Three companies expected to grow in the information services sector (System Information, Minori Solut ions, Obic)

Even as the domestic economy stagnates in the futureone of the industries expected to grow with high probability is information services.

With the labor force also shrinking,companies must increasingly streamline their operations. And many of these can now be done by systems.

Japanese companies have lagged in adopting systems compared with advanced nations, and their low productivity has been conspicuous. Due to labor shortages and work style reforms, the momentum for adoption is finally rising.

Using AWS (Amazon Web Services) or Microsoft Azure, anyone can now access systems from anywhere. On the other hand, it remains difficult for non-experts to implement, andan intermediary “system vendor” must be involved for easy deployment.

This system vendor, together with Amazon and Microsoft, isan indispensable presence for corporate IT modernization. In that context, we introduce some of the companies that caught our attention by looking at the recently released Quarterly Reports (Shikiho).

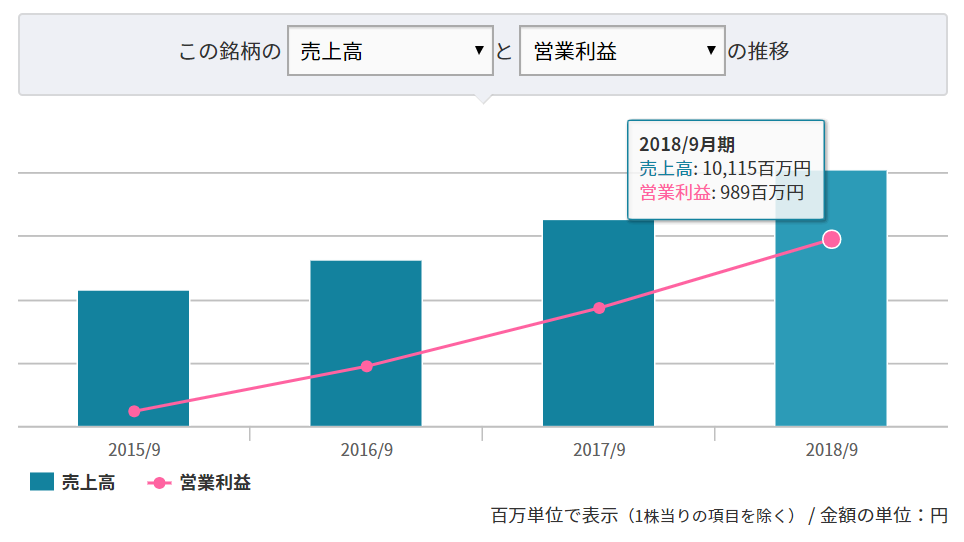

Systems Information (3677)

Specializing in large-scale system development, with many orders from financial institutions. The performance has beensales roughly doubled in four years, rising sharply.

Its strengths includeholding the highest level 5 in CMMI, the maturity model for an organization's software development process. In Japan, only about 10 companies, mainly major system vendors, hold this certification. Large corporations, confident in these vendors’ stability, place orders with Systems Information from among many companies.

The president and managing director are also from NTT Data, making a solid lineup. Their trust from financial institutions is likely high.A small but rapidly growing company that also exudes a certain gravitas.

What’s concerning isthat orders come from specific companies and subcontracting work is heavy. For example, Dai-ichi Life’s systems account for more than 10% of sales, and subcontracting from Mitsubishi Electric Information Systems and NTT Data is substantial. If customers cut back or are removed for some reason, the damage could be significant.

The stock price continues to rise, with a high P/E ratio of around 24 times. Nevertheless, ROE is also high at 26%, andas companies become more system-dependent, the outlook is favorable. In that sense, achieving CMMI Level 5 would be a strong economic moat.

There is no need to rush and buy, but if the market drops sharply, this would be a stock to target.

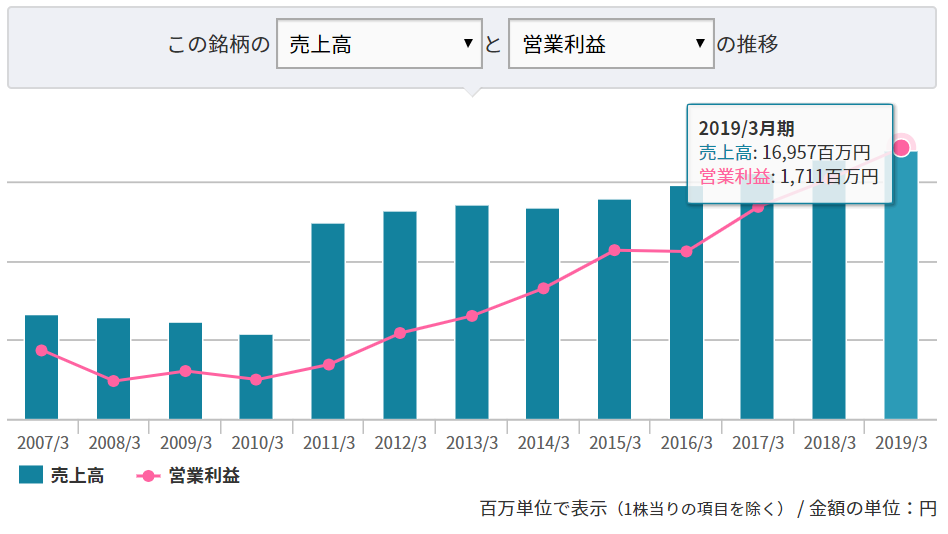

Minori Solutions (3822)

This business model is almost the same as Systems Information, handling corporate system construction.

In particular,the relationship with Mitsubishi Research Institute DCS through a capital alliance is strong, and related sales account for about 15% of total. Other sales to SCSK (Sumitomo Corporation affiliates) account for about 10%. Here too, subcontracting is a strong characteristic.

Unlike Systems Information, externally they do not appear to have major strengths. Still, their performance is steadily growing, signaling industry growth prospects.

Even when looking at similar companies with similar business models, operating margin remains around the same level (about 10%), and is on an upward trend.Even without a major differentiating factor, demand is sufficiently strong and there is no over-competition evident.

The reason competition is not intensifying is, ironically, due to labor shortages. Large-scale development requires many system engineers, but supply remains tight. Therefore,large, well-known companies with easy access to talent have an advantageous environment.

Minori Solutions was founded in 1980, giving it a decent history and it is listed on the first section of the Tokyo Stock Exchange. This is part of its strength. On the other hand, fixed customers could lead to a sharp drop in orders in a pinch.

Perhaps because the economic moat is less visible,the P/E is about 13 times, roughly half that of Systems Information. It looks cheap relative to earnings growth, but it is necessary to determine whether this growth is due to favorable economy, industry expansion, or internal efforts.

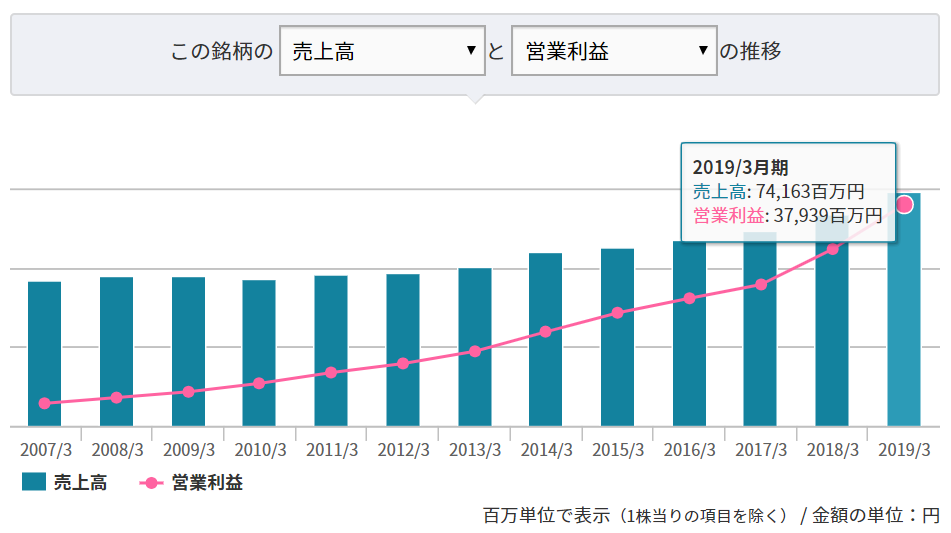

Obic (4684)

A company that develops and sells packaged ERP (Integrated Core Business Systems). It was established in 1968, which is unusually long-standing for a system company.

To be blunt,this company is too profitable to stop. Its operating margin exceeds 50%, and it has steadily grown year after year without doing mergers or acquisitions, maintaining growth through in-house development.

ERP, once implemented, will have all of a company’s numbers in it, making it hard to switch to another system. It is said that switching costs are high. Because they have done this for a long time, earnings have continued to accumulate, andachieved 25 consecutive years of profit growth.

Like the two companies above, most system vendors outsource the actual programming, butObic does everything in-house. This might contribute to the software’s ease of use.

Strong performance and solid financials are reflected in a high P/E of 33 times. However, this is not simply overpriced; it seems to be a company worthy of such valuation. While the stock price continues to rise and the timing to buy is difficult, I would like to buy on pullbacks.