Cloud Bank, you know— I invested ten times the condition, and to have the reward rejected is really harsh, isn’t it?

Our investment targets are mainly FX, Nikkei 225, and crude oil, with sub-targets being gold, silver, and platinum. Recently, however, I’ve been allocating surplus funds to social lending.

Social lending is a respectable investment with annual yields around 3–10%. About a year ago, I opened accounts with “Minna no Credit” and “Lucky Bank” and invested with Lucky Bank.

※ Minna no Credit offered an extraordinarily high cashback which was very attractive, but thanks to information on 2ch, I was able to avoid investing in Minna Kure (Minna no Credit).

“Actually, Nemu-Gon once considered lending money to a Korean lending company years ago.”

I looked into it a bit now. The company name is Seoul Cosmo Holdings. For about five years after starting business, it seemed they reliably paid interest (around 8.5%), but from 2013 repayments stalled, and most investors apparently lost their funds…

At that time I hesitated to invest somewhat indifferently, and if I had invested, I would have been scammed properly.

Also, when SBI started social lending, I took an interest and watched.

At that time, I thought SBI would be trustworthy, opened an account via a point site, and took the plunge into investment.

…However, borrowers didn’t appear much, and I eventually withdrew all the invested funds.

This happened because there were few borrowers who passed SBI’s screening, leaving the lenders’ funds idle (I was one who withdrew funds because borrowers didn’t appear).Moreover, another issue at that time was that social lending involved lending to individuals rather than companies, and some borrowers couldn’t repay, leading to loan defaults.

Reference:A thorough investigation into the actual situation of SBI Social Lending loan defaults!

Looking at it this way, lending money through social lending has managed to avoid troubles quite neatly.

Investing in Korea’s consumer finance involved a vague promise from the investor who ran the operation that you would receive high interest for 3 or 5 years, plus a free Korean seaweed snack, and SBI simply earned the rewards from the point site and eventually didn’t invest and withdrew… However, thanks to that, there were no loan defaults or delays. Also, Minna no Credit earned only affiliate account-setup rewards, and I avoided risk with information on 2ch which said the investment was unreliable.

Hmmm… Could it be that, unlike FX, lending investments actually come with a lot of luck?

…when I thought that…

【CloudBank, you know— investing ten times the reward conditions should not be rejected, that would be cruel, right?】

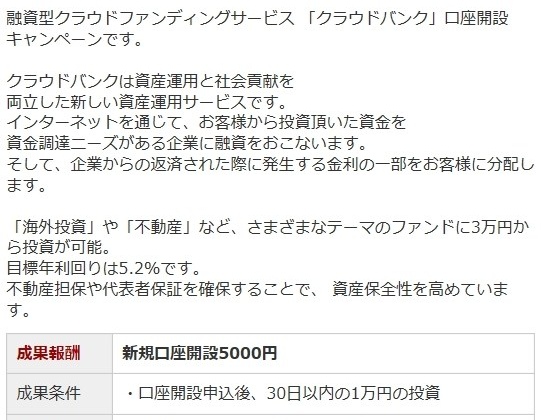

1–2 months ago, CloudBank’s project appeared on point sites and self-affiliate schemes.

I’ve always been interested in social lending, so if I could do it while earning points, of course I would go for it!

But after opening the account, the reward for investing over 10,000 yen was somehow rejected

And I invested 100,000 yen, ten times the required amount, yet was refused

This is ridiculous! I had planned to keep using Lucky Bank or Maneo for a long time in the future

Withdrawal fees were supposed to be free, and audits were passed, so I believed it would be fine

I still believe luck may overturn this for social lending, but this is not something to do, you know?

let’s prepare a point-site account for new social lending openings

If you also create a card or open an FX account, you can get rewards over 10,000 yen

【Point site Hapitas】

(Please rewrite this part for publication to the purchaser)