Conduct a 10-year backtest and a 2-year forward test in a simulated manner to avoid excessive parameter optimization

■ Overview

EA “Senji Ban-kou” and “Yamamurasaki Suimei” have been functionally added to MT5 Strategy Tester

We conducted both backtesting and forward testing to avoid excessive optimization of parameters.

■ Forward Test

When developing an EA and performing long-term backtests, I always worry that it may not perform well in forward tests,

and after release, for the first three months to about half a year, it may show good profits, but many EAs

tend to go into losses afterward. There are several EAs I have created in the past with this tendency.

Therefore, as shown in the figure below, we split historical price data into two parts for backtest and forward test,

optimize the parameters in the backtest, and then confirm in the forward test that optimization has not been excessive.

We release after running about 10 years of backtesting and about 2 years of forward testing.

This has given us much more confidence in the release.

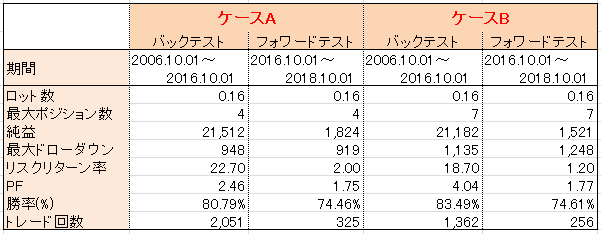

■ Example

Which would you choose?

Case A Backtest

Case A Forward Test

Case B Backtest

Case B Forward Test

Compared with Case A and Case B backtests, Case B shows PF above 4 and looks favorable, but the forward test results

show that Case B's performance drops significantly more.

We perform such verifications for “Senji Ban-kou” and “Yamamurasaki Suimei” before release.

Therefore, after listing with Gogo-jan, for about six months to eight months, we have obtained good forward results.

■ Sales Site

“Senji Ban-kou” https://fx-on.com/systemtrade/detail/?id=14944

“Yamamurasaki Suimei” https://fx-on.com/systemtrade/detail/?id=15576

(Please replace this part for public release)