日経平均とドル円

0

From July up to here, my market impression is that there is no driving force in the market and no clear sense of direction.

There are frequent allocations between bonds and equities, but the movement remains at a balance, neither more nor less.

The stock market moves on future expectations to begin with, and as I have repeatedly said, it has not fallen in the second wave of the pandemic.

As a market, it has already priced this in as a matter of course, and to some extent a worsening situation is within the expected range, causing the stock market to drift accordingly.

Traditional correlations have broken down, and what to watch now and how to position oneself have become important viewpoints.

For example, the USD/JPY

Many analysts and renowned traders are looking for a downside move because, on a monthly chart, a descending triangle is currently forming, which is one reason, and

from a fundamentals perspective, the Bank of Japan’s further easing has less room than the Fed, so the absolute amount of dollars tends to increase, leading to dollar saturation and hence a relative tendency for a weaker dollar.

And as you can see, volatility is converging, and this month it is in the inside range of June’s monthly chart.

Naturally, the monthly highs and lows are watched and function as a horizontal range, so it is unlikely to deviate greatly from this range.

In other words, at this stage, it would be an imprudent strategy to long to 109 yen over about one month, and it would be hard to imagine shorting to 105 yen.

Conversely, it means you could go long near the lower bound and short near the upper bound, so taking a day-by-day approach with a range expectation and trading within that range would yield the highest performance.

◆ Nikkei Stock Average

Japan used to be called a trading nation, and its trade surplus boosted its national strength.

Naturally, this had a significant impact on stock prices.

However, in the 2000s it gradually shifted to a trade deficit, and Japan remains a trade deficit country today.

In other words, Japan now runs on domestic demand. It is driven by overseas investments that do not show up in trade figures.

Australia is a prime example of this model.

A perpetual trade deficit country, but with strong overseas investment, making the economy heavily influenced by investment.

That said, it would be erroneous to say there is no trade power left; Japan still retains international competitiveness and responds firmly to USD/JPY movements.

The main factor is believed to be Japan’s main industry, the automobile industry, though...

As I noted earlier, USD/JPY is currently in a technical and fundamental downtrend within a range.

While US stocks, China, and European stocks stay solid, they do not rise because USD/JPY is holding them back, which is one reason to consider.

What I have written so far is an analysis of the current situation, but from here is my own view.

As the author, I wonder if trying to gauge stocks using the USD/JPY pair is still valid in Japan’s current model.

In the mid to long term, there may be a slight reaction, but I think the focus will firmly shift to corporate value and price movements anchored to that.

In that sense, Japanese stocks are cheaper than world stock prices and may eventually blow away selling pressures and begin a steady rise.

※ Quote from Nikkei Shimbun

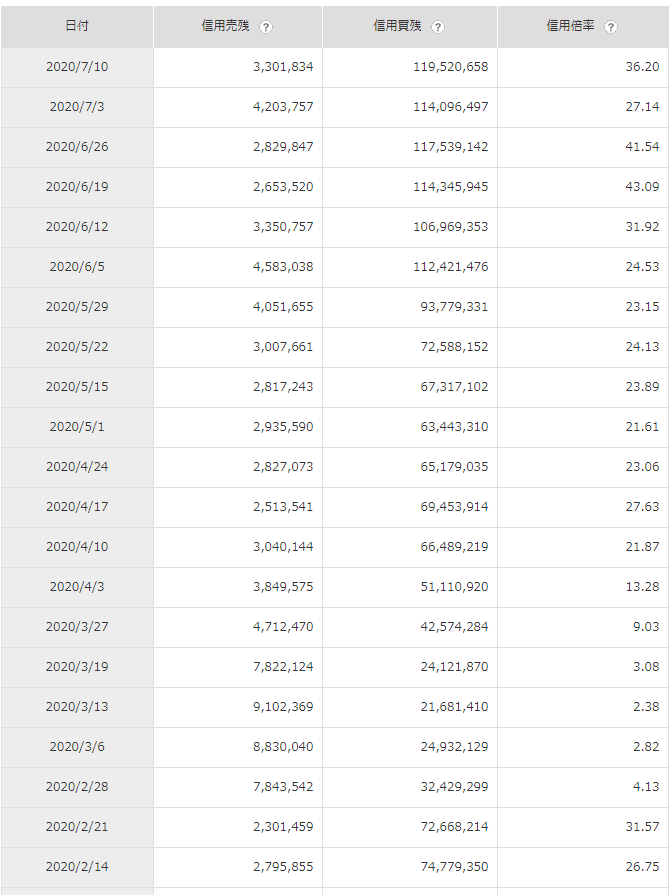

This is the balance of double inverse futures credit.

As you know, inverse ETFs are positioned to benefit when the Nikkei Average falls, and this product multiplies that effect with double leverage.

As stock prices rise, the credit long balance for double inverse has surged well beyond the coronavirus outbreak’s early days, reaching a level where a single digit change occurs in the balance.

Recently, the Nikkei Leveraged short selling ban was announced, which is due to the enormous unrealized losses among short sellers.

It is said that the Japanese mentality tends to be very negative.

While foreign stocks do not fall due to pandemic news, the Nikkei Average often reacts to declines and still responds to fundamentals.

However, in most cases, after Tokyo market closes, overseas buyers come in and prices rise the next day, which has been the recent trend.

This trend will likely continue for some time as long as we remain Japanese (a fact that cannot be changed).

Tokyo selling, foreign buying.

The Nikkei average, which is very heavy, is expected to be resolved in the not-too-distant future either by double inverses lifting off or by the usual margin selling being lifted.

Then the USD/JPY would continue to fall while the Nikkei Average would rise.

After all, stock prices and currencies are all based on value standards, and while economic conditions influence them, the absolute quantity of money, an absolute index, serves as the baseline for value.

What this means, in an extreme example, is that if Japan’s current money supply were doubled (which is extremely unlikely) and every can of juice cost 100 yen today, the value of a can would rise to 200 yen in the long run.

An increase in the money supply in the market leads to people having more money, which naturally drives goods sales.

If goods sell, gradual price increases follow as a basic principle, and the stock market follows the same logic.

The loosening of monetary policy and the way central banks around the world dumped money into the economy during the pandemic has made global stocks rise, which is the natural outcome; essentially, the value of fiat currency is decreasing, so the value of stocks rises relatively.

The same applies to minerals, with gold being particularly notable.

This has become lengthy, but I conclude that unless monetary tightening occurs, even in a recession, cheap stocks will be bought and remain resilient.

News sites and various media often compare this to Lehman Brothers, and investors waiting for a second bottom might be shorting with leverage, but I want to remind you that the current crisis began with a virus, not an economic recession, and that should be the starting point for understanding.

This is like the difference between illness and injury: economic recession is a disease that takes a long time to cure and is usually caused by structural problems, but the drop caused by a virus is more like an injury, and while the overall economy may transform, corporate strength and banks’ resilience remain, and central banks around the world will surely recover, though it may take time.

I think we will continue to hear about the bankruptcy of well-known companies.

Nevertheless, the advancement of young companies will stand out more, industry reorganization will proceed, and corporate mergers will occur, so stock prices are likely to move in a steady upward trend.

From the perspective of the end consumers, unemployment and salary cuts do not show a flood of money, but there are enormous amounts of capital among corporate shareholders and major financial institutions that directly benefit investors, which can lead to perception gaps.

I want to approach the market with as flat a mindset as possible as well.

× ![]()