Yasuda Warehouse (9324) has assets worth less than half of its actual value!? Analyzing the "asset value stocks" catching attention due to Uniho's surge

Uni-Zoo HD (3258) surged on takeover chatter and drew attention to “undervalued assets stocks.”

Uni-Zoo HD was targeted for acquisition because the assets it holds (real estate) were trading far below intrinsic value. Before HIS’s TOB announcement, in rough terms, it was300 billion yen worth of real estate could be bought for 60 billion yen.

If you acquired such a company, regardless of whether you sold the real estate, you could essentially make a “huge profit.”There is no doubt funds would eye this.

Warehousing companies rank high in “implied PBR” undervaluation

A metric showing undervaluation relative to assets held isPBR, which is based on book value—that is, the price paid when purchased. For real estate, the appreciation after purchase is not reflected in the PBR.

The appreciation not reflected in book value is called “unrealized gains,” and the PBR that reflects these is called the “real PBR.” The smaller the real PBR, the cheaper it is considered.

Below, since Rakuten Securities had a real PBR ranking, we list it.

(Rakuten Securities)

In this ranking, the warehousing companies stand out. Led by No. 1 Yasuda Warehouse (9324), followed by Shibusawa Warehouse (9304), Mitsui Warehousing HD (9302), Mitsubishi Warehouse (9301), and Sumitomo Warehouse (9303).

The business models of these companies are very similar.They own warehouses and run logistics businesses while also owning central-city real estate for rent. And most of their profits come from the real estate business.

Each company has a long history, and their real estate business dates back a long time. For properties owned for a long time, especially in the city center, even after the bubble burst, there remain substantial unrealized gains.

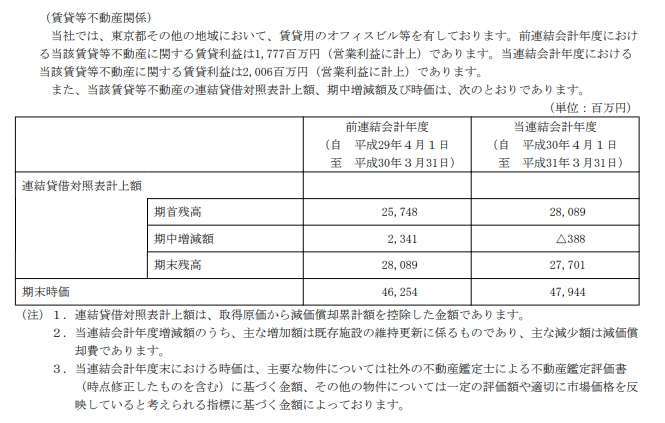

Real estate and stock worth 68 billion yen are being sold for 27 billion yen

Yasuda Warehouse, ranked No. 1has a fair value of 27 billion yen for rental real estate on the books, while the market value is 47 billion yen, meaninga unrealized gain of 20 billion yen.

Furthermore, there are 42 billion yen in investment securities (including 33 billion yen in Hulic stock), and 7 billion yen in cash and deposits, soeven without impairment, these assets alone would amount to 960 billion yen (470 + 420 + 70).

After subtracting 28 billion yen in interest-bearing debt,“real net assets” are 68 billion yen.

Checking Yasuda Warehouse’s market capitalization at the time of writing (August 21, 2019) shows27 billion yen.

Assets worth 68 billion yen are being sold for 27 billion yen— Yasuda Warehouse is currently this undervalued.

Acquisitions like Uni-Zoo’s are unlikely to spark a catalyst

So, even if you bought Yasuda Warehouse now, can you be sure the stock price will rise? Not necessarily.Even if price is cheap, if there are no buyers, trading price will not rise.

A phenomenon where the price remains low despite undervaluation is called avalue trap.

In Uni-Zoo HD’s case at the outset, HIS and funds launched a TOB (takeover bid), which acted as a catalyst for the stock price to rise. This kind of trigger is called acatalyst.

However, Yasuda Warehouse’s securities report reveals that it has implemented a “defense against acquisition.”This is designed to assign new share options to a third party if a hostile bidder appears, thereby reducing the bidder’s stake.

If this is done, the bidder must either back off or sue. That would require significant effort, so bidders tend to be deterred. Incidentally,Uni-Zoo HD did not implement an acquisition defense, which was a contributing factor to the takeover battle.

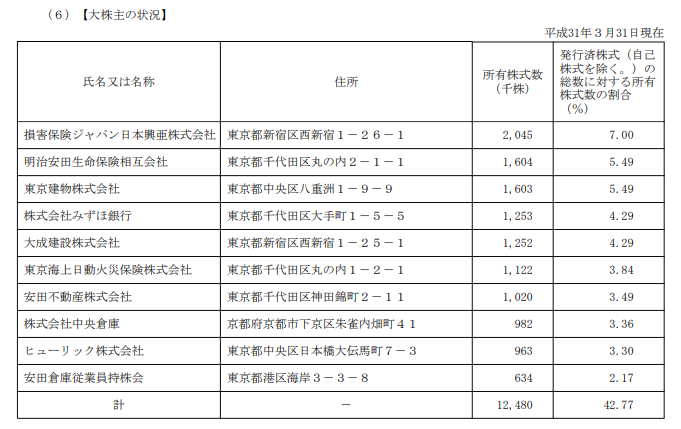

Moreover, looking at the shareholder composition, it is very stable.Founders and notable large corporations together hold nearly 50%, making it nearly impossible for a hostile party to gain a majority.

Regarding shareholder structure, Uni-Zoo HD had made missteps. Originally a bank-related (Mizuho Group) company,repeated public offerings reduced the share of stable shareholders, making the shareholder structure unstable. Well, that was their own fault.

Other warehousing companies are in similar situations, so it is difficult for a takeover battle like Uni-Zoo HD’s to happen. In other words, there islittle likelihood of a catalyst. Looking at past stock prices, even when undervalued, they rise briefly and then revert as sustained buying fails to materialize.

Stocks that are unlikely to fall and may rise if lucky

Of course, there is still a real possibility they will rise.

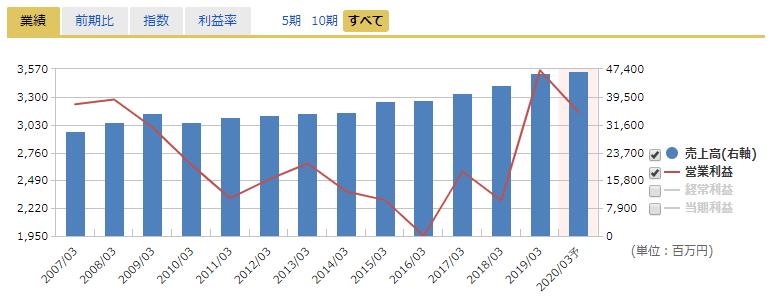

For Yasuda Warehouse, profits have recently increased, and even if profits remain, net assets keep accumulating, sothe undervaluation grows year by year. It would not be surprising if this is revisited somewhere.

Also,the payout ratio is currently around 20% and conservative, but if it were suddenly raised, it could attract new investors. The financial condition is healthy enough to support this.

Most importantly,the minimum value is guaranteed by assets held, and “if lucky, the upside could reach about 2x”, making the risk-reward favorable.

- Stock price is undervalued at less than half of the assets held

- Acquisition defense makes catalysts unlikely

- Value is guaranteed, and upside depends on luck

In other words, it is a battle against the time risk of “when will it rise.” Investments in such“asset-value stocks” aren’t necessarily efficient, but they are very solid. It’s not bad to know this.