A quirky talk on FRB financial regulation and odd movements in B/S

Just a somewhat nerdy topic for reference.

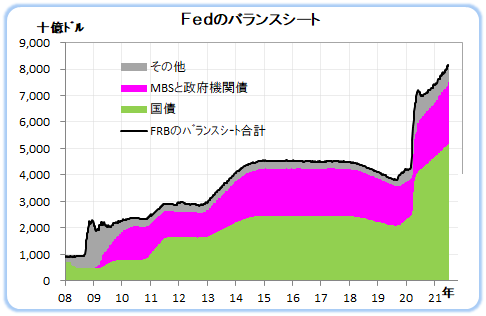

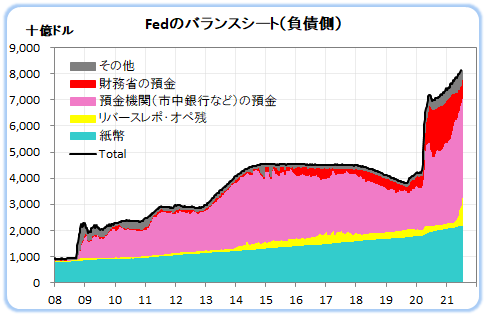

Let's look at the FRB's B/S.

Asset side movement

Liability side movement

First, since last year, the market has purchased a large amount of assets (Treasury securities and MBS) (on the asset side).

Then, the market has deposited the funds it received back through, circulating back to the FRB (on the liability side).

However, in April, reverse repos began to expand. A reverse repurchase agreement is where the FRB sells Treasuries to the market with a repurchase condition.

Isn’t that strange? The FRB buys Treasuries from the market and then sells those Treasuries back into the market. This is not trading (to profit), but something they are doing as monetary policy. If so, why buy Treasuries from the market in the first place?

The daily base over-night Treasury repo status is The weekly base of total repo is |

In other words, even if tapering is carried out, as long as the market does not misunderstand that the FRB has started to tighten monetary easing,there is no problem, is there?

Perhaps tapering could be faster than expected.