A company right after going public requires meticulous attention. How to identify risky companies learned from MTG

MTG, which manufactures and sells products such as SIXPAD, posted a net loss of 26.7 billion yen for the fiscal year ended 2019.

The company had just been listed on the Tokyo Stock Exchange Mothers market in July 2018, but it immediately announced a substantial downward revision.Its stock price fell by nearly 90% from the public offering price, deceiving investors’ expectations.

IPOs are a structure that tends to disadvantage general investors

In this way,great care must be taken with companies right after listing. The reason is thatthe IPO mechanism tends to disadvantage general investors.

Why does this happen? It becomes clear when you consider the perspective of founders and venture capitalists (VCs) who invested before the listing.

They can obtain a huge amount of funds by selling their shares at the listing. In other words, their past efforts are rewarded here.

If they want to maximize profit, founders and VCs havean incentive to list at as high a price as possible. Therefore,before listing they tend to improve performance a bit and tell rosy stories about the future.

Thus, many general investors dream about IPOs and buy shares.

On the other hand, once they have sold their shares, they lose interest in subsequent stock prices.It is not uncommon for companies and managers to reach a state of “listing-goal,” where they are satisfied merely by going public.

After listing, stock prices rise more than warranted, and if performance falters, they can only fall. In this way,a large number of companies experience continued stock-price declines after listing.

The most legitimate-form of misconduct is “false accounting”

Companies that push hard at listing eventually get exposed. MTG is a clear example.

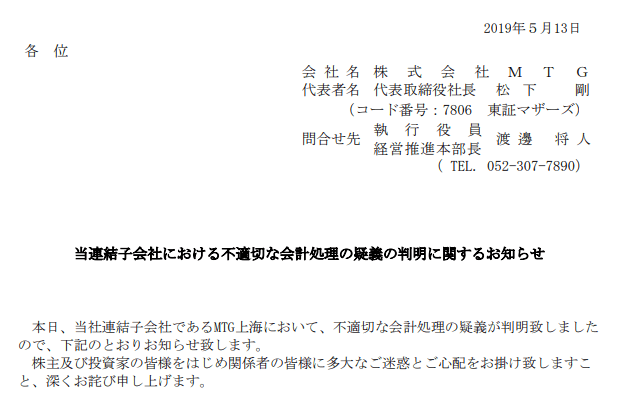

The most dangerous act is fraudulent accounting. On May 13, 2019, less than a year after listing, a press release regarding improper accounting was announced.

To summarize the content briefly, it claimed that simply bringing products into a warehouse in China was recorded as “sales.” This alone does not constitute sales. The products remained in the warehouse, and if not sold, they would come back, and of course no money would come in.

This is “fictitious sales” and a common method used in fraudulent accounting. The aim is to make performance look better, and while the auditing firm (Deloitte Tohmatsu) bears some fault for not detecting it, the company is also highly culpable.

Because the intention to deceive investors is clear,if you encounter such a stock, sell immediately. This is because further bad information is highly likely to come in.

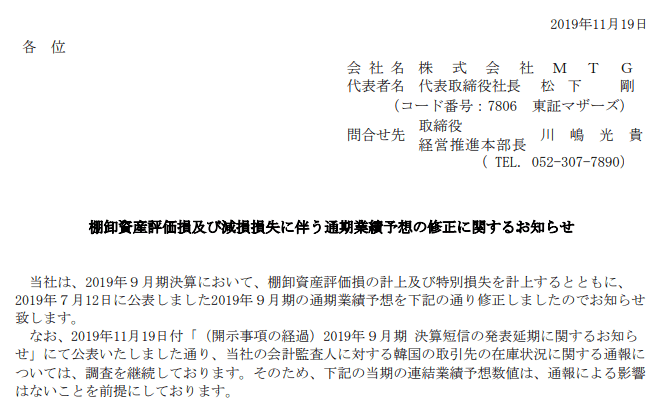

In MTG’s case, even six months after the accounting fraud was disclosed, the company posted a huge net loss again in the form of “inventory valuation losses.”It was natural that goods could not be sold remained in the warehouse.

Reasons to avoid companies with negative “operating cash flow”

Even without fraudulent accounting, this kind of case is not rare in companies. How should investors tell the difference?

If you look at the details of the financial statements, a seasoned reader will spot it, but for others it is difficult. Pay attention to“cash flow”.

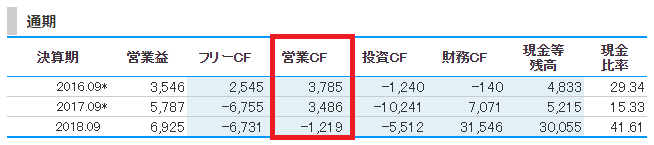

In MTG’s case, in the fiscal year ended September 2018 (before the fraud was revealed),operating cash flow was negative. Even though profits were in the black, operating cash flow was negative, which meansactual cash inflow was not there.

On the other hand,cash flow cannot be manipulated. How much cash is in the treasury is obvious to anyone. Negative operating cash flow means continuing operations will consume cash.

Of course there are exceptions. However,truly good companies undoubtedly increase their money. After all, a company’s ultimate goal is to increase money.

Therefore,beginners should avoid companies with negative operating cash flow.

What matters is the sustainability of the business model

That said, we don’t immediately grasp every number and invest. The core of the analysis is the “business model”.

When evaluating a company, always understand“how does this company make money”. You can see that the revenue sources are the beauty product brands “ReFa” and the aforementioned “SIXPAD.”

In particular, when I looked at SIXPAD, it reminded me of a past fad. Yes,the abdominal device that makes your stomach shake—the “Ab-Tronic”.

I recall it being popular when I was in middle school. I wondered, “will this really build muscle?” butthe boom soon faded.

Therefore I did not consider investing in SIXPAD as a major productbecause I judged the business model lacked sustainability.

Such “fad items” eventually see the boom fade and leave massive inventories, rapidly triggering a management crisis. MTG is a prime example of this.

While riding the boom may temporarily push stock prices up, buying at that price issimply a game of who ends up with the last laugh. At minimum, it is not desirable for long-term investing.

You should first learn to identify dangerous companies and protect your hard-earned money.