Translate the following HTML to English, keep the HTML as is, do not use markdown or insert line breaks, and decode entities before translating: WeWorkで問題噴出のソフトバンクGは売り?買い?バリュー株投資家に求められる「ドM気質」 >

SoftBank is a “Investment Company”

When people hear “SoftBank,” they may think of a mobile phone carrier. However, the subsidiary mobile carrier is listed, and the parent company mainly engages in“investment business”.

In 2017, SoftBank launched the ¥10 trillion“SoftBank Vision Fund”, and the second fund has already been announced. It is carrying out investments at a national-budget scale.

In the fund, by investing in promising IT ventures, they plan future returns from exits. The trigger for Masayoshi Son’s passion is thought to beinvestments in Alibaba in China. An investment of 200 million yen swelled to 5 trillion yen, becoming 2,500 times at IPO.

Additionally, there are success stories such as ride-hailing company Uber. With repeated investment successes, they are aiming to build a “SoftBank Empire” that spans the globe.

Concerns about the Vision Fund

However, as the situation with one of its investments, WeWork, came to light, doubts among investors arose: Is the Vision Fund really okay?The stock price fell sharply.

In such times, investors should coolly research other potential investments. Here are SoftBank’s earnings presentation materials.

“ByteDance” runs the video app TikTok, while DiDi and Grab are the Chinese and Southeast Asian equivalents of Uber, respectively.WeWork was an important investmentin that context.

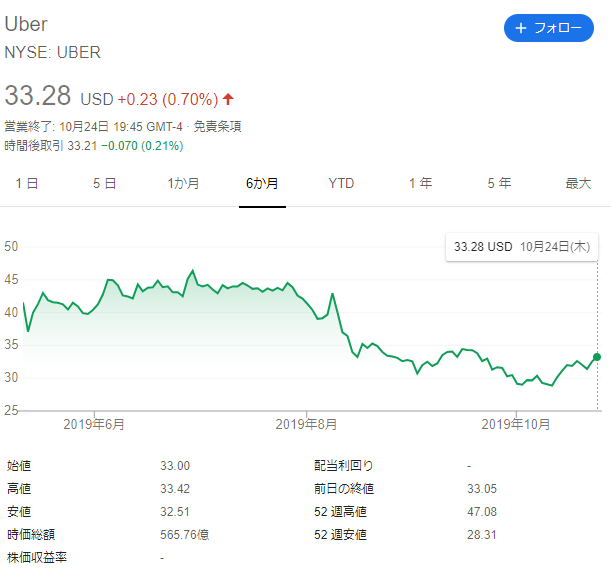

Uber has gone public, butit continues to lose money and its stock price has fallen. The trajectory here will likely impact DiDi and Grab as well in a big way.

Also, ByteDance’s TikTok has enormous momentum, but questions remain about whether the boom will stabilize and how it will monetize.

Looking at these circumstances,the Vision Fund does not appear to be rock-solidas an investment.

Moreover, investing in unlisted companies often requires that one good company among many explodes in growth to secure any return.That thrill may be irresistible for risk-taker Son.

As an investor, I do not rate the Vision Fund highly. That is because there are many uncertainties and the contents are not well understood(r66).

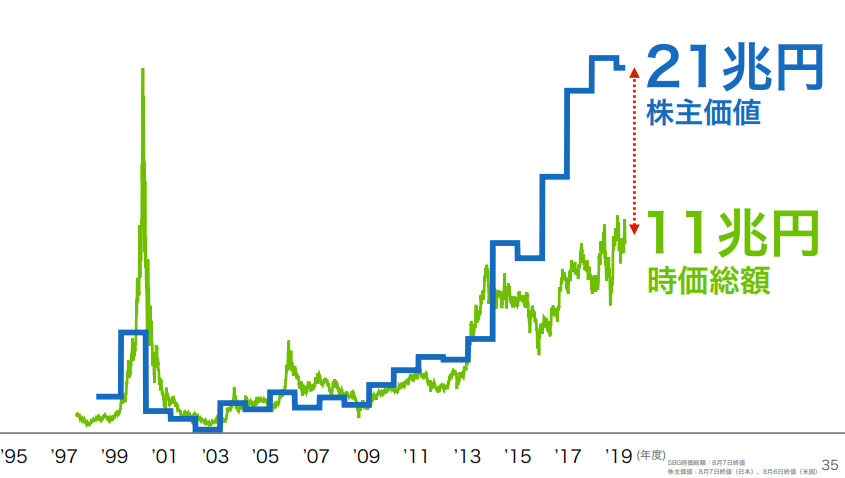

21 trillion yen of equity can be bought for 8 trillion yen

So, is SoftBank Group a sell? That’s another question.

Looking at the disclosed materials,there are statements attractive to value investors. The most prominent is the following slide.

The intrinsic value is ¥21 trillion, while the market capitalization is ¥11 trillion (recently dropped to ¥8 trillion). This is exactly the embodiment of the value investing principle of“buying a 1,000-yen bill for 500 yen”.

Here, shareholder value refers tothe market value of the held shares.

Alibaba is 11.3 trillion yen, SoftBank (the mobile carrier) is 4.7 trillion yen, among others. Subtracting the 5 trillion yen of “net debt” yields the 21 trillion yen of “shareholder value.”

Among them, the Vision Fund is 35 million yen, not particularly large.From a value perspective, the Vision Fund’s movements are not very relevant.

Therefore,even if the Vision Fund fails, SoftBank’s “value” is not easily undermined.

Is 17 trillion yen of interest-bearing debt excessive?

SoftBank is said to have a lot of interest-bearing debt.

Indeed, 17 trillion yen is on a consolidated basis, but about 10 trillion yen of that is from Sprint and SoftBank (the mobile carrier). These companies generate stable internal cash flow, so they have little impact on the parent’s funding condition.

Incidentally, Sprint will merge with T-Mobile and be excluded from SoftBank’s consolidated group.

At least,compared with when we bought Vodafone, there was clearly more room, with less risky financing.

Interest rates are significantly lower than before, and the company continues to expand by leveraging the low-rate environment.

If the fund itself does not undertake forced investments,the financial problems are not necessarily large. (Note: Investors worry that WeWork’s investment came from the main company.)

How far will the stock price fall?

So, is SoftBank Group a buy? In the short to medium term, there is substantial downside potential.

This is becausemore failed cases like WeWork are likely to emerge.

Even Masayoshi Son cannot have all investments succeed. Moreover, investments in unlisted companies are more prone to failure.

In recent years of abundant capital, the market for unlisted stocks rose. Vision Fund investments occurred in this period, sothere’s a high possibility of having bought at high prices and without substantial fundamentals.

What happens after a bubble is its burst.

If that occurs, stock prices will drop significantly. Moreover, this will not be mere headline risk;through the Vision Fund’s impairment, the results can also swing to a loss.

In fact,half of current operating profit is earned from the Vision Fund’s “unrealized gains”. Since these are not realized gains, the market trend could reverse completely.

Moreover, the unlisted stock bubble and stock market plunge tend to occur in similar timings. Most assets are listed shares, so if the market crashes,the value of the main company will inevitably be significantly affected.

Thus, SoftBank Group’s stock could fall endlessly, in theory.A stock that could keep falling without bound.

The “M” mindset required for value investors

However, this is a story about stock prices.Falling stock price does not mean management is in danger. The mobile carrier is solid, and Alibaba has established a solid position in China.

Moreover, if even one company within the Vision Fund achieves great success, it can generate large returns.

If you buy now,by the next economic cycle (about 10 years), you are likely to be in positive territory, in my view.

However, given the nature of this company,you will be repeatedly unsettled by various bad news and stock declines while you hold it. Each time, you will be forced to decide whether to sell.

Of course, true value investors would hold on, and if possible, muster the nerve to average down.When there is no major problem with the substance and the stock price falls, that only increases its appeal.

“Hit it harder! And let the stock price fall further!”

Value investors need that“M-mindset”.

If you can identify the bottom of the stock price, that is ideal. Yet, like many, including me, it is difficult, which is why you shouldkeep tight control of your funds, buy as cheaply as possible, and welcome price declines.

Can you do that?If you can answer “yes,” your future as a value investor looks bright.

★I’m posting useful videos on YouTube! Please subscribe to my channel★