Why investing all of your assets in index funds for asset management in your 50s is a mistake. What are the real measures you should take?

A feature titled “In your 50s, there’s still time” has been organized in Nikkei Veritas.Shortfall of 20 million yen after retirementbased on government documents.

I felt anger toward the financial planner who said, “Just invest everything in a global equity fund”

As you approach your 50s, retirement becomes a real possibility, andfor those who have not taken measures so far, it becomes unclear what to doabout. Starting asset formation from now, you don’t know where to begin.

Among them, a certain financial planner wrote“Assumed return 5%. Invest everything in a global equity fund”When I saw this, as a fellow expert, I felt“What an irresponsible statement!”.

Indeed, the expected return of the world stock market is said to be above 5% annually. However,if a 50-year-old person thinks they can reliably get 5% just by putting all their existing assets there, that is a major mistake.

Bonds, on the other hand, provide a steady interest every year. Therefore, by buying highly rated ones, you can obtain a fairly “certain” return. However, the return here mainly refers to gains from stock price fluctuations.Stock price fluctuations are by no means stable.

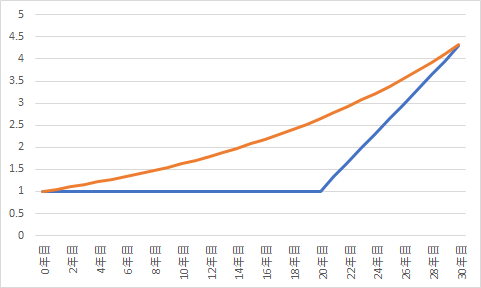

Then, what is a 5% annual return? It isa retrospective long-term performance calculated backward. If you think you can get that in the next year, you are making a big misunderstanding.

Suppose the calculation period is 30 years. Perhaps the first 20 years’ return is zero. The next 10 years may stay flat,but if the last 10 years rise by 4.3 times, the 30-year annual return becomes 5%.

In this way,stock returns are not linear but non-linear.

If a 50-year-old person invests now,what happens if it remains flat until the 20th year, i.e., until age 70. Money doesn’t grow, and you cannot feel secure. You might quit halfway, thinking it didn’t work.

You might think 20 years of flat performance is long, but such things can actually occur. Japan’s 30 years of Heisei era were exactly like that, andthe US also experienced a “death of stocks” in the 1970s when stock prices hardly grew. There is no investment with no risk.

Moreover, if prices stay flat or, worse, rise and you buy when stocks are overpriced, even if you call it an index fund, it’s not easy to recover.Can someone who has never invested endure a long-term drawdown?

Therefore, those starting to invest should not decide on “this” from the outset, butlearn for themselves what investing is all about. Index investing is the same. If you do so, you won’t be swayed by absurd stories, and above all it becomes an effective way to alleviate anxiety.

Is your retirement plan sufficient? Calculations aren’t difficult

So what should people in their 50s who fear the future do? The following is written from the viewpoint of “what I would do.” Please use it as a reference.

(1)Calculate retirement assets (no investments)

First, estimate future assets. The main factor isthe sum of current savings and retirement allowance. You can roughly guess how much your company’s retirement allowance will be by listening to salary tables and people around you.

By the way, when I left the company to become independent, I asked a senior of my generation who had retired earlier. The amount was 500,000 yen! Even though I had joined for less than seven years,I was shocked by how little it was and recalculated my independence funds.

If you do this, you should be able to determine whether you have at least 20 million yen.

(2)Calculate pension and expenses balance

Upon retirement, the only reliable income is usually the pension. In fact, you can easily calculate how much pension you will receive from the following site.

Simple pension estimate - expected pension (PSRnetwork)

Based on this, a person born in 1968 (50 years old), with a university degree and 40 years of service, and an average annual income of 5 million yen,will receive 1.9 million yen per year from age 65, or 158,000 yen per monthas pension.

Would this amount be enough for your life? Consider your current living costs.If you require 200,000 yen per month, you would have a shortfall of about 50,000 yen. In that case, the government’s estimate of needing 20 million yen holds.

(3)Consider how to fill the gap

If your income and expenditure are in the red, and you have little assets,you must think about how to cover the shortfall. Also, even if you’re in the black, having a bit more gives you more leeway to enjoy your later years.

Work or passive income, or stocks. Preparation and experience are essential in any case

I see three main ways to fill the gap.

- Work

- Have assets that generate regular income

- Grow your assets

If you can keep working, almost all retirement anxiety disappears. Working doesn’t mean you must work five days a week, eight hours a day like during your career. If it’s 50,000 yen per month, that’s easier than a college student’s part-time job.

Of course, applying your experience instead of manual labor will likely contribute more to society.Starting now to prepare for a small business that earns some income is one option.

The assets that generate regular income aredividends and rental income. With high-dividend stocks, you can earn about 5% per year, so with 20 million yen you can receive after tax about 800,000 yen per year, or 67,000 yen per month.

Yes,with 20 million yen you can supplement with about 50,000 yen per month without touching the principal.

However,it is too risky to start investing with retirement funds for the first time. Everyone makes mistakes at first, but once retired, it’s hard to recover. Also, if the timing of your entry is when prices are high, dividend yields will drop.

Moreover, it would be terrible if you fell for a ponzi-like real estate investment out of the blue.Real estate can leave you with not only your own funds but even debt if you fail.

Therefore,you need to study and learn as early as possible. With experience, you won’t fail dramatically when you retire. If you accumulate high-dividend stocks before retirement, you can study and prepare at the same time.

Finally, for those who lack assets but do not want to work at all,investing to grow assetsis a possibility.

However, as mentioned above,it is extremely dangerous to pour a large amount of money into a specific asset including indexes all at once. Instead, you must accumulate experience by investing gradually in something you yourself think of.

In your 50s, you still have about a decade before retirement. If you continue investing for 10 years, you will begin to understand companies and market trends. Of course, you will make mistakes at first, but you can recover over time if you don’t push beyond reasonable limits.

In other words, “starting to invest” meansnot betting everything on something right away, but gradually accumulating experience. By doing so, you’ll have more time to think about money and it will prompt you to reconsider how you want to live.

I offer services because I want you to have a way to start investing.First, by following my example you can avoid major mistakes and begin investing. Please take a look at it sometime.