Hamaki Group Logistics (9037), boasting standout profit margins in corporate logistics. A big breakout stock is born from a modest, unglamorous industry

Many companies consider logistics indispensable for their business activitieslogistics. This will not disappear even as the internet society progresses. On the contrary, it is expanding due to the rapid rise of online shopping.

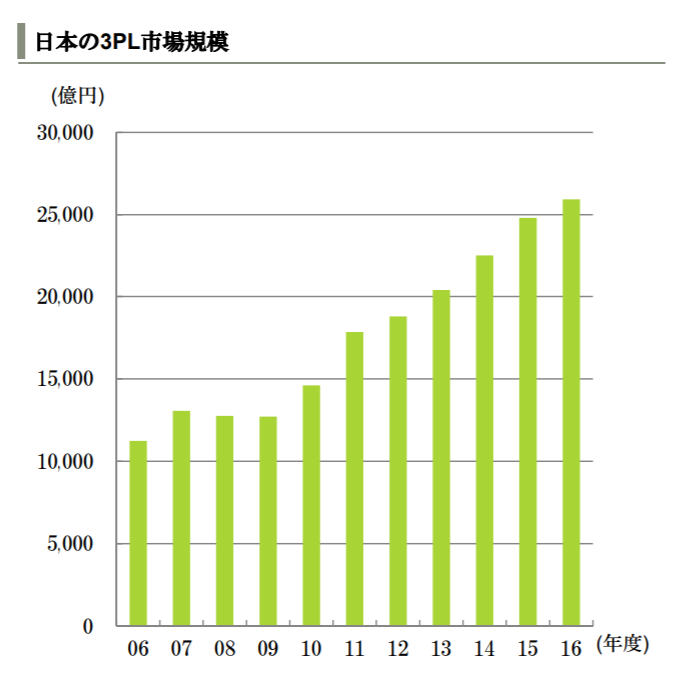

A company with outstanding profits in the expanding 3PL market

When you think of logistics operators, Yamato Holdings (9064) and SG Holdings (9143) = Sagawa Express come to mind, but these are household delivery companies.

Many trucks on the road are carryingintra-company and inter-company logistics. While companies may handle this themselves, recently logistics operators have been taking on most of it,third-party logistics (3PL)is becoming mainstream.

3PL means logistics companies themselves own centers and transport their customers’ products and materials. They accumulate specialized logistics know-how suited to the industry,allowing client companies to conduct logistics more efficiently and focus on their core business.

The 3PL market continues to expand. In a society that eliminates wasteful costs and labor, there is still a large room to uncover demand.

The market continues to expand, but transport operators are by no means highly profitable. A flood of small and large operators leads to fierce price competition, while labor costs are rising.Each company manages to secure only a few percent of profit.

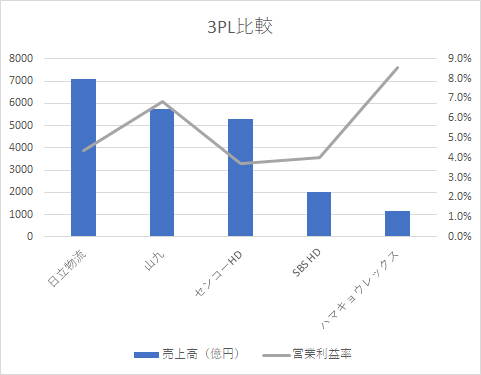

In such a context, Hamakyō Rex (9037) stands out with high profitability. In terms of scale, it is mid-sized, but its profit margin is outstanding. This has been a long-standing trend, not a recent development.

Hamakyō Rex originated in Hamamatsu in 1971. It entered 3PL in the 1990s and has expanded its operations since.

Thoroughly cutting costs that do not lead to profits

Its features includethorough cost reduction andM&A with small and medium-sized operators.

The founder and current chairman, Masataka Osuga (78), adheres to a management philosophy built from the ground up to generate profits. This has been passed on to the current president, his son, Hidetoku Osuga (52).

Reference: Yaramai Logistics Industry - Hamakyō Style: The Prosperity of Carriers

Cost reduction is not done by overexertion. It is reflected in the numbers.

Looking at each company’s performance, operating costs are about 90% of net sales for all, and Hamakyō is no exception. This does not indicate that they are stinting on personnel or vehicle costs.It shows that they are not being stingy with labor costs or vehicle expenses.

So where do they cut costs? In selling, general and administrative expenses. For example,even if money is spent on the headquarters, profits won’t rise, so they cut such areas thoroughly.

Hamakyō’s operating expense ratio to sales is only 2%. For other companies, this is about 5%. From a 10% gross profit, this much is deducted, soas a result, operating margin appears as an 8% difference from 5%.

A haven for small and medium-sized businesses in distress

Profits gained from more efficient operations by others go toward M&A. However, the company is not expanding through aggressive M&A. Rather, itinherits the business of companies that seek consultation.

There are many transport operators in the country, most of which are small and medium-sized businesses. They lack sufficient management know-how, so they struggle with price competition and rising labor costs. Hamakyō takes them on, reforms management, and returns them to profitability.

As the scale grows, more logistics centers can be built, enabling economies of scale to be realized.The market is expanding, so the company can grow accordingly.

The big stock often comes from quiet industries

If this management style can be maintained,Hamakyō will continue to grow steadily.

However, competition is intense and profit margins are low, so there is a risk that performance could deteriorate quickly if not careful. In other words,it depends on management, for better or worse.

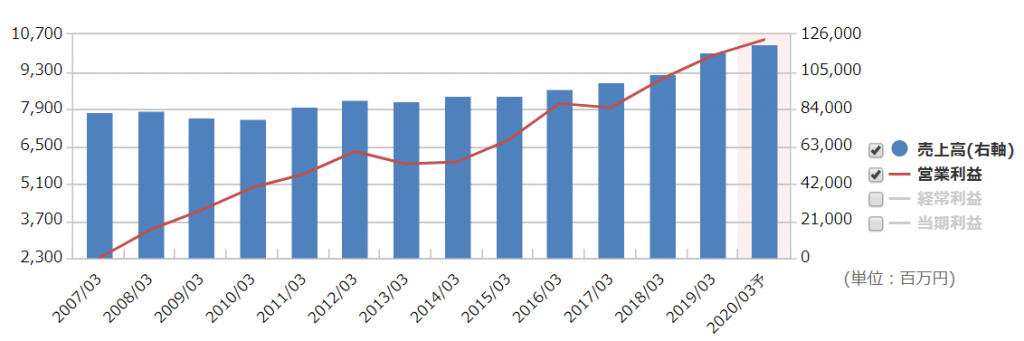

Financially, there are no major issues. The PER is a little under 12, which is average compared to others in the same industry.There is little room for decline, so if performance expands, the stock price is expected to rise accordingly.

Although a modest industry,stocks like this can unexpectedly produce big windfalls. I will continue to monitor future developments.