The president of Solast (6197) is an elite who graduated from Stanford MBA. Will the rapid progress of the caregiving business continue?

Solarst (6197) is a company that undertakes medical clerical work and provides nursing care services.

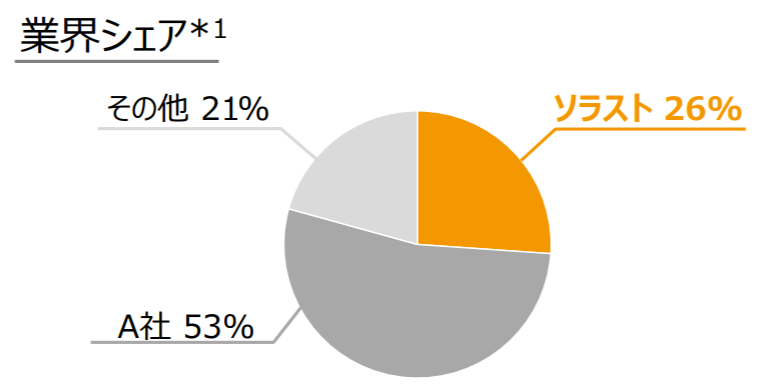

In medical clerical work, it boasts the industry’s second-highest position next to Nichii Gakkan (9792). The two companies together hold about 80% of the entire industry, making them overwhelmingly dominant.

A Solid Medical Clerical Outsourcing Business Generates Abundant Profits, Invested in Nursing Care M&A

In Japan, where the aging population continues to advance, healthcare is still a growing field. Many hospitals operate inefficiently, leaving substantial room for expansion.A promising business, blessed with an economic moatthat can be seen as such.

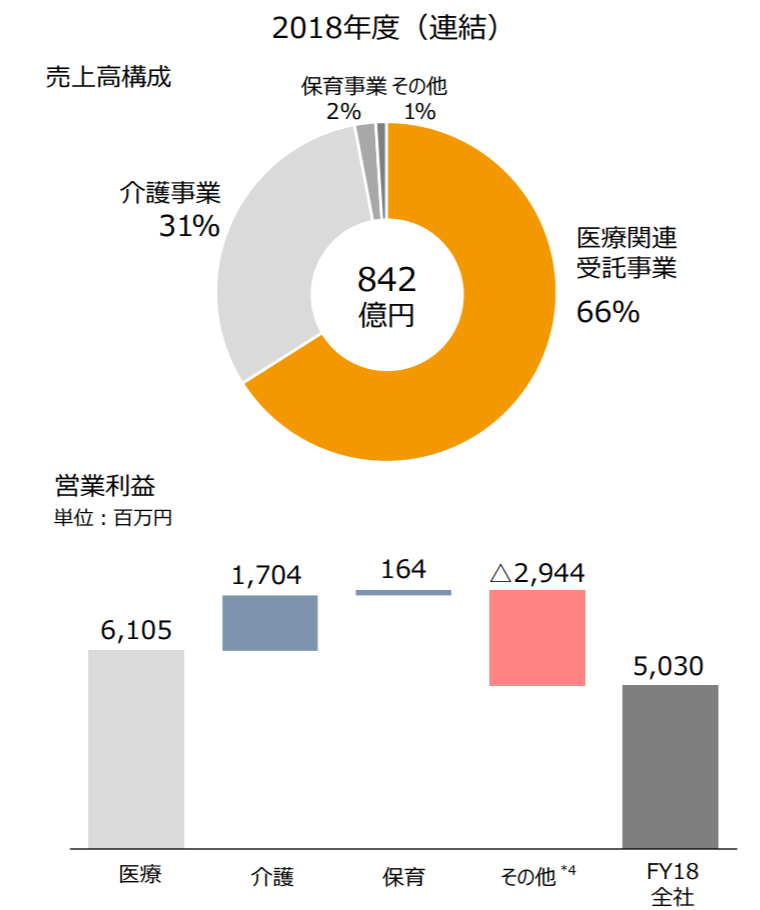

The operating profit margin of the same business is also high, recently recording 11%. The majority of operating profits are produced by this business.

Even with this alone, it already appears to be a first-rate company, but it has further ambitions. That is,expansion of the nursing care business.Using M&A, it aims to expand in areas with even greater growth potential than medical care.

Utilizing the abundant cash generated from the medical clerical outsourcing business for M&A in the growth area of nursing careis an ideal style for a growth company. It is a textbook corporate development drawn in pictures.

The CEO Is an Elite Stanford MBA

This too is possible thanks to the CEO’s prowess. President Ishikawaholds a Stanford University MBA and is an elite who has moved from Nichimen Iwai to GE in the United States. Frankly, such a person is mismatched with the industry.

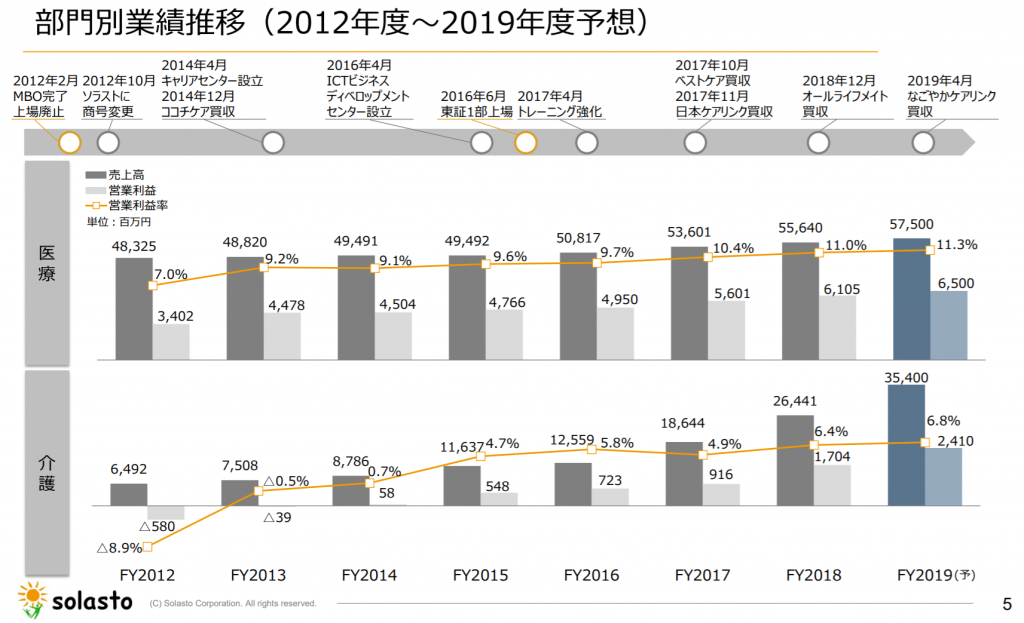

In fact, Solarstengaged in an MBO (going private) with the Carlyle Group in 2012. The Carlyle Group introduced President Ishikawa. He reorganized the previously opaque management, and re-listed on the Tokyo Stock Exchange First Section in 2016.

Carlyle has already sold its shares, but Ishikawa remained. Now he has abold plan to multiply sales by 3.5 times and profits by 4 times by 2030. There is also expectation for growth after the re-listing.

Where Do Nursing Care Profits Come From?

What worries about this company is the profit from nursing care. It is generally a difficult industry to make profits in, with an industry-average profit margin of around 3%.A profit margin exceeding 6% is overwhelming, but I have yet to fully understand the clear factors behind it.

There are many parts that can be streamlined by expanding scale. Also, ICT utilization is being promoted.

However, the largest weight in nursing care islabor costs, and if these are being cut, problems may arise later. It’s worth watching this for a while.

Also, achieving successful M&A is not easy.The success rate is about 30%. In such a context,if CEO Ishikawa were to resign, questions would remain about continued growth afterward.

Because it is not a large company,the CEO’s movements have a significant impact. This is something to monitor carefully.

Recent Stock Price Decline. Can It Be Considered Cheap?

Recently, the stock price has fallen significantly. The reason lies in bid-rigging in orders from public hospitals and local governments, leading to inspections by the Fair Trade Commission along with Nichii Gakkan.

This incident stems from the industry’s high market share turning against it. While not conclusive, it is not considered fatal.

The issue is whether the fallen stock price is cheap.

This year’s projected profit-based P/E is 18x, butexcluding extraordinary gains, it is effectively about 23x. It is not overpriced, but not necessarily cheap either.

With growth from M&A and efficiency improvements increasing profitability, the company is expected to continue growing.If the stock price falls further or if growth drivers become more convincing, investment may be considered.

We will continue to monitor future developments closely.