Analysis of Corporate Bond Issuance and Yen Cash Flows - Detailed Explanation

Issuance of Western corporate bonds in Japan

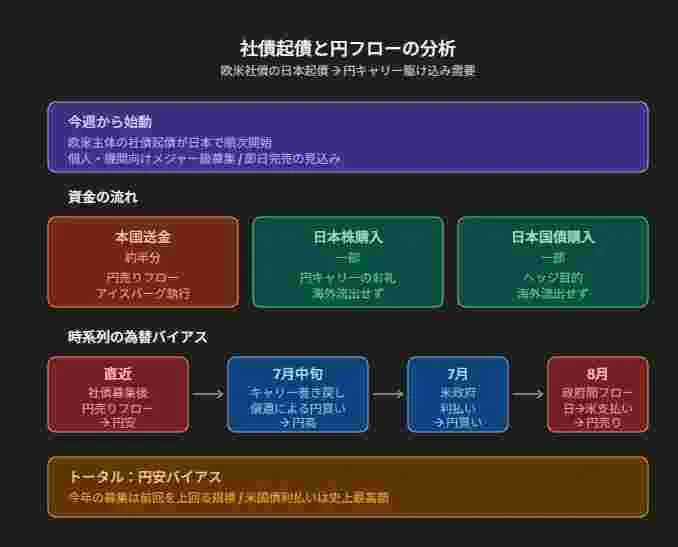

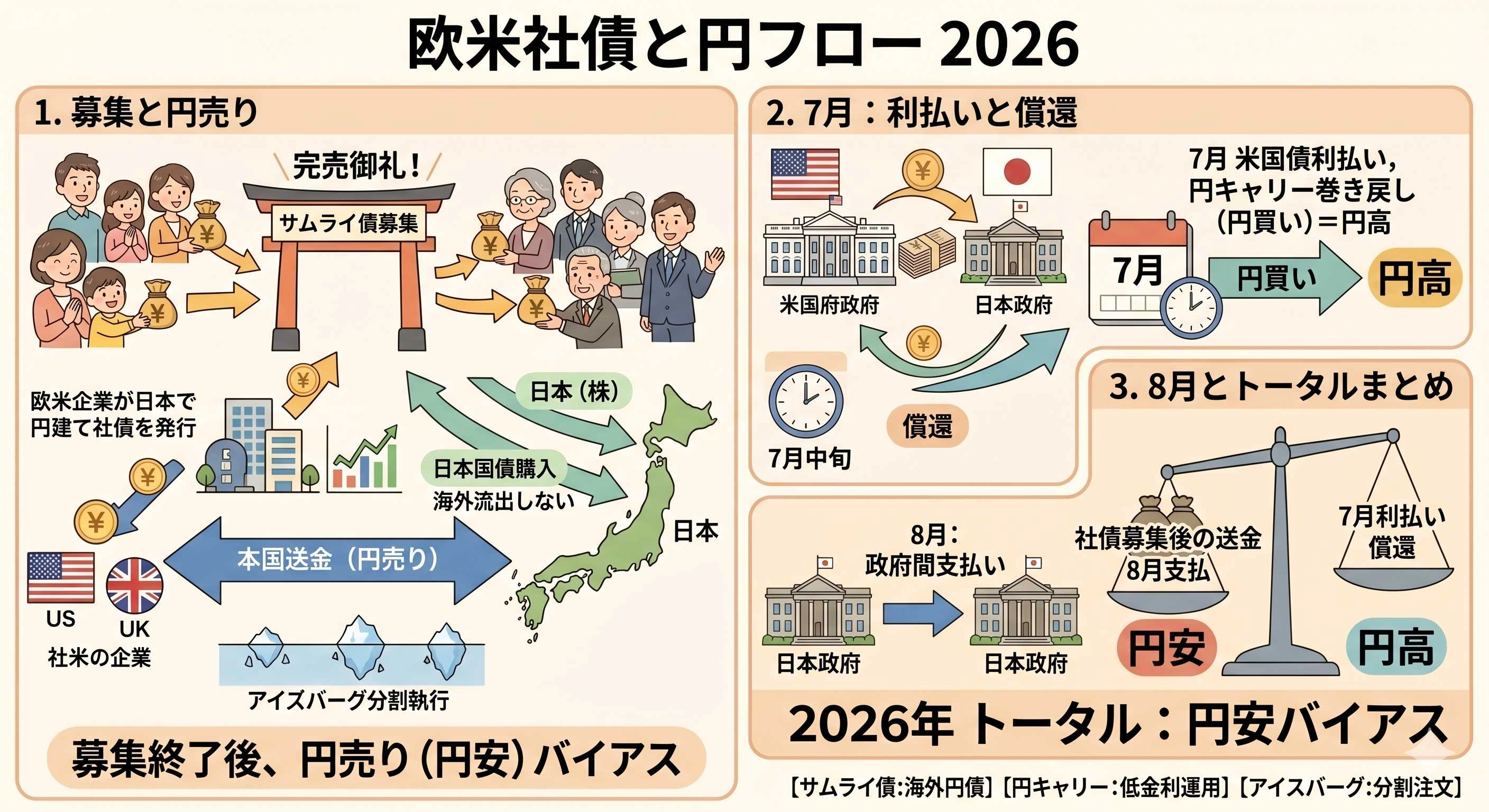

Bond issuances led by Western entities are beginning in Japan in sequence. Since February this year, there have been sporadic issuances for institutions, but this time it is a major offering aimed at both individuals and institutions.

This is rush demand driven by yen carry trades. Western companies seeking to borrow in low-interest yen are issuing yen-denominated corporate bonds in Japan (Samurai bonds).

Expected to be sold out on the day

Something similar happened 3-4 years ago, and it sold out immediately then. This time too, it is expected to close with “sold out” without waiting for the deadline (roughly two weeks to several weeks).

Fund flows: what happens after the fund-raising

Outflow of yen selling

In this type of movement, after the offering (buying bonds in Japanese yen), the collected yen is immediately remitted back to the home country (the West).

| Use of funds | Proportion | Impact on FX |

|-----------|------|-------------|

| Remittance to home country (to the West) | about half | Yen-selling flow occurs |

| Purchase of Japanese stocks | part | No overseas outflow |

| Purchase of Japanese government bonds | part | No overseas outflow |

For the portion used to buy Japanese stocks and Japanese government bonds, there is no overseas outflow as gratitude for yen carry (or as hedging). Still, yen-selling flow equivalent to the募集 amount emerges in various places.

Iceberg-like execution

Most of it takes iceberg form. This is a method of splitting a large order into small pieces and executing it gradually so as not to alert the market. Like an iceberg, only a portion is visible.

Reversal of yen carry

The redemption of bonds issued 3–4 years ago is also due to occur later. This is the reversal of yen carry.

At redemption, Western companies must exchange domestic currency into yen to repay yen-denominated bonds, generating yen-buying flow.

Timing expectations

| Item | Content |

|------|------|

| Initial peak expectation | Mid-July |

| This time’s expectation | Diversify or time it to offset |

Because the scale of this yen carry is large, the timing of the reversal may be dispersed, and offsets may be made by aligning new fund-raisings and redemptions.

Total FX bias

As this year’s fund-raising exceeds the previous one, the FX trend will be as follows.

| Timeline | Flow | Impact on yen |

|--------|--------|-----------|

| Recently (post-bond issuance) | Yen-selling flow | Yen depreciation |

| Afterward | Reversal of yen carry | Yen appreciation |

| Total | - | Yen depreciation bias |

Recently, yen-selling flow after bond issuance, followed by yen buyback due to yen carry reversal, but overall it will bias toward yen depreciation.

Annual schedule of government-to-government flows

July: Interest payments by the U.S. government (yen-buying)

In July, on U.S.-government-held U.S. Treasuries, the U.S. government pays interest. This is a yen-buying flow.

August: Government-to-government flows (yen-selling direction)

In August, government-to-government flows occur, with Japan making payments to the U.S. government. This happens every year, so it should be included in annual plans and addressed as usual.

This year’s special factors

Record-high U.S. Treasury interest payments

This year’s U.S. government interest payments on Treasuries will be the highest ever. This is believed to be due to the front-loaded issuance of U.S. Treasuries during past events (e.g., the pandemic period) causing overlapping interest payments.

Actions of U.S. Treasury Secretary Yellen

As the deadlines approach, U.S. Treasury Secretary Yellen becomes more vocal. There will be more statements regarding fiscal and financing matters, potentially increasing market noise.

Glossary

| Term | Meaning |

|------|------|

| Issuance | The act of issuing new bonds |

| Samurai Bond | A yen-denominated bond issued by a non-Japanese issuer in Japan |

| Yen Carry | Borrowing low-interest yen to deploy in high-interest currencies |

| Reversal | Unwinding carry trades (yen buying) |

| Remittance | Foreign remittance |

| Iceberg Order | Method of hiding a large order by breaking it into smaller orders |

| Redemption | Maturity repayment of bonds |

Summary

| Timing | Event | FX impact |

|------|---------|-------------|

| From this week onward | Western corporate bonds issued in Japan | - |

| After fundraising ends | Yen-selling flow (home country remittance) | Yen depreciation |

| Then | Reversal of yen carry (redemption) | Yen appreciation |

| July | U.S. government interest payments | Yen buying |

| Mid-July | Reversal peak (diversification possible) | Yen buying |

| August | Government-to-government flows (Japan to U.S.) | Yen-selling direction |

| Total | - | Yen depreciation bias |

Recently, yen-selling flow associated with bond issuance is dominant, but follow-on yen carry reversal and July U.S. government interest payments also loom. It is advisable to understand the annual schedule of government-to-government flows and incorporate the usual responses into planning.