Can Bourbon (2208), which holds many staple products, become a Buffett-style “monopolistic consumer company”?

If the consumption tax is raised as planned in October 2019, consumers will tighten their purse strings even more. After that, the winner-take-all in supermarket aisles will become clear.

Coca-Cola 20 Times in 30 Years

As a value stock investor,you must invest in companies that sell products that can withstand tax increases on consumption. This is nothing other than Buffett's notion of an "economic moat" or monopolistic consumer goods.

Buffett's success story is often cited asCoca-Cola. Buffett began buying in the late 1980s, and over the next 30 years its value grew about 20-fold.

Additionally, the power of dividends is strong.The current dividend yield relative to the acquisition price is as high as 50%. This is because Coca-Cola has continued to increase distributions as it grew. It truly is a "cash cow."

Many Core Products, Sound Business and Finances

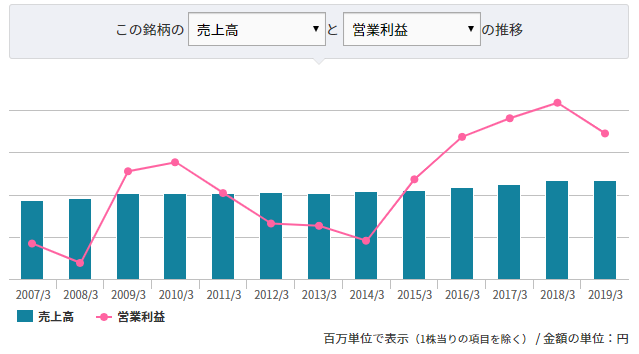

So, what would be Coca-Cola in Japan? This led me to focus on the confectionery makerBonbon (2208). They offer familiar sweets such as "Alfort," "Petit," and "Elise."

The stock price isPER 13x, suggesting a value, and it has recently hit a new YTD low. Meanwhile, earnings are gradually expanding.

Even if consumption tax rises, demand for staple products should stay solid, so there may be little to worry about.Financially, effectively debt-free, with no major risk factors seen.

Growth is Underwhelming

On the other hand, growth is somewhat unsatisfying.

The company says it aims to be a "global company connected to the world while being local,"yet overseas sales are almost nonexistent.

There are limits to expanding in a shrinking domestic market. If it grows domestically, it must either increase market share or raise prices to preserve profits.

However, I sense a cap on market share. To grow significantly, you may need to find a new distribution channel that is not the traditional supermarket (subscription services or regular deliveries could be suitable, though they do not seem to be in place yet).

Also, the advantage of Bonbon’s products is that they offer high performance for the pricerelative to their price. They are relatively inexpensive and reliable no matter what you buy. Conversely, if prices rise, the value proposition would become weaker and could be a loss leaderfor the brand.

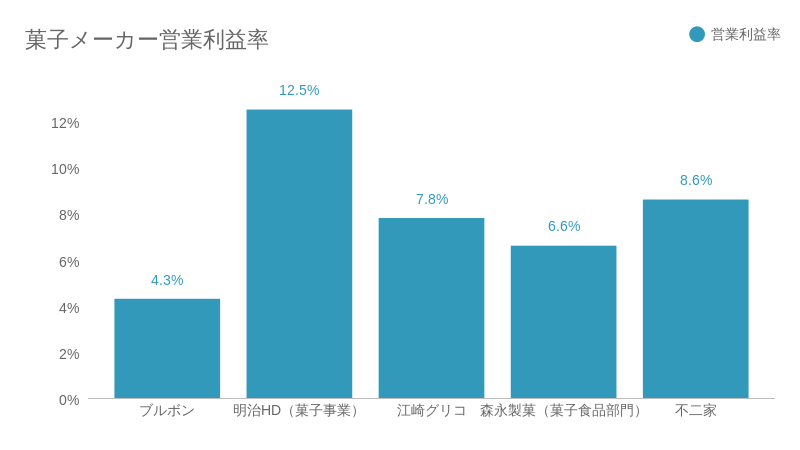

Looking at operating profit margins among confectionery makers,Bonbon shows how cheap and good its products are. But that also means a structure that makes it hard to earn profits.

To break this structure, aside from conventional products, you need to launch more profitable productsthat generate higher margins. However, those seeds are still not visible.

In summary, Bonbon is financially and operationally stable, but its growth is not high. The stock price is somewhat cheap, but not at a level where one would necessarily want to invest now.

Learn from Calbee’s Frugra

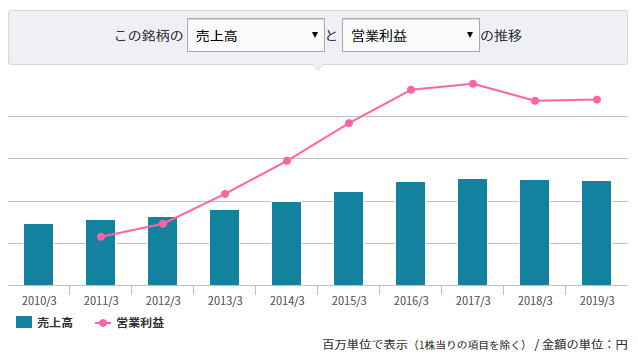

As a growth example for food makers, I look atCalbee's case. They developed the cereal "Frugra" made with abundant dried fruit, creating a new category.

They then sold it in overseas markets like North America and achieved success.Simultaneously achieving improved margins and geographic expansion through new market discovery.

In other words, for food makers, the keys to growth will continue to be "developing new categories" andexpanding into overseas markets. In particular, the trust in Japanese products in China, where domestic demand is rapidly expanding, seems to be a potential key to breakthroughs.

Whether Bonbon can achieve this remains uncertain, but I would like to view the entire food industry from that perspective.

※Please also see Tsubame Investment Advisory’s services.