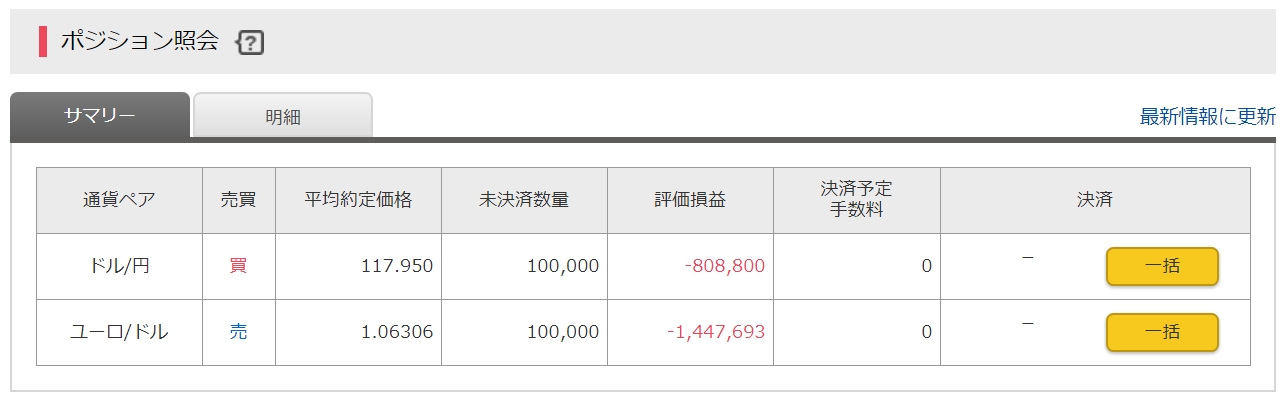

As of the screenshot, the rate was 1.195 with 10 lots held-1,447,693 yenloss.

Of course, unrealized losses exceeded 1.5 million when it went over 1.2 (I was forced to add 500,000 yen in margin) )

)

When I wrote before that EUR/USD looked like it could die, it was around -1,000,000 yen, so

the unrealized losses have grown as splendidly as that… damn it

※ The unrealized loss on USD/JPY also peaked near -960,000 yen, close to 1,000,000 yen.

Really, there aren’t many people who can endure such losses to this extent

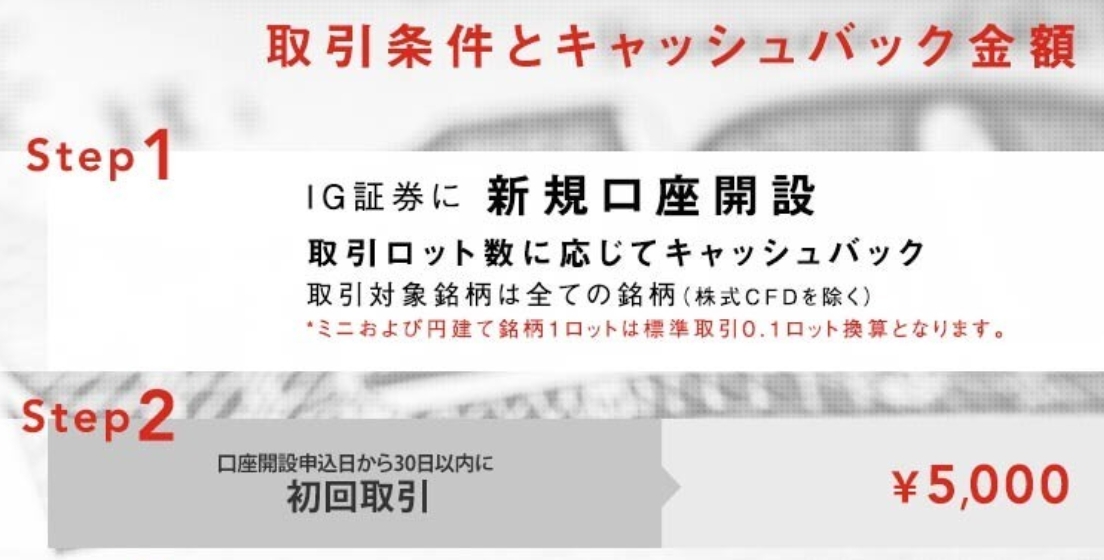

【Would you like to take advantage of a campaign in trading high-interest BRL (Brazilian real)?】

IG Securities is the only FX broker where you can trade BRL/JPY, and they are running a new account opening campaign.

The first 150 people might be interested, but since the company is minor, it should be okay

Getting 5,000 yen is worth it by itself, but I think this campaign can be stacked with a friend referral program…

If so, you could get an additional 9,500 yen through the extra referral program

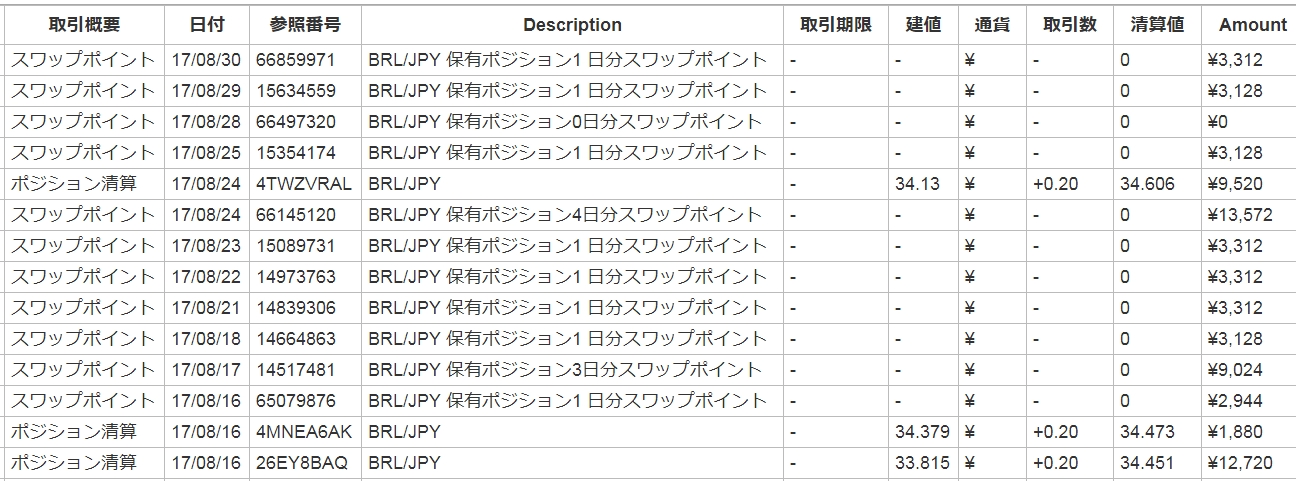

After winning the campaign, you can have a BRL dedicated account and swing with a daily swap of 92 yen

Since this year, high-interest emerging market currencies like the Turkish lira, South African rand, and BRL have all been strong.

There was a loss cut due to the real shock, but now the rate has fully recovered, and enduring the huge unrealized loss from dollar weakness is thanks to emerging market currencies (Turkey has also hit the bottom!).

BRL is really recommended, as you can get about 3,000 yen per day in swap interest and occasionally make about 10,000 yen in profit from swings.

If you want to start BRL trading and double-dip into the campaign, visit my blog

and leave a comment in the sectionwith your gender, name, and the email address registered at account opening

If you check 'Hide from administrator', comments will be anonymous and invisible to others.

Don’t miss this chance (One more person can be referred)

(One more person can be referred)

【Debt-collateralized social lending is not popular】

I complained that I liked trust lending that pays direct distributions to bank accounts, but there were few cases to invest in, so

| Return on investment (before tax) | Investment period | 募集金額 |

|---|---|---|

| 9.00% | 18 months | 40,100,000 yen |

four cases appeared at once from 8/18.

These four are essentially the same project, but the募集額 was four times larger, so it remained investable even after a few days.

…but even after more than 10 days since fundraising started, as of 8/30 only about half had been filled.

It’s unbelievable that such high demand still leaves this much unfilled in trust lending, which typically requires being glued to a PC at start time.

Splitting the same project into four parts is common in social lending (splitting the 10th issue is not unusual)

And the interest rates are also quite attractive.

However, these are now rare debt-collateralized projects.

Why are debt-collateralized projects so unpopular?

I think Trust carefully screens borrowers…

But with real estate collateral they disappear in an instant, while debt collateral remains quiet, so customers sense something and avoid it…

There seems to be no history of principal loss only in debt-collateralized deals, so I can’t gauge the true intent.

I tend to look at fundraising status and think, if it’s popular, it must be safe; if not, it might be dangerous.

Are popular listings truly safe staples?

Is investing only in instant-sell listings guaranteed to be profitable?

Someone explain it in simple terms, please

Using this points site, I issued three credit cards in about half a year

10,000 yen × 3 = 30,000 yen earned

Total accumulated: 219,000 yen earned ♪

Total accumulated: 219,000 yen earned ♪

【The highest reward rate points sitePoint Income】

(Please rewrite this part for publication to the purchaser)