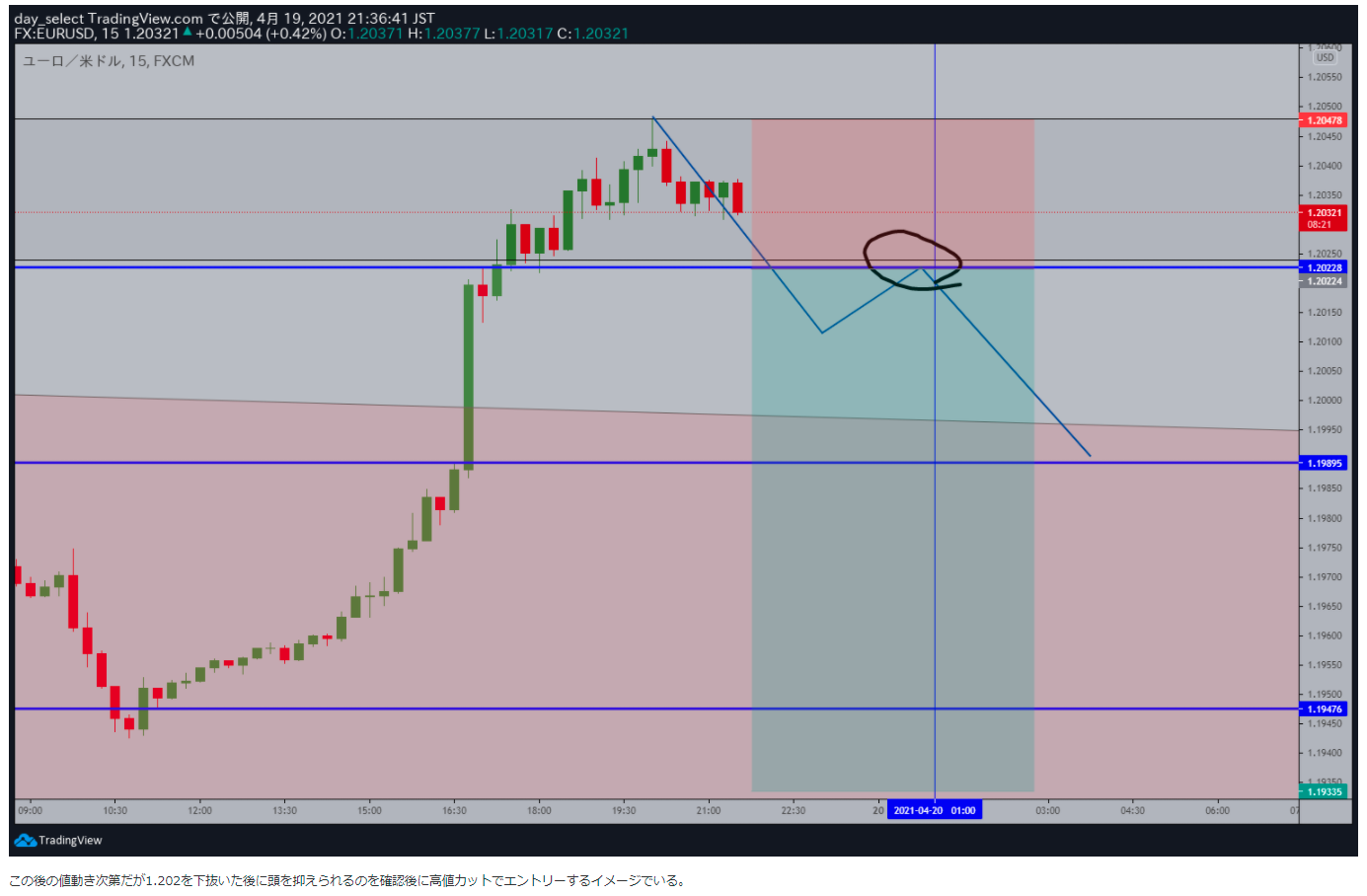

4.20 London First Half Overview and Entry Method

※This article does not indicate or recommend timing for buying or selling.

Please make your own investment decisions.

The euro has been continuing a very strong rise against the dollar and the yen.

At yesterday's London fix, there was no confirmation of a rebound in the euro-dollar from selling into the rally, so the trade was skipped.

Although pushed back by profit-taking ahead of the London fix, it was unable to push back within the range, and there were no signs of a trend reversal; since the conditions were not met, it was left undecided.

As correlations are weakening and the market is becoming more confusing, I want to organize things a bit because sticking rigidly to the current view could make the situation harder to see.

Starting with long-term interest rate declines, the dollar index has been pressured by profit-taking in USD/JPY, and now rates are being pressured lower against European currencies, especially against the euro and the pound.

In particular, the impact of the euro, which has a high weighting in the index, is strong and can be inferred from the euro-dollar chart.

Although long-term rates have been recovering recently, the dollar index is not reacting, suggesting that this is drifting away from the themes since the start of the year and requiring consideration of other factors.

In general markets, there are currently no clues about direction, and speculative players are driving sharp price moves.

As major stock components approach earnings season and stay around record highs, there is little tendency to push higher; although there is no major crash, the outlook since May has shown a lack of catalysts, so active trading has not been taking place.

This can be seen in the weak reaction even when good economic indicators are released.

As good earnings are anticipated and positions are built toward them, now that earnings season has begun, it is a time to realize profits rather than take positions, so the stock market is not leading the market and correlations with the forex market have weakened.

The differences between the EU area and Japan, which had shown similar movements, are now becoming more apparent.

Both sides struggled earlier in the year due to vaccine shortages and weakness in both the yen and euro; however, in Europe, vaccine procurement and administration are progressing well, and vaccination rates have been gradually rising recently.

In contrast, Japan has secured sufficient vaccine quantities, but vaccination rates have not risen, highlighting poor handling.

Vaccination uptake is around 1%, the lowest among advanced economies.

Europe, although initially slow to respond, reached the 10% range by the end of March, and concerns about a slowdown in economic recovery seem to have largely receded.

Japanese stocks, where vaccination progress is lagging, have now completely lost their upward momentum and are moving toward a bearish phase in the near term.

Domestic demand industries were severely affected by the state of emergency, but export-oriented companies are also facing heavier heads recently.

While tech stock prices may see renewed buying due to stay-at-home demand, they have not yet been able to support the overall market.

In the long term, vaccine disparities are expected to disappear, and the current distortions are expected to be corrected, but in the current market environment the impact is clearly evident.

From the perspective of adjusting views, I do not think it's necessary yet, but I feel that a revision of expectations is needed.

If the rate levels are changed, it is natural that you will eventually hit the target; I am reluctant to do so, but looking ahead over the next few weeks, there is a high likelihood that profit-taking has run its course and a risk-off trend may emerge,

and the dollar’s value could gradually unwind as well.

× ![]()