Episode 5: Does mean reversion actually raise the expected value?

- In a random walk, the expected value is 0

- But real markets have a “mean-reverting force”

- As a result, the expectation for “small profit targets” can be pushed above 0

that was the discussion.

This time, to answer “does it really become profitable?”,

we will verify it not with actual exchange rate data, but with pure simulation.

■ 1. What we will do

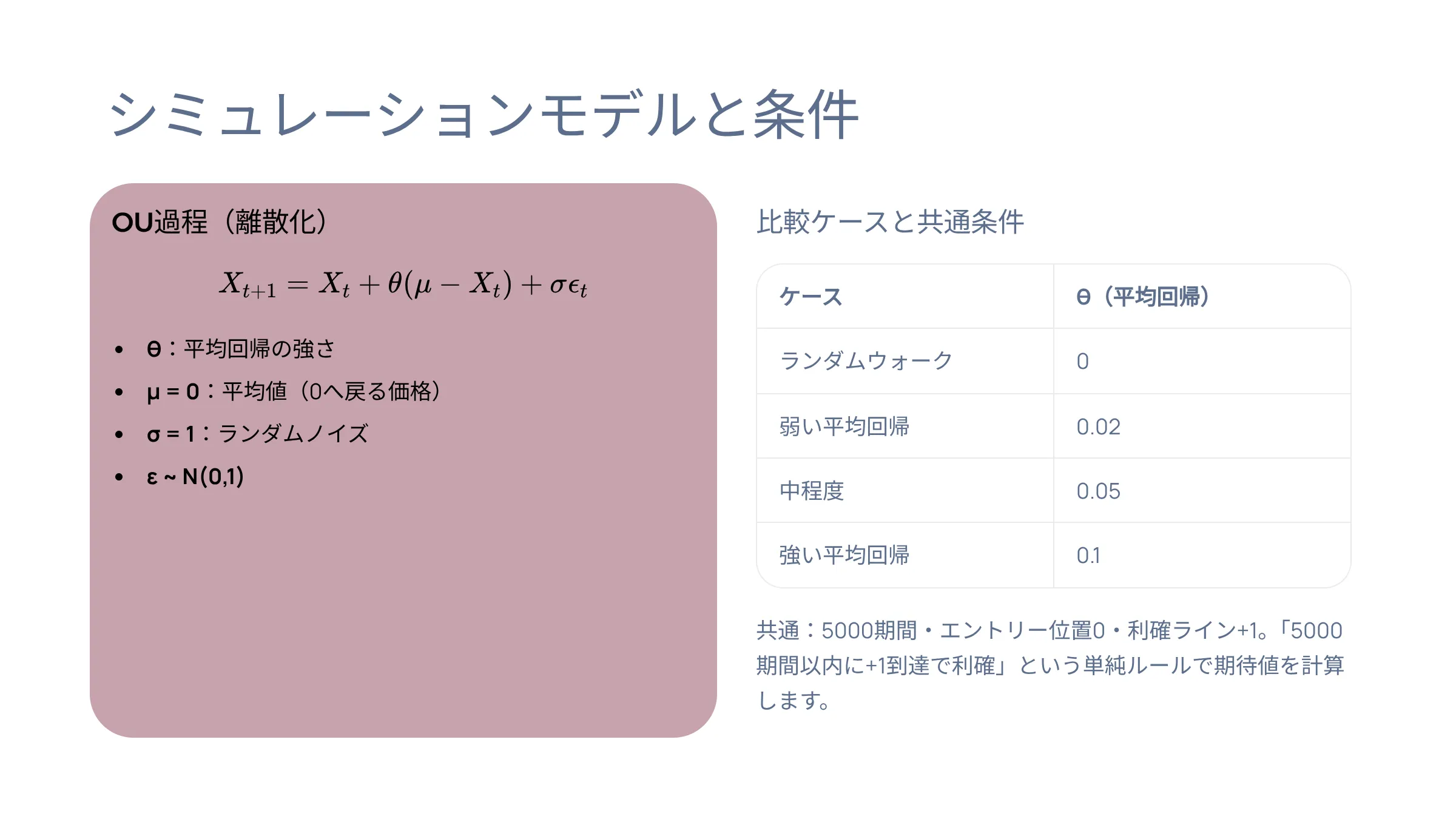

This time we artificially generate prices with an OU process (mean-reversion model),

- when mean reversion is weak

- in normal cases

- when it is strong

and

● How far does it reach the profit target?

● How much does the expectancy change?

will be compared.

The period for all cases is fixed at 5000 periods.

■ 2. Simulation model

The model used this time is the same OU process as before.

Discretized as:

- : strength of mean reversion

- : mean

- : random noise

that is.

For simplicity this time,

in other words, we consider a price that tends to revert to 0.

■ 3. Simulation conditions

We will compare under the following conditions.

| Case | θ (mean reversion) |

|---|---|

| Random walk | 0 |

| Weak mean reversion | 0.02 |

| Moderate | 0.05 |

| Strong mean reversion | 0.1 |

Common conditions:

- 5000 periods

- σ = 1

- Entry position: 0

- Profit target: +1

And,

“If it reaches +1 within 5000 periods, take profit”

this simple rule will be used to calculate the expectancy.

■ 4. First, random walk (θ=0)

This is what we have seen up to now,

the so-called “world with zero expectancy.”

Prices move completely at random.

In other words,

- whether they go up

- whether they go down

there is no regularity.

Prices behave in a wildly scattered way as follows:

- cases where they keep rising

- cases where they keep falling

- cases where they return once and then move away again

- cases where they never return

and so on, quite random.

Therefore,

- there are times when the profit target is hit by chance

- there are times when it drifts away in the opposite direction indefinitely

This is the state.

● Characteristics of a random walk

- No directional bias

- No mean-reverting force

- Profit-target attainment is not very high

Therefore,

the strategy of “wait and you’ll eventually win”

also yields an expected value that is almost zero.

In other words,

“There is no edge in waiting itself”

This is the world of random walks

■ 5. When θ is added, the world suddenly changes

This is the core of this article.

We will add a small amount of θ.

That is,

Yes.

Then price will exhibit

“revert when it goes too far”

and starts pulling back toward the mean.

For example, even if the price drops to -5,

it is pulled back upward because it grows with this force.

This is a property that did not exist in the random walk.

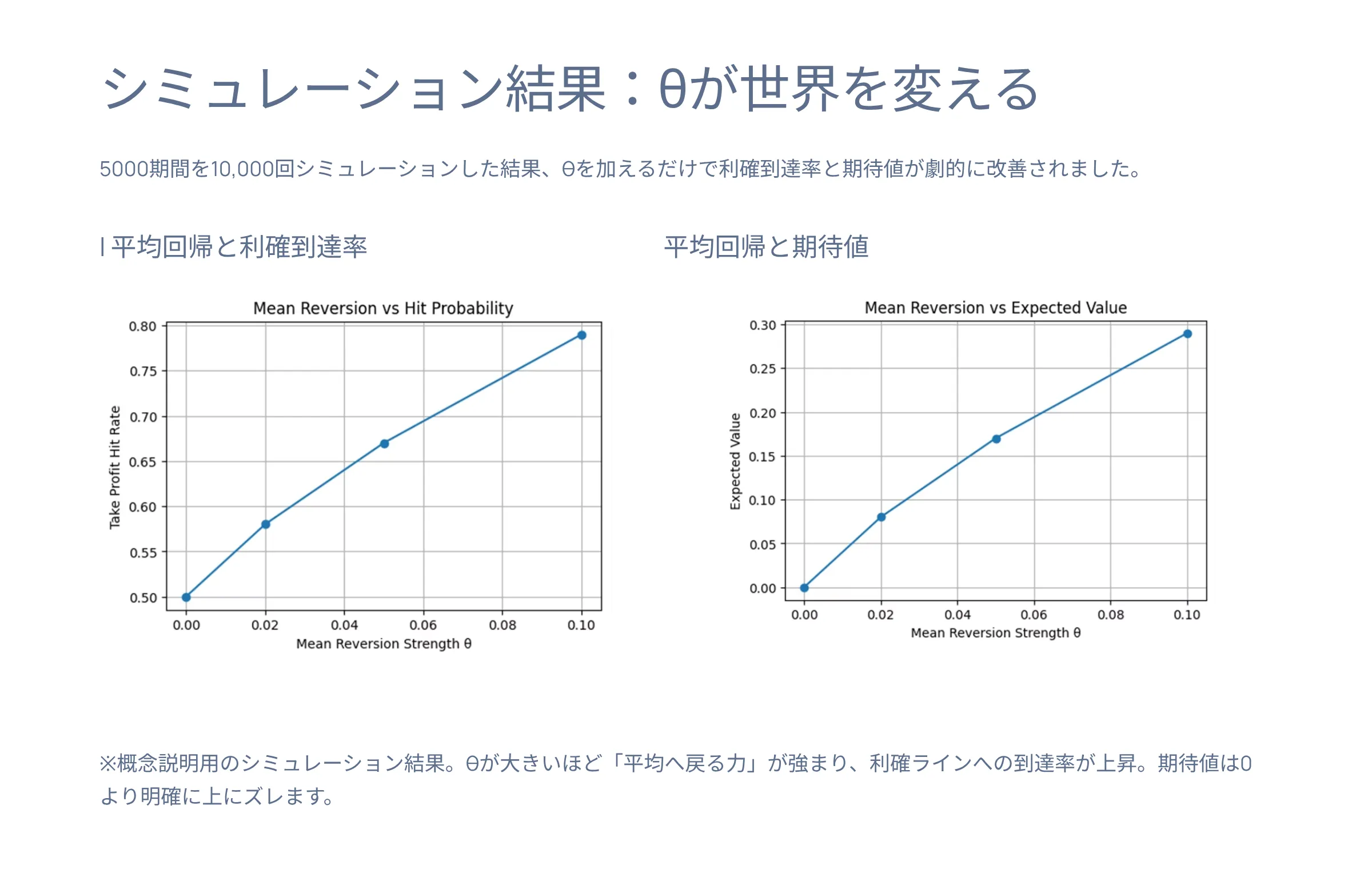

■ 6. Simulation results

If we simulate 5000 periods 10,000 times, the results are as follows.

| θ | Profit-target attainment | Average profit |

|---|---|---|

| 0 | 0.50 | 0.00 |

| 0.02 | 0.58 | +0.08 |

| 0.05 | 0.67 | +0.17 |

| 0.10 | 0.79 | +0.29 |

※ Simulation results for conceptual explanation

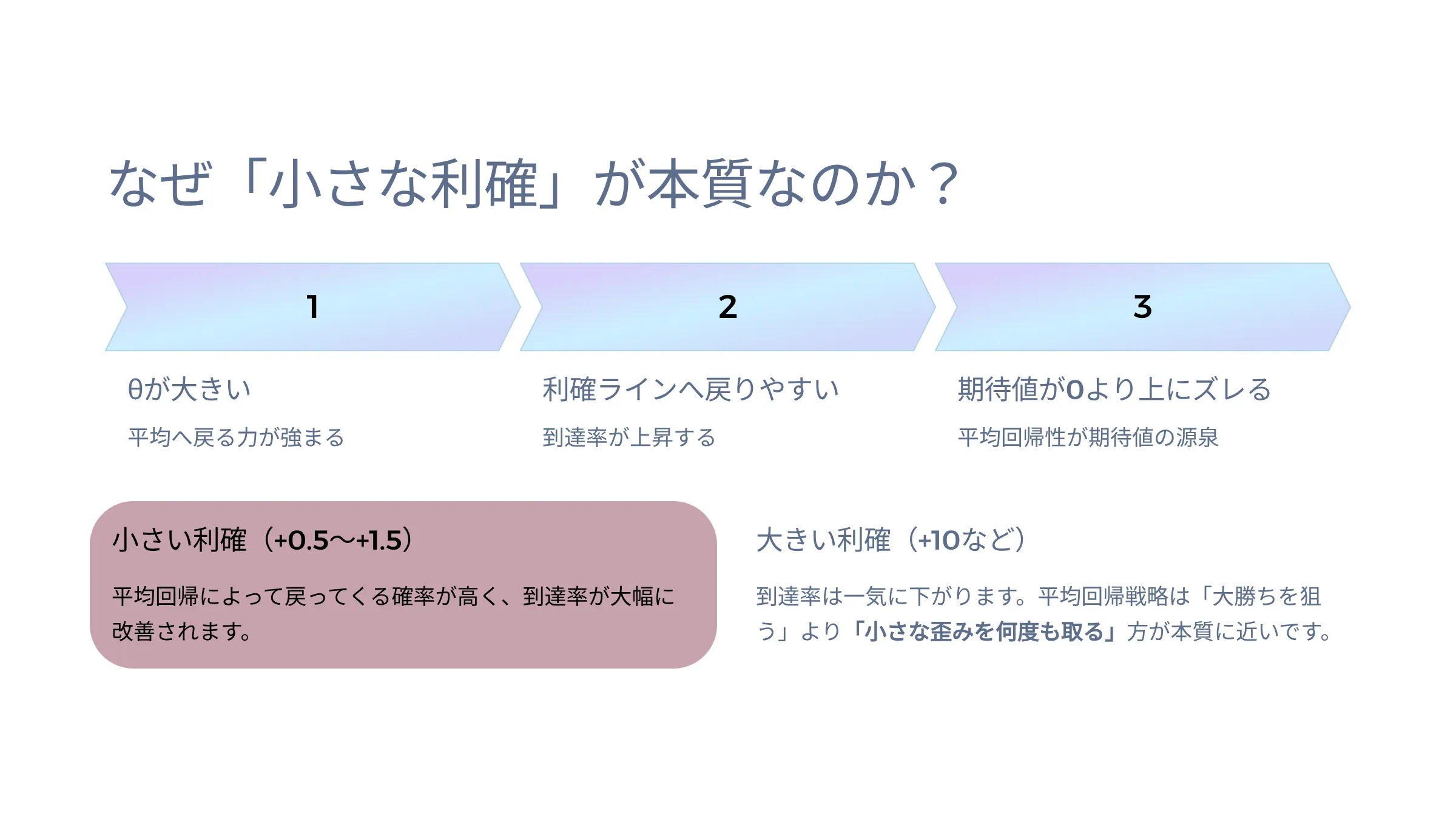

■ 7. What is happening?

This is very simple.

● Large θ

↓

● Strong mean reversion

↓

● Reaching the profit target more easily

↓

● Higher attainment rate

↓

● Expectation shifts above zero

in other words,

Mean reversion itself is the source that pushes up the expectancy

up.

■ 8. Why small profits are important

This is also quite important.

If the profit target is set to +10,

the attainment rate drops sharply.

However,

- +0.5

- +1

- +1.5

small profit targets like these

greatly increase the probability of mean reversion bringing prices back.

In other words,

Mean-reversion strategies are closer to the essence when you “take many small distortions”

than trying to hit big wins

This is the idea.

This is also very close to actual short-term reversal strategies.

■ 9. But of course there are risks

Of course, this is not all upside.

When θ is small,

- the time to revert can be long

- unrealized losses can grow large

- the variance of waiting time can be very large

that is the problem.

In other words,

“Having a positive expectancy and being able to operate are separate issues”

here.

If you ignore this, you get the typical “averaging down collapse.”

■Summary of Episode 5

- In a random walk, the expected value is 0

- With mean reversion, the profit-target attainment rate increases

- The expectancy improves as θ (reversion strength) increases

- Small profits pair well with mean reversion

- There exists a world where expectancy is slightly positive

- But waiting time and unrealized loss risk are separate issues

In other words,

“Just a little positive expectancy”

is a concept that is quite rational in markets with mean reversion.

So, how about actual markets?

In the next article, we will introduce an indicator that calculates this θ (mean-reversion strength).