How far will JT (2914) keep falling? What "The Future of Stock Investing" can teach us

JT (2914) stock price is falling.

The current dividend yield is about 7%which is a level rarely seen in Japanese stocks.

Most holders probably bought for dividend income. Even if bought at 3,000 yen, the yield was over 5%. It has fallen to 2,200 yen, which is painful.

With the stock price so low, you would think the business performance must be poor, but that is not the case. Operating profit, while not at its peak, has remained at about 80% of it.The most recent first half was actually an increase in profits.

Causes of the stock price decline

So why has the stock price fallen so much? I think there are three factors.

Future of the tobacco business

It is clear that the tobacco business is not a growth industry. Smoking rates in advanced countries are certainly decreasing. Especially in recent Japan, as the Olympics approach, the movement to quit smoking is growing stronger.

In Tokyo, passive smoking prevention ordinances have tightened smoking rules and separation in eateries. Other municipalities and the country may follow. At a time when smoking rates are already declining, this adds pressure.

Lagging behind in heated tobacco

What offered a ray of hope was “heated tobacco.” It is said to have fewer adverse effects on users and those around them compared to combustible cigarettes. Philip Morris’s “iQOS” sparked the boom.

However, JT has lagged behind this trend.While iQOS has a market share of over 70%, JT’s “Ploom Tech” is only about 8%. Development has been slower than expected, and investors are growing frustrated.

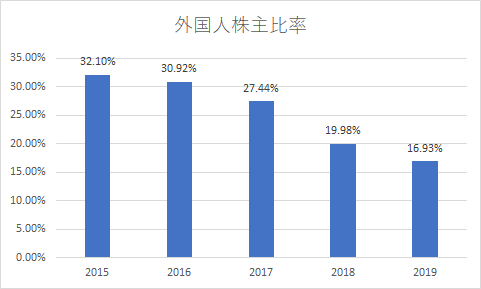

Global ESG investment trend

A major current in the global asset management industry isESG investing. ESG investing excludes companies that do not align with Environment, Society, and Governance on ethical grounds.

Whether this is economically rational is another matter, but JT, which develops tobacco business, falls under the S (Society) andfaces selling pressure from foreign institutional investors.

What good cash flow supports

How far will JT’s stock price fall?

One thing that can be said with certainty is, “There is no stock that keeps falling forever.” The only time it could go to zero is if the company goes bankrupt, butJT is far from bankruptcy.

That can be said because the company’s cash flow tells the story.

JT generates an average ofabout 400 billion yen in operating cash flow each year, and uses this for dividends and acquisitions in emerging markets. If things get bad, they simply cut spending, and money steadily accumulates.

Tobacco is a regulated industry in every country,with little competition. Therefore, it can continue to generate stable and high profits.JT’s operating profit margin has stayed around 25% and is stable.

Even if demand decreases, profits might seem to drop, but that is not the case. People will continue to buy tobacco no matter the price, soeven if sales volume decreases, price increases can sufficiently cover revenue declines.

Cash flow also serves as the source for many investors’ dividends. The current total dividend is about 260 billion yen, with a buffer of nearly 70% of operating cash flow. Even if the company does not grow,maintaining current cash flow can avoid dividend cuts.

With a 7% dividend, after-tax compounding would recover the cost in 13 years. In other words,if you hold for 13 years without cutting the dividend, you can fully recoup the stock price at that time.

There is a charm in disliked stocks. What The Future for Stock Investing teaches

In fact, tobacco stocks have been sold off before for similar reasons.

At listing, they were shunned by investors compared with NTT or JR because the outlook seemed bleak.The only negative initial public offering allocation rate in privatization ever recorded.

if you had held on and reinvested dividends, the annual return from 1953 to 2003 was 19.8%. This is an astronomical number—100万円 growing to 83百万円 over 50 years.

Philip Morris’s case is described in detail in the long-term investing classic “The Future for Stock Investing.” If you haven’t read it yet, please do.

According to the book, the traits of stocks that deliver returns over the very long term are “companies that do not go bankrupt and are “undervalued because they are disliked by the public.” By holding such companies and “reinvesting dividends,” you can achieve high long-term returns.

This is exactly the current situation with JT, isn’t it? The likelihood of bankruptcy is extremely low, ESG investing dislikes it and it is undervalued (PER 11x), while still offering high dividends (yield around 7%).

Therefore, the role of holders is topersistently reinvest dividends without being swayed by stock price fluctuations. If the price keeps falling, holding for 13 years would still break even.I don’t think it’s a bad investment.

Of course, it’s possible the book’s described phenomena happened to occur by chance. That’s whyconsidering various possibilities and stepping into areas that seem somewhat advantageous is the investor’s duty.