Carrying on without a real business, operating on a bicycle-assembly (i.e., cash-strapped), and misappropriating funds, yet continuing to exist? Everyone's Credit

The administrative action by the Kanto Local Finance Bureau against "Minna no Credit," which operates social lending, has been decided.

(1)

Business suspension order

Suspend all operations of the financial instruments business (excluding procedures for closing customer transactions) from March 30, 2017 to April 29, 2017.

(2)

Business improvement order

1) Promptly provide customers with appropriate explanations regarding the contents of this administrative disposition.

2) Investigate the causes of the current legal violations and problematic business operations regarding investor protection, and immediately correct them.

3) Accurately grasp the status of the operation and management of assets invested by customers, and promptly explain to customers the status of operation and management of the assets they invested in, and other necessary matters.

4) Conduct customer intent confirmation, take measures to protect investors by ensuring fairness and responding in line with customers’ wishes, and promptly implement such measures.

5) Clarify responsibility, implement internal sanctions, etc., and reconstruct the internal control framework required of a financial instruments business operator.

6) Accurately understand the financial condition of the company, its parent company, and related companies, and formulate future cash flow plans for the company.

7) Report in writing within one month (and as soon as improvement measures are formulated and implemented) on the status of response and implementation from 1) to 6), and continuously report in writing on the status of execution until everything is completed.

Kanto Local Finance Bureauhttp://kantou.mof.go.jp/kinyuu/pagekthp032000621.html

“Minna no Credit,” which appeared to be operating so absurdly that a first-grade red card seemed likely, has received an unexpectedly lenient disposition…

Is this for real?

Can a business survive by not conducting operations, operating on a revolving basis, and misappropriating funds??

On March 24, 2017, the Securities and Exchange Surveillance Commission announced the disposition contents in an easy-to-understand manner, so I will explain them simply:

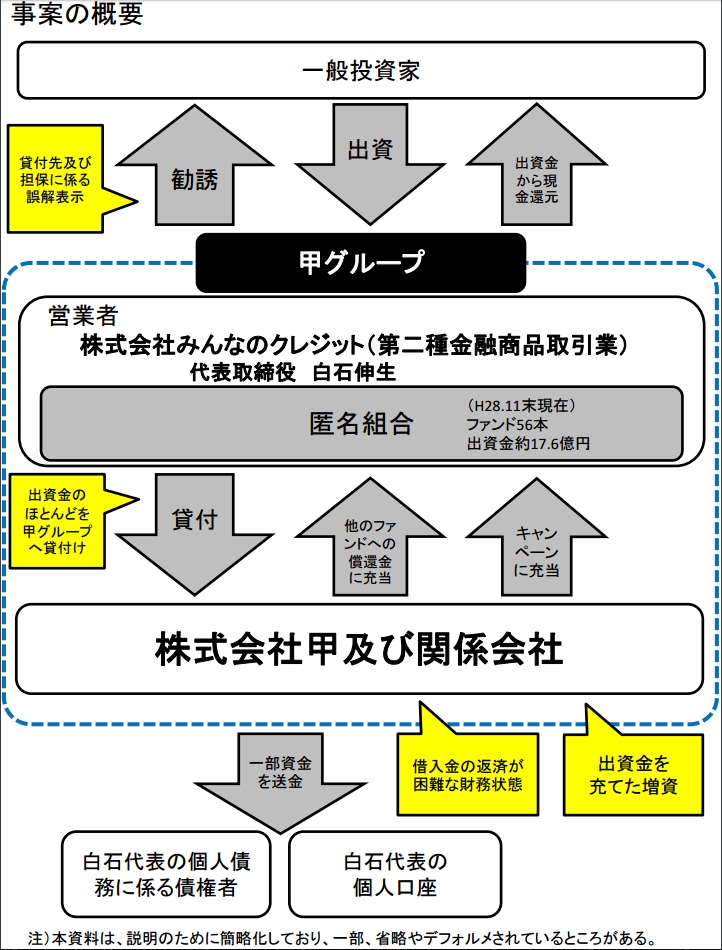

1. The fund indicated that it planned loans to multiple real estate-related companies, giving an impression that the risk of loan losses was diversified, but in reality it did not diversify and lent mainly to its parent company and related companies.2. It was stated on the website that funds borrowed from the fund would be repaid from profits from real estate businesses, but in fact funds from other bonds with later redemption dates were also being allocated.

3. Most lenders were within the company group, most collateral consisted of the company’s unpublished stock, and some loans had no collateral at all.

If the company declines, collateral loses value; there were loans with no collateral, yet it was indicated that the fund’s loan claims were secured.

5. Under the guise of a cashback campaign, cash was returned to customers, but when the source of the cash was examined, funds invested in the company were circulating back to the company and being allocated as such.

6. Representative Shiraishi instructed funds investments to be sent to his own deposit account and to his creditors; this could be considered embezzlement of funds.

8. From the end of May to the end of November in 2016, the company incurred large losses every month, increasing accumulated deficits, and from August to October of that year the company was in a state of insolvency. There were other issues as well, and loans to the company group showed a high risk of repayment delays.

I wonder if this is about right? The original source (reference) is here →Click here

Image sourcehttp://www.fsa.go.jp/sesc/news/c_2017/2017/20170324-1/01.pdf

Because the company did not proceed with the promised lending to real estate-related businesses and instead funneled money within its own group, there was no real revenue from real estate-related businesses. Therefore it operated on a revolving basis, using funds from new funds to repay existing funds. Additionally, investment funds were used for Mr. Shiraishi’s deposit account and to repay his own debts.

Even though such a severe violation occurred and the company’s assets had dropped considerably, it did not go out of business. Honestly, I was surprised.

As of March 24, the company’s website stated that Mr. Shiraishi had refunded all funds in full, but I was skeptical about its truth.

…However, rather than closing the business, the operation was only suspended for a period, which might mean that the full amount of misused funds was returned at least temporarily?

Not yet completely reassuring, but for those who invested, perhaps they could take a breath.

Questions about the audit

Minna no Credit was audited in December of last year, and on December 14, the Securities and Exchange Surveillance Commission announced that an inspection was underway. Looking at this, investors who had been watching for a few weeks to a month wondered what kind of disposition would be decided. However, even in the following month and the month after that, no disposition was made. Seeing this, I think some people reopened their investments thinking there were no problems.

Although returns from cashback campaigns are not much different from other social lending platforms, the cashback offered at the same time as investment was too attractive... If funds were to be called, a bonus might be paid, but with Minna no Credit, thousands of cashbacks were provided immediately at the same time as investment. Since the audit also finished without issue, it seemed there were investors who felt safe and invested more.

Even if the audit takes longer to reach a disposition, shouldn’t there have been some note like "audit ongoing" or "discussions with the representative"?

[Note]

Minna no Credit was also a high-value project on point sites. However, I, the moderator, applied through self-affiliate.

Because point sites award points upon completion of investment, while self-affiliates offer points simply for applying, I chose the latter. Nemuron knew that Shiraishi, the representative, had previously started several companies and that many of them failed, so I participated only in the option that granted points for simply applying. Of course, the rewards were lower than those conditional on investment completion, but it was a good decision. I have invested in social lending through Luckin Bank (also via self-affiliate) to some extent and Maneo (also getting Campaign from Click Securities).

I have invested in social lending through Luckin Bank (also via self-affiliate) to some extent and Maneo (also getting Campaign from Click Securities).

By the way, although Minna no Credit is the main topic, Cloud Bank has undergone its second audit, and Luckin Bank also faced an audit.

Luckin Bank showed changes in descriptions in projects after this audit.Well, unlike Minna no Credit, it should be okay, right?

Please replace this part for disclosure to the purchaser