Can ISB (9702) escape low-margin management?

ISB (9702) is a company established in 1970 that develops systems. In recent years, its performance has been improving due to the rise of IoT.

The performance of system-related companies has been very strong recently. In addition to significant technological advancements, the trend of work style reform is also contributing,with companies' investment appetite being very robustas well. The company's earnings expansion is believed to benefit from this.

Outsourced mobile development used to be the mainstay

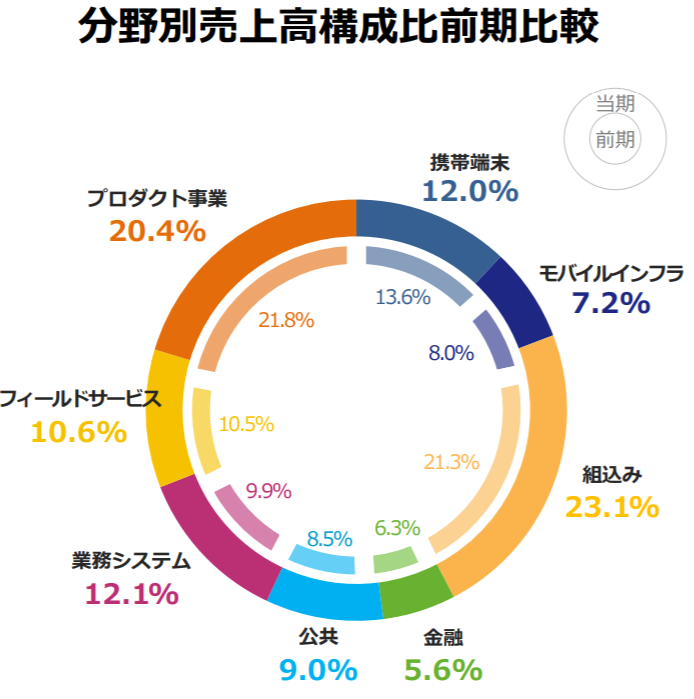

ISB originallyhad strengths in mobile phone developmentand is believed to have strong connections with KDDI and NEC. Following that trend, fields such as “mobile devices,” “mobile infrastructure,” and “embedded systems” remain the mainline even today.

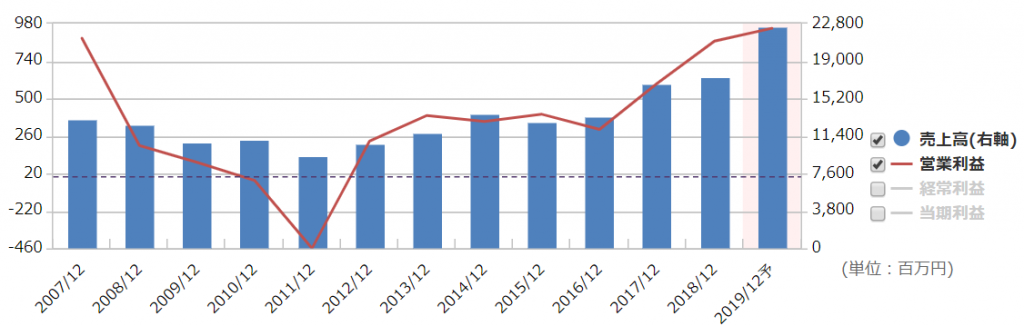

However, what is concerningis the low profit margin. While competitors have operating profit margins around 10%, this company has less than 5%.

The main reason is believed to be high personnel costs. Being a long-established company, salaries of traditional talent remain high, andthe average annual income exceeds 6 million yen. The average annual income for system integrators is cited as 4.7 million yen, which this company surpasses.

【Reference】Average annual income ranking latest by industry (DODA)

Also,since orders are basically contract-based, there are many projects with little price competitiveness (low profitability)that seem to be common.

Can it break away from low profitability?

The company also views the low profitability as a problem and has set as its first target the achievement of a 5% operating margin. As a measure for this,it aims to expand its own product business rather than contract development.

However, whether it is development capability or sales strength, there is not a strong sense of momentum. Its share of sales is around 20%, and it seems not to be pushing hard. It gives the impression of not being very aggressive.

Right now, momentum is more in the“embedded” business. Leveraging the technology cultivated in mobile phones,the automotive fieldandthe medical fieldare seeing increased orders. This is expected to grow steadily.

An ordinary company with fairly low prices

It is effectively a debt-free company with no major risks in sight.With market expansion, it is a company that grows its earnings gradually.

However, unless it breaks out of the contract-driven model, improving profitability will be difficult. It also seems to be struggling to secure talent, so explosive growth is unlikely. For now, its strength is that it is a stable company..

Recently, the stock price has fallen, and the P/E ratio is around 12, giving a sense of undervaluation. Looking at both the business and the stock price,there doesn’t seem to be a problem with buying.

On the other hand,it is a “ordinary” company to invest limited funds in. Its stock price is not dramatically undervalued, and large upside potential is hard to expect.

From now on as well, I would like to keep an eye on system-related companies broadly.