Can JBR (2453) become an overwhelmingly formidable presence that troubleshoots so effectively that no one dares approach? A sense of undervaluation lingers in the stock price.

This summer I personally had a lot going on around my home.

There were updates for termite prevention (every five years), air conditioner failures and repairs, and even a power outage caused by Typhoon No. 15.

In particular,I was overwhelmed by the air conditioner failure. It happened during a sudden heatwave, so even if I contacted the manufacturer, they couldn’t come right away, and I had a hard time finding a repair company. In moments like this I sincerely wished for a place where I could say, “If you contact us here, you’ll be fine.”

Actually, a major listed company that offers such a service isJapan Best Rescue System (JBR) (2453).

A subscription for “peace of mind”

The company operates a call center and, by coordinating with service providers nationwide, it builds a business model around addressing customers’ “troubles.”“Life Ambulance”“Water Ambulance“Student Life 110”

Leading the results is the “membership business.”

For example,when renting a residence, paying a guarantee fee in advance allows JBR to respond to key or water-related troubles for free.

For tenants, that provides peace of mind, and for JBR it offers a stable income stream. If no troubles arise, the guarantee fee remains profit,taking advantage of the trendy “subscription” model.

Can we create something worthy of saying, “This is where you go for trouble resolution!”

The heart of this business ishow broadly the network can be expanded. A network consists ofthe collaboration with the intermediary companies andthe securing of contractors who actually perform the work.

Intermediaries include real estate companies, home builders, and university co-ops. They provide warranties at the time of rent contracts, home purchases, or when students move to Tokyo for university admission.The more partner companies there are, the greater the opportunity to acquire customers.

However, recentlythe partnership with Docomo has been terminated, so it isn’t all smooth sailing. The benefit as an intermediary isn’t that clear-cut.

Contractors arelocal sole proprietors and small to medium-sized enterprises. For JBR, the key is how broadly and how high-quality a network can be assembled. Based on online reputations, the current impression is a mix of both good and mediocre.

The issue isthat there are no barriers to entry in this business. It’s just having a call center, so anyone can imitate the same business. For example, if a major real estate company starts doing the same, they would become a formidable rival.

To prevent that,they must raise the network and service quality to confidently say, “This is where you go for trouble resolution!”but it doesn’t seem they’ve reached that position yet.

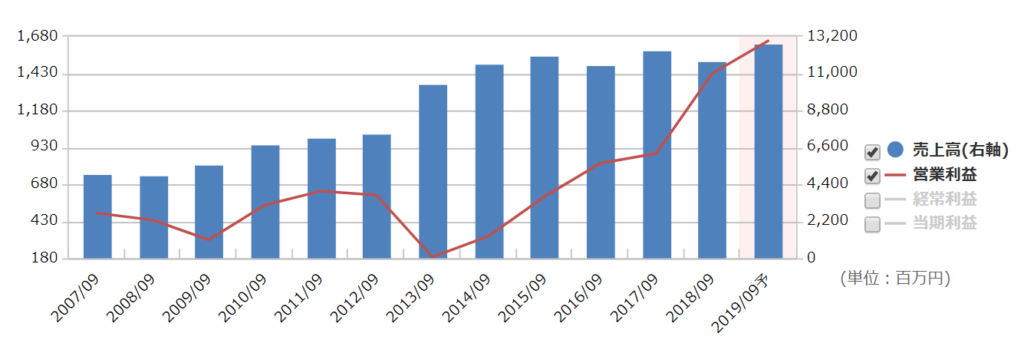

Growth potential is reasonably priced, but not yet absolute

Looking at the stock price,it has recently been weak.

However, the earnings aren’t bad. Growth is still continuing, and with a P/E around 20,it appears somewhat undervalued. Depending on the price, it could be worth considering. Of course, the business must be performing well as a prerequisite.

Can they build an overwhelmingly powerful business that no one can catch up to?I’d like to keep an eye on the direction from here.