Will ¥2 trillion in "goodwill" weigh on JT (2914)? Assessing signs of potential dividend cut

Article about JT (2914)I posted this, and received valuable feedback from the renowned investor Invesdoctor.

It would have been a good article if it had touched on the finances.

Will JT bottom out? Finally a dividend yield of about 7%... There is value in disliked stocks = Shunji Kibo | Money Voicemag2.com/p/money/757761

That’s right; the previous article did not touch on finances. This is certainly one of the factors driving the stock price down.

“Goodwill” Is a Minefield that Can Cause Sudden Losses

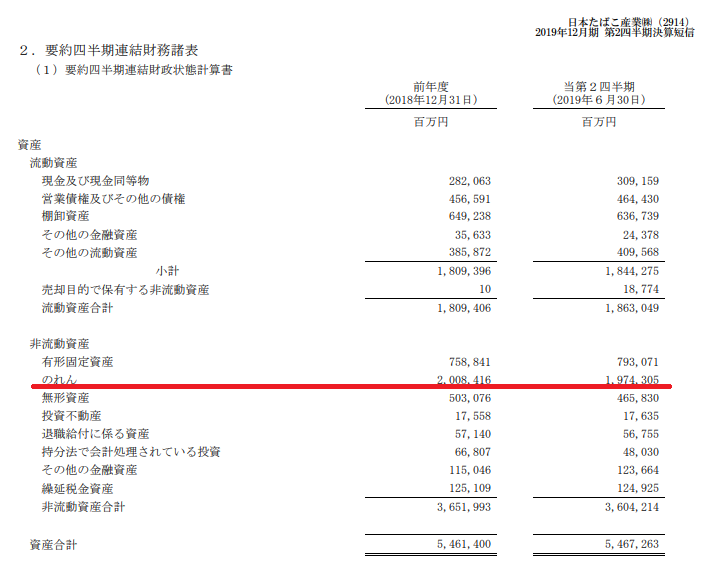

Investors are particularly concerned about “goodwill.” Looking at the financial statements, there is about 2 trillion yen in goodwill.

Goodwill is the item that arises when a company is acquired. If a company is bought for more than its net assets,the excess paid is recorded as goodwill.

For example, if net assets are 10 billion yen and the purchase price is 20 billion yen, 10 billion yen (20 − 10) becomes goodwill.

Because it is something you overpaid for, under Japanese accounting standards it has typically been amortized over 20 years as an expense. If goodwill is 10 billion yen, it would be expensed as 0.5 billion yen per year (10 billion ÷ 20).

However,by adopting International Financial Reporting Standards (IFRS), goodwill no longer needs to be amortized periodically. JT has been using IFRS since 2011. With IFRS, companies can inflate profits compared to traditional standards.

On the other hand,IFRS requires testing for impairment at each reporting period and recognizing losses when goodwill is deemed to have no value.

In the above example,if you decide goodwill is only worth 5 billion yen, you would record a 5 billion yen impairment loss. From shareholders’ perspective, this could cause a panic sell. Many investors fear this possibility.

Reasons Why JT Is Less Likely to Suffer a Large Goodwill Impairment

Impairment testing uses the “discounted cash flow method,” which discounts expected future cash flows to present value and sums them up.

…That sounds hard, sothe gist is that if the acquired business stops being profitable, impairment occurs. In JT’s case, because the potential impairment could reach up to 2 trillion yen, investors are wary.

In short, to gauge goodwill impairment, you need to judge whether the acquired business is performing well or not.

So, where did JT’s goodwill originate? It’s fromacquisitions of overseas tobacco companies. The largest ones are 1999’s R.J. Reynolds America (U.S. external business), 2007’s Gallaher (UK), and 2016’s American Spirit (U.S.).

That is,if overseas operations deteriorate, impairment risk rises; otherwise not much to worry about.

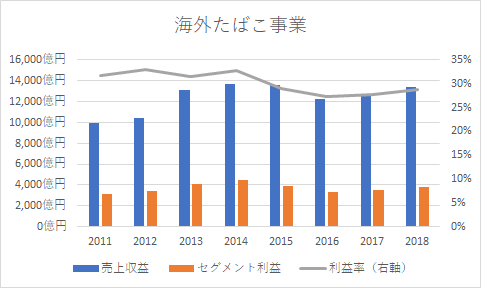

Next, let’s look at JT’s overseas operating performance.

Not showing strong growth, but relatively stable trend. Profit, which had been on a downward trend, has increased in the most recent three years.

Tobacco businesses are stable globally. Regardless of whether it is good or bad, there is addiction, and once someone has it, it’s hard to quit.

Smokers in developed nations are decreasing, but price increases can offset that.Heavy smokers will continue smoking even if a pack costs 1,000 yen.

For non-smokers, higher prices reducing smoking rates is welcome, and price increases are often implemented alongside tax hikes, so government revenue does not decrease. In other words,price increases are welcomed by many stakeholders.

In this way,the stability of the tobacco business is maintained and the risk of large goodwill impairment is low.

No signs of reduced dividends at this time—shareholders must stay vigilant

I’m not saying goodwill impairment risk is zero. The future is unpredictable in business.

However,even if all 2 trillion yen of goodwill were impaired, it would not lead to a crisis.

JT has 2.7 trillion yen in capital. Even with a 2 trillion yen loss, it would not become insolvent and would still have capital to spare.

Goodwill impairment does not involve cash outflow. Therefore,there is no direct impact on dividends. The dividend source (retained earnings) has room, and JT can continue to pay dividends steadily from 400 billion yen of operating cash flow.

That said, impairment would only become necessary if performance deteriorates.If performance worsens, the above assumptions will be undermined.

Therefore,shareholders must diligently monitor performance and stay alert for signs of deterioration.

What I can say at present is that there are no signs of impairment or deterioration in performance. If cash flow remains stable, the likelihood of a cut in dividends is low, and the Ministry of Finance, which holds 37.6% of the stock, is unlikely to approve a dividend cut.

As an investment for dividends, it is not bad at all.

There is no single correct answer in investing. In this context,the skill required of an investor is to take actions that, based on the information available now, seem somewhat advantageous. Please learn more about the company and enhance that skill.