This week's forecast

A Technical View on Market Observation

Following last weekend’s rise in U.S. stocks, today’s Nikkei平均 also rebounded, but when looking at individual issues, the outcomes were mixed in terms of highs and lows.

On the Tokyo Stock Exchange Prime, the number of advancing issues was 942 and declining issues 1,139, so more stocks were in decline. While the index overall rose, in個別 (individual) names, it felt like position-squaring selling was weighing on them. This week, the Japanese market enters Golden Week; since Thursday the 29th is a holiday, effectively Golden Week begins on the 29th.

Naturally, aggressive buying is hard to come by, and the Nikkei averages oscillate driven by futures trading, but for individual stocks, actual purchases may be delayed until after Golden Week ends. In the United States, strong economic indicators continue to be released, and expectations of an economic recovery are a positive factor. In Japan, however, a state of emergency was declared, and concerns about an economic slowdown are stronger, making the situation almost opposite to the U.S. Vaccination in the U.S. is accelerating, but in Japan vaccinations are slow to progress, creating a large gap in expectations for economic normalization between the two countries. Vaccines are not produced in Japan and are supplied from the U.S. and the U.K., so slow rollout is understandable; from the perspective of foreign investment funds, such a Japanese market might presently be seen as a place to take profits.

However, the Nikkei average was 22,948 yen at the end of October last year. From there it rose, and on 2/16 this year it temporarily reached 30,714 yen. Since then, it has moved in a box pattern with ups and downs, but considering the gains since November last year, maintaining a high range with ongoing time correction is a strong development. As Golden Week approaches, expectations for major corporate earnings have cooled, and the Bank of Japan’s ETF purchase policy changes and the yen’s weakness easing are few buying catalysts, contributing to the Nikkei’s softness. From a technical perspective, the Nikkei has already fallen below the 25- and 75-day moving averages; the next downside target is the 26-week moving average. The 26-week moving average, currently rising, is in the 28,100-yen range; if the market slides again, the area around the 26-week moving average would be expected to provide support. This time around, the past rule of rising before holidays might be difficult to apply. In particular, with a fourth wave of COVID-19 infections, which is reported to be more contagious than previous strains by some statistics, early containment is in question. Cautious investing is prudent, but amid the COVID-19 era there are business opportunities and some companies will grow their earnings, so select stocks carefully. This week’s Nikkei average is expected to trade in a range centered around 29,000 yen, roughly 28,500 to 29,500 yen.

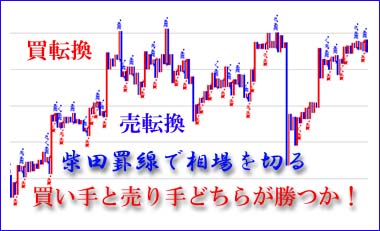

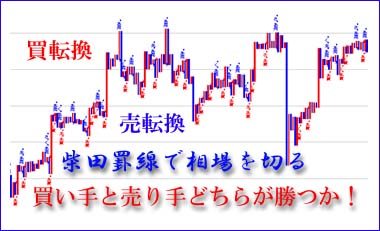

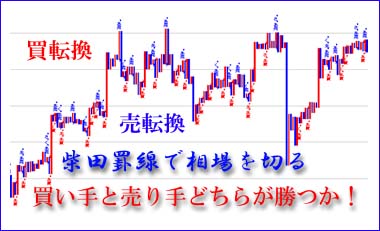

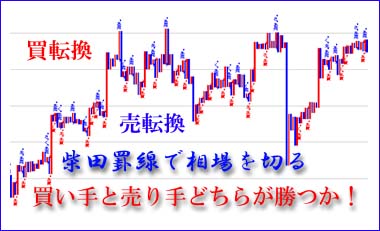

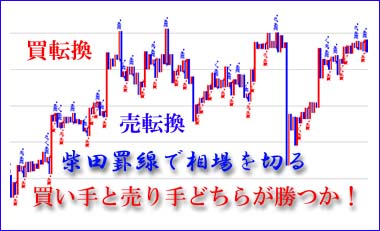

Observation from Shibata’s Kaisen (Shibata’s Technical Rules)

This week, after last week’s sharp drop and a rebound, we may see a wait‑and‑see around 29,000 yen.29000 yen ahead; in this environment, meetings discussing U.S. and Japanese monetary policy will be held, and domestic company3月期決算発表が本格化します。

27日の日銀金融政策決定会合、27~28日にFOMCがあります。FOMCではこれまでと同じように大規模金融政策を継続する方針とみられ、投資家には安心感が広がり株式にも堅調な動きが期待できます。一方、日銀には気になる動きがあると持論する市場関係者がいます。それは、日銀は4月に国債の購入を減額させており、先週の大きな下げでも21日に701億円EFTを購入しただけで相場を支える動きではありませんでした。市場関係者の間では、「日銀は金融緩和縮小に動きている」という認識が広まっているということです。新型コロナ感染拡大で景気低迷が続く日本の株式市場にとって日銀の金融緩和縮小が事実であれば痛手となります。もちろん、日銀は否定するでしょうが、カナダ中銀は来年にも利上げに踏み切る可能性を示唆しており日米欧協調による金融緩和も終りに近づいているということかもしれません。

From the chart movements, last week, the daily chart broke downward from a triangle consolidation,75-day moving average line was breached,28419 yen, and subsequently on22nd, there was a sharp rebound to29188 yen, recouping the75-day moving average line, but it has fallen below the25-day moving average line (as of22date29409 yen). Unless this level is broken above, reaching the 30,000 yen level will take time. This time, the rule of rising before holidays may be less applicable. In particular, the fourth wave of COVID-19 infections is reported to be more contagious, with some statistics indicating a doubling of infectivity in the N501Y strain, raising doubts about rapid infection containment. Investment should be慎重な stance; however, amid the pandemic there are business opportunities and some companies will grow earnings, so invest selectively. This week’s Nikkei average is expected to trade in a range around 29,000 yen, with a base around 28,500 and a ceiling around 29,500 yen.

Indicator Analysis

Nikkei Average

Last week’s forecast suggested that due to a renewed surge in COVID-19 infections, Osaka and Tokyo might issue a state of emergency within the week, which would push the chart toward the 25-day moving average (as of the 16th, 29,542 yen) and test the 75-day moving average (as of the 16th, 29,045 yen). If the 75-day moving average is breached, the adjustment could be protracted.

As U.S. stocks also fell, the Nikkei Average dropped to 28,419 yen on Wednesday, a low not seen in about a month. However, it managed to close the week around 29,020 yen, above 29,000, and did not fall below the 75-day moving average (as of the 22nd, 29,144 yen), indicating a downside break from the triangle consolidation.

Last week, negative news piled up, and on the 20th and 21st the index dropped about 1,200 yen. On the 22nd (Thursday), a rebound of 679 yen to 29,188 yen occurred, temporarily recovering the 75-day moving average (as of the 22nd, 29,144 yen). However, the 25-day moving average (as of the 22nd, 29,409 yen) stands just above, and breaking above it would be necessary for a return to the 30,000 level; this may take time. In the near term, U.S. stocks may provide support, but the Nikkei is likely to hover around 29,000 yen, waiting to see the results of the third state of emergency. The expected range is 28,500 to 29,500 yen.NY Dow

Last week’s forecast suggested that continued expectations for economic reopening and solid corporate earnings would support the market, but last week’s action softened.

April 19 (Mon) saw a savage drop in tech and growth stocks after Bitcoin’s plunge, and on April 20 (Tue) the WHO warned that global COVID infections were approaching a peak, with U.S. daily new cases exceeding 60,000, leading to a broad slide in three major indices. On the 21st (Wed), there was a brief rebound, but President Biden’s proposal to raise capital gains taxes for the wealthy caused a sharp decline. The week ended with the NY Dow bouncing to around 34,043, a gain of 227 dollars from the prior day.

This week, attention is likely to focus on tech earnings. Additionally, on the 28th, President Biden is expected to deliver his first congressional speech since taking office, with mention of infrastructure plans, climate policy, and possibly capital gains tax. It remains unlikely that taxes will rise rapidly while unemployment remains high; in the near term, solid corporate results and expectations of an economic rebound are likely to keep markets rising.Exchange Rate (USD/JPY)

<Last week the dollar weakened>

Last week, at the start of the week, the U.S. State Department placed travel bans on nearly 100 countries, boosting the dollar and weakening the yen, but Biden’s proposal to raise capital gains taxes for the wealthy reduced dollar buying and yen selling. With the Japanese government planning to declare a state of emergency, dollar selling and yen buying intensified. On April 23, the NY market saw the dollar/yen fall to as low as 107.48, and the week closed at 107.87 yen.

<This week, dollar selling moderated by growth expectations>

The FOMC will be held on April 27–28, continuing to maintain current monetary policy. While expectations that ultra-loose policy will continue linger, they also act as a factor restraining a dollar rebound. On the 28th, President Biden is expected to speak about tax increases, which is likely to limit dollar buying.