Central Motor Industry Co., Ltd. (8117) is a niche market Uniqlo? Exploring the reasons for the low rating and the “umami”

Chuo Auto Industries (8117) stock price is solid. In the current turbulent market,reaching the all-time highis being updated.

On the other hand,PER is around 9xand at a cheap level. Is this company a buy from now?

Uniqlo of a Niche Market

Chuo Auto Industries' main business isselling automobile coatings to dealers

The industry classification is “Wholesaling,” but since the company manufactures and sells its own products, it would be more appropriate to call it amanufacturing wholesaler. This is because they started manufacturing as they evolved from a primarily wholesaling company.

A representative example of moving from selling other companies’ products as-is to manufacturing in-house (the so-called SPA) includes Uniqlo’sFast Retailing (9983), andNitori (9843), and more recently, the business supermarket companyKobe Bussan (3038).

Chuo Auto Industries aims to be a “development-type company. This intends to hear the requests of closely connected dealers and manufacture and sell products that meet their needs.

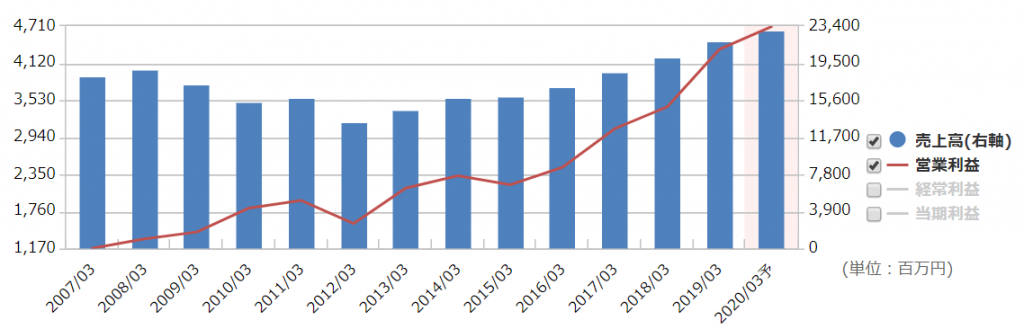

That strategy seems to be paying off. The performance is growing steadily.

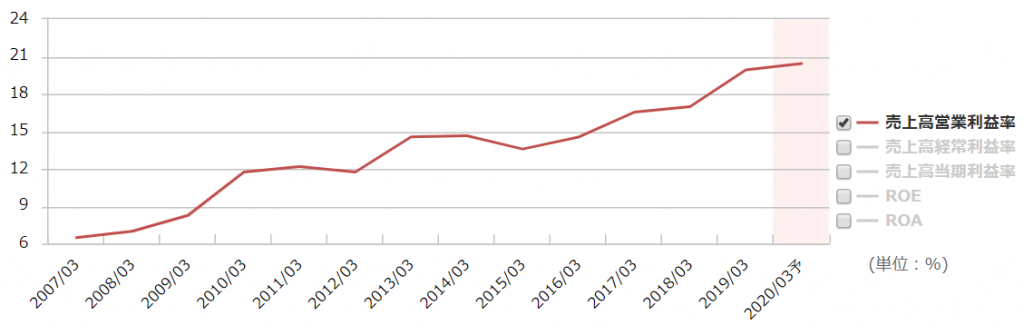

What especially stands out is the improvement in profitability. By expanding from wholesale to manufacturing wholesale, they have achieved higher profit margins. The most recent operating margin is 20%, a high level even for a manufacturing company.

Competitive Environment, No Weaknesses in Financials

In the niche market for coatings for dealers, Chuo Auto Industries holds the top share.

Rivals are original equipment manufacturers’ genuine parts, but the company deliberately does not make genuine parts to enable trading with various maker-affiliated dealers, crafting products that meet nuanced needs to attract customers.

Few other companies take the same position, so competition is not fierce. Although domestic auto sales are unlikely to grow rapidly,as long as they maintain careful customer service, shares can gradually, gradually increase.

Debt-free management, holding 10 billion yen in cash and 10 billion yen in investment securities. In 2017 they opened the R&D facility “Nakanoshima R&D Center,” and are putting effort into product development, leaving no shortage of potential growth.

In terms of business expansion, the stock appears flawless.

“Wholesaling,” “Automotive-Related,” “TSE Second Section” Dragging Down Stock Price

While the stock price has updated its all-time high,PER is about 9x, a low level. The low PER is not a recent phenomenon but a long-term trend.

Why is it not valued higher? I think it stems from the company's attributes.

“Wholesaling” tends to be undervalued. A prime example isMitsubishi Corporation (8058), a general trading company, with a PER of only 7x.

“Automotive-related” is also a headwind. The domestic auto market’s expansion prospects are slim, and the transition to electric and autonomous vehicles places the industry in a transitional period. With future concerns, even the largest in the industryToyota Motor (7203) has a PER of 9x.

Moreover, the listing market is theTSE Second Section. This market is generally viewed as middle-of-the-road—not a growth company nor a large enterprise.It is a stock difficult for both institutional and individual investors to buy.

The Delicacy of Low Valuation

Will Chuo Auto’s valuation remain low as is?

If you look pessimistically, yes. In fact,Trading houses will not see PER rise no matter how much earnings grow. This fixed notion is hard to change.

However, even if that is the case, Chuo Auto Industries’ earnings are growing. Even with PER of 10x, if they can increase profits by 10% annually, they could grow 60% over five years.

Also, with such favorable earnings and strong finances and a relatively cheap PER,downside risk is limited.

Furthermore, if the market happens to value the company positively in the future, what might happen? For example, if in five years PER doubles to 20x and profits grow 10% annually during that time,the stock price would become 3.2x.

In other words, the company can be seen as an investment withlittle downside and a potential 3x if luck favors. It may be quite advantageous for investors who do not avoid risk.

Of course, risks must not be forgotten.

Since dealers tend to coat cars mainly at the time of new-car sales,if automobile sales slump, earnings could temporarily dip. No company can completely avoid economic cycles.

However, even if the market share temporarily shrinks, if they can expand share during that period,when the economy recovers, earnings could rise substantially again. Fortunately, the company has financial buffers to withstand temporary downturns.

Currently the stock price is rising, but there is still a sense of being undervalued. As an interesting stock, I plan to continue monitoring it.

★ Comprehensive investment information! Click here for the Tsubame Investment Advisory homepage ★