IR Japan (6035) is a niche-top subscription stock! The first to find it reaps the profits

The environment surrounding Japanese listed companies is changing dynamically. In the past, inter-companycross-shareholdingwas common, but as Western-style management has permeated, the prevalence of cross-shareholding has continued to decline.

In such a situation, stable shareholders are decreasing, and listed companies are exposed to potential pressure from external shareholders.All of a sudden being bought out by a company you don’t know at allcan also happen. For example, the old Murakami Fund buys up undervalued companies’ shares and pressures for management reform and dividends.

This is necessary for the healthy development of the capital market, but management cannot be complacent. There are funds that pursue only their short-term profits,and we must keep a keen eye on changes in our own shareholders.

A subscription business that is indispensable for listed companies

IR Japan HD (6035) has been a company that meets such corporate demands by carving out niche markets.

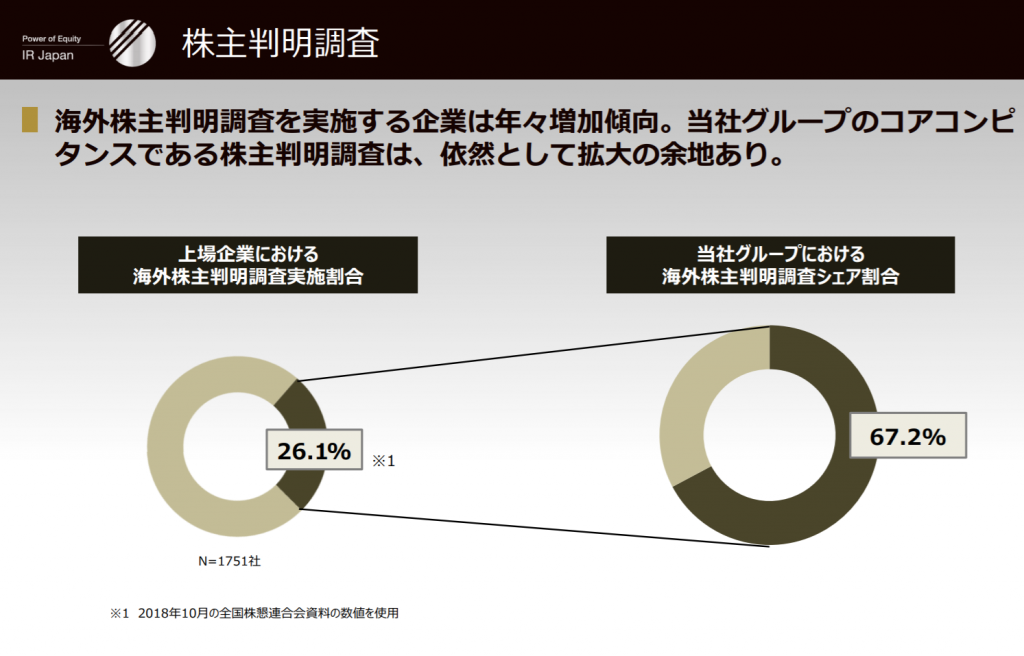

What the company excels at issubstantive shareholder identification investigation. Many foreign shareholders buy Japanese stocks using trusts called “custodians,” so it is difficult to determine who is buying just by looking at the shareholder registry.

Therefore, the company conducts this investigation on behalf of clients. From there, it provides advice on how shareholders exercise their voting rights and how to communicate with shareholders.

If a company has already received a letter from an activist investor, it will ask the company to address the matter through their services. Shareholders change daily, so contracts are inevitably renewed. In other words, IR Japan’s business is a trendysubscription (regular subscription) model.

A tasty stock that offers both stability and growth

The company holds 67% of the market share. Meanwhile, only about 26% of domestic listed companies engage in shareholder measures, indicating there is still room for growth.A stable yet growth-ready, tasty stockcould be said.

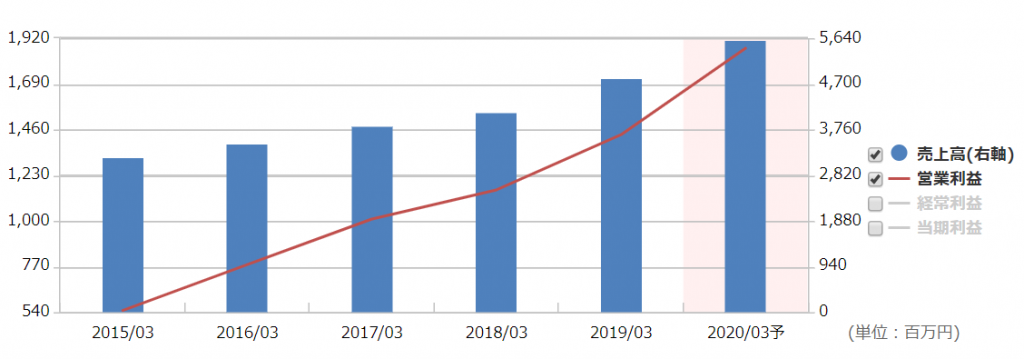

Performance is steadily increasing. Rising awareness of corporate governance is also a tailwind for market expansion.

The company’s business does not require much additional investment or cost even as customers increase. In other words,if the market expands, profits will grow faster than sales. With motivation, expanding related consulting businesses should not be difficult.

Look for a "niche top" that is ahead of the competition before it becomes overvalued!

The risk isthe emergence of strong competitors and intensified price competition. However, at present, it’s mainly provided by “○○ IR” under the umbrella of major securities firms, done in a part-time manner.

Therefore,for the time being, the company’s superiority is unlikely to waver. There appears to be no blind spots for stable growth in the coming years.

However, even though this is such a good company,the stock price will still be expensive. The PER for this year’s earnings forecast is around 40x, a level that is hard to approach. I wish I had spotted it earlier.

Thus,there are hidden large-growing companies even in niches. Of course, I will continue to diligently look for other similarly promising firms as well as keep追ing this one.

★ Full of investment information! Visit Tsubame Investment Advisory’s website ★