Elecom, continuing to grow (6750). Can it maintain a competitive edge in a highly competitive industry?

Elecom (6750) is a company that sells PC and smartphone peripherals. It is a “fabless” manufacturer that does not own its own factories, outsourcing production to companies in China and Taiwan.

An industry that must keep moving. The key lies with the founder

Starting with PC peripherals such as mice and keyboards, the company has been expanding its lineup to meet growing demand for smartphone films, cases, and cables in recent years.If you go to an electronics retailer, you will surely find the company’s products.

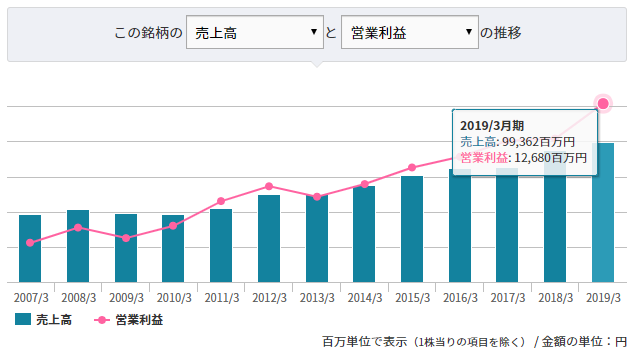

Performance is very strong, with continuous year-on-year growth. The company is leading the expanding market as a top player.

The strength of fabless manufacturers lies in flexible production capacitybecause the lifespan of PC and smartphone peripherals is not long, they must continually release products that meet market needs. This naturally leads to multi-product, small-lot production, which would be difficult to handle if the company owned its own factories.

The capabilities required of such companies are,to accurately grasp market needs and quickly place them on the leading shelves. Elecom excels in this regard, developing new products one after another and getting them onto shelves in powerful electronics retailers with strong connections. It is precisely because of this capability that the company has been able to stand as a top runner.

However,it is also true that competition is intense in this field. Outsourced production can be, in effect, enabled by anyone who has the design drawings. Chinese manufacturers that contract production can also sell the products as is. The products themselves are not particularly difficult.

In other words,it is difficult to keep winning unless you are continuously moving. In that regard, it cannot be said that the company necessarily has a “moat” in the sense of a protected competitive edge.

Nevertheless, the reason the company has continued to win so far seems to lie in the founder’s personality. The founderMr. Heda is reputed to be constantly on the move, driving product development from the top down. This has likely been the driving force behind leading a fast-changing market.

With that in mind,the greatest risk for the company is a change in leadership. He is still 65, but in interviews he has said he wants to step down cleanly, and to that end he has hired engineers to strengthen the company’s strengths and has acquired antennas companies that operate stable B2B businesses.

【Reference】Bridge between major firms and entrepreneurs: Elecom President Junji Hada (Nikkei)

Many challenges, but solid ability. The next development is worth watching

How long the president will stay, how long the smartphone-driven market will continue to grow, and whether the acquired companies can be managed well—all are still significant questions. Yet the company has continued to grow because it has real capability.

The stock price has continued to rise. Even so,the P/E ratio is 18x, not particularly high. If the favorable trend continues, it is believed that annual growth of about 10% could be achieved without relying on market factors.

On the other hand, as mentioned above,it does not have a strong “economic moat”. Considering future risks, it is not necessarily a bargain, so it isn’t exactly a buy-now situation.

With essentially no debt and no financial problems, the company’s future management trends, including potential M&A, are of interest. I will continue to monitor how the stock price evolves.