Are selling and buying symmetric?

Selling and buying in trading are not symmetric.

In stock trading, some high-volume institutional investors engage in noticeable short selling in certain stocks. Of course they short to make profits. It’s a kind of legitimate fraud. They entice individual investors to buy stocks by promising profits, while institutions and brokerage firms borrow those shares to short them, driving prices down and forcing stop-outs. High dividend yields, target prices, low PBR and PER are just tools of fraud. “Losses from individual investors' stop-outs = profits for short-selling institutions.”

“It’s easy for the manipulators to push prices up, but difficult to push them down.” Note that in the stock market, selling and buying are asymmetric. When buying, profit-taking occurs, making it harder to raise prices and thus harder to profit. Conversely, when selling off, stop-outs occur, allowing prices to drop more, making it easier to profit. Also, when buying back, profit-taking sells are present, so buying back does not raise prices much. In other words, there is an inherent asymmetry in the stock market where selling off and then buying back can automatically yield profits.

Of course, there are times when buying pressure begets more buying, and short selling is squeezed and the price does not fall, so casual short selling is extremely dangerous, to be noted.

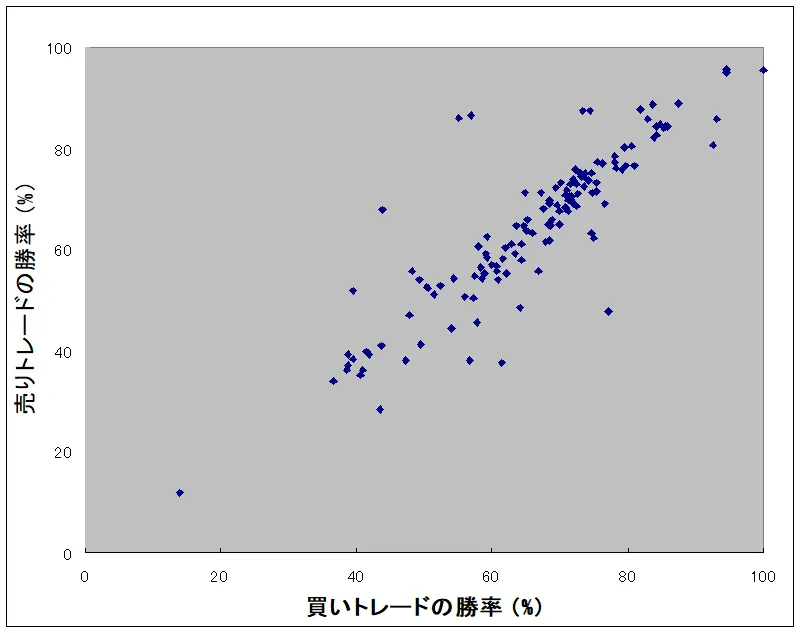

In FX markets, which often move up and down, repeatedly confirming resistance and support, selling and buying are not symmetric. Even in EA (expert advisors) that are often technically crafted symmetrically, there are differences in trading performance to some extent. The figure below plots the win rate of short trades versus long trades for the EA in GoGoJiang’s “Real Account EA Operating Rate” backtest. The two often align closely, but there can be notable differences.

One cause of asymmetry is swaps. Positive swaps in USD/JPY can yield substantial returns with long-term holding. For example, with USD 1, 160 yen, 1000 units, a swap of 10 yen per day yields an annual return on margin exceeding 50%, so buys tend to be long-term and sells tend to be short-term. Swaps vary by currency pair. The above figure includes various currency pairs and also XAU/USD, so a per-pair aggregation and plotting is necessary.

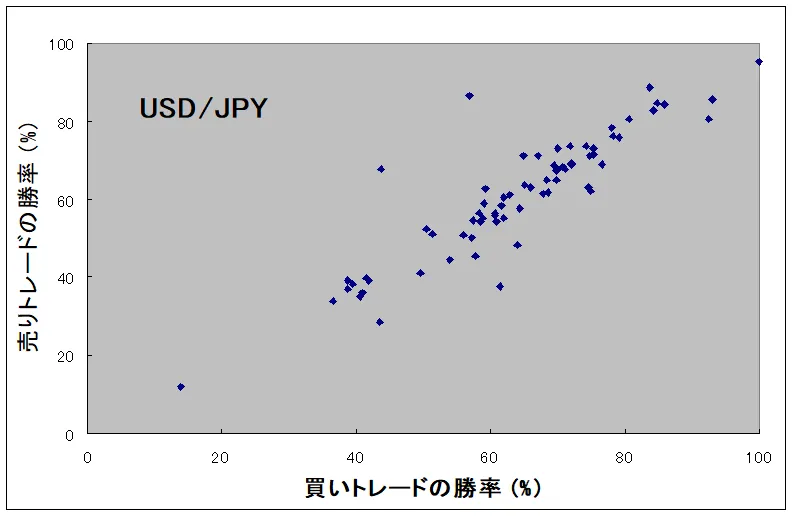

When limited to USD/JPY, it looks as follows.

“There is some variation, and it seems buy trades have higher win rates than sell trades, though not clearly so.” However, this graph does not reflect eight EAs limited to buying trades; those naturally suggest buying trades are superior to selling trades.

Therefore, for EAs limited to buy or sell directions, we calculated the advantage rate per currency pair (including XAU/USD) and compiled a table. Included also are approximate swap values (as a percentage per day of the currency value).

-------------------------------------------------------------------------------------------------------------

Currency Pair Buy Win Rate Sell Win Rate Buy Advantage Rate Swap Examples

-------------------------------------------------------------------------------------------------------------

USD/JPY 63.8 60.8 84.6 0.010 78

XAU/USD 70.4 68.1 60.0 -0.012 20

EUR/USD 71.5 72.7 7.1 -0.005 14

GBP/JPY 56.8 56.1 71.4 0.008 14

AUD/CAD 73.8 73.9 45.5 0.004 11

EUR/JPY 62.8 72.4 60.0 0.004 6

GBP/USD 76.8 78.3 50.0 0.000 4

AUD/JPY 65.3 65.6 0.0 0.009 2

CHF/JPY 64.3 61.9 100.0 -0.003 2

EUR/CHF 80.9 76.5 50.0 0.004 2

EUR/GBP 70.0 71.2 0.0 -0.007 2

GBP/CHF 69.4 72.1 0.0 0.008 1

USD/CHF 84.3 84.2 100.0 0.007 1

-------------------------------------------------------------------------------------------------------------

Let’s take a closer look at the six currency pairs with more data above. Swaps are clearly favorable for USD/JPY, GBP/JPY, EUR/JPY, while EUR/USD with negative swaps is favored for selling. AUD/CAD, popular for its carry and tendency to be less trend-prone, shows little difference by trading direction. By contrast, XAU/USD, despite holding physical gold yielding no interest, shows the strongest buy-side advantage, yielding the largest negative swap.

I attempted to download backtest data for USD/JPY buy-favored EAs, but access requires purchase, so I gave up.

I also develop various EAs, so I tested the effects of restricting trading direction through backtests (2025/07/01-2026/06/30, USD/JPY 0.1 lot). The results are shown in the table below.

---------------------------------------------------------------------------------

EA Name Trades Net Profit Win Rate pf

(Yen) (%)

---------------------------------------------------------------------------------

OTR2501 355 67,947 50.14 (53.81/43.94) 1.10

OTR2501L 286 87,635 53.15 1.16

OTR2501S 191 -100,035 42.93 0.78

OTR2502 262 38,249 49.62 (57.03/42.54) 1.09

OTR2502L 138 100,530 59.42 1.55

OTR2502S 154 80,000 46.75 1.03

OTR2503 150 132,369 58.67 (62.64/52.54) 1.64

OTR2503L 96 104,977 62.50 1.94

OTR2503S 67 -7,191 50.75 0.94

OTR2504 306 6,136 49.67 (52.98/45.65) 1.01

OTR2504L 204 68,904 52.45 1.19

OTR2504S 186 -112,948 44.62 0.74

OTR2515 204 83,294 53.43 (57.76/47.73) 1.22

OTR2515L 129 69,937 54.26 1.31

OTR2515S 95 24,930 49.47 1.14

OTR2608 350 -20,245 49.43 (54.45/43.40) 0.97

OTR2608L 226 104,129 53.98 1.26

OTR2608S 192 -139,675 42.71 0.71

---------------------------------------------------------------------------------

All EA names that are limited to buying trades are labeled with ***L, and those limited to selling with ***S. The win rates in parentheses are (buy trade win rate / sell trade win rate).

Restricting trading direction can significantly improve EA performance. The backtest results do not account for swaps, so the real difference would be even larger.

One thing I often feel when running an EA is that after a string of losses, I wonder if this EA can win in the long run. Before completely stopping operation and giving up, please consider restricting the trading direction. It can improve performance somewhat and at least halve the losses.

Some EAs may already have a built-in trading-direction restriction feature. Since it is very easy to program to stop only one side of trading, you can ask the developer to implement it.

If an EA does not have a trading-direction restriction feature and the developer will not modify the program, I have created and am selling a simple workaround to trade in a restricted direction (approximately):cancel trade EAPlease feel free to use it. Also among my EAs above, the backtested results are favorable forOTR2503, OTR2515, OTR2608L, which are also listed for sale as potential candidates for your EA portfolio.。