SoftBank (9434) has reached a 6% dividend yield. Can it achieve long-term growth by overcoming concerns about declining fees?

SoftBank, which listed in December last year (9434), faced network outages and a downturn in stock market sentiment immediately after the listing, and it continues to trade below the public price.

On the other hand, due to the decline in stock pricethe full-year dividend yield reaches 6%, which is attractive to income-focused investors.

Rising concerns about price reductions; a challenge for the entire industry

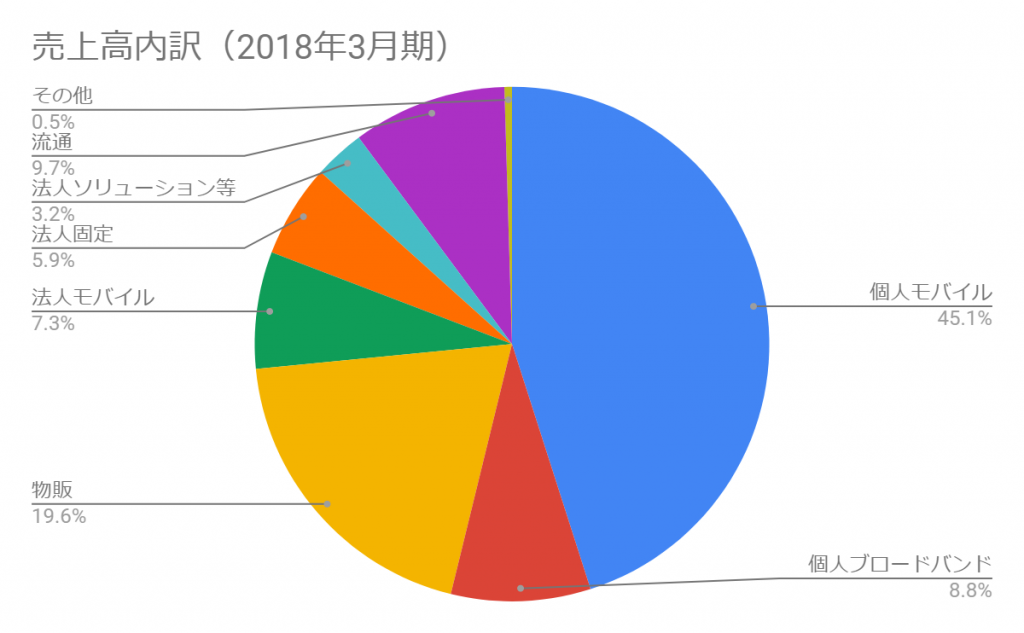

SoftBank is a subsidiary of SoftBank Group (9984) and handles mobile and fixed-line communications. The personal mobile business accounts for about half of its sales, and the personal business generates about 80–90% of its profits.

The line contracts boast 43 million contracts (Sum of SoftBank, Y! Mobile, LINE Mobile), from which enormous revenue is generated.The business outlook is relatively stable, one could say.

Yet the stock price has fallen becausepricing reductions are a rising concern. In addition to Rakuten entering the mobile carrier business in earnest, NTT Docomo has announced plans to reduce rates by 20–40% on some existing plans this coming April. The government has repeatedly criticized the persistently high mobile charges.

【Reference】Mobile call charges to be lowered, schedule becoming visible (Zaikai News)

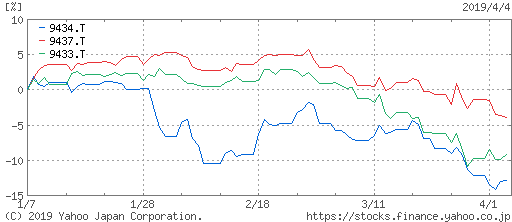

Because this is an industry-wide issue,NTT Docomo (9437), KDDI (9433) are also cutting prices. Among them, SoftBank has fallen by more than 10% in the past three months.

Mobile charges have been increasingly scrutinized over the past 1–2 years. One reason is that with the spread of smartphones, the absolute amount paid has risen.

In fact,the rise of low-cost carriers (MVNOs) continues. While the major carriers’ rates have not fallen dramatically, it is no longer feasible to ignore them forever.

In response, SoftBank owns within its group budget carriers such as Y! Mobile and LINE Mobile, and au has UQ Mobilethese help retain contract numbers while pushing down the per-unit price.

What is worrisome is not only the decline in revenue from pricing.

In 2020, as 5G, the ultra-fast, large-capacity communications, is expected to become fully operational,the 5G is expected to operate in earnest. Carriers must invest accordingly, and those costs are unavoidable.

Amid this, Chinese Huawei products, which had provided relatively inexpensive, high-quality equipment, are becoming harder to use due to American pressure. It is inferred that SoftBank used many Huawei devices, as evidenced by advertisements on baseball team uniforms.

If investment costs rise, at least in the short term, there could be negative impacts on earnings.

Technology advances in communications networks, and internal cost reductions

On the other hand, let's consider a somewhat longer-term perspective.

The biggest asset of mobile carriers is their enormous customer base and nationwide network = base stations. These become indispensable as 5G and IoT (Internet of Things) are used more widely.

For example, autonomous driving requires 5G, so in addition to mobile contracts, additional contracts are expected.One person will need two contracts: mobile phone and car.

In the nearer term, simply by moving to 5G, it is possible to raise contract fees. In the past, prices increased each time from 3G to 4G. As smartphones have become inseparable from daily life, this price increase is likely to be accepted.In other words,investing in 5G is likely to be recovered through increased contracts and higher charges.Also, the most costly part of network investment is securing locations, butsince base stations are already secured, it is sufficient to erect antennas atop them. This can significantly reduce costs compared with starting from zero.Additionally, I am focusing oncost reduction.SoftBank states it will greatly improve operations and reduce costs by using AI and RPA. For a company of this scale, the cost-reduction impact is immeasurable.With 20,000 employees, for example, using RPA to halve this number is not impossible. If average annual salary is ¥7.5 million, reducing 10,000 employees would save ¥75 billion. The impact on operating income of ¥6.4 trillion would be substantial.Of course, this will not happen overnight, but effects should gradually appear.Sustained profit growth. If that can be achieved, long-term investors have nothing to complain about.Risks lie in net debt and parent company trends. Can earnings improve and continue high dividends?Notable risks include3.3 trillion yen in interest-bearing debt. Historically, debt has been used to expand the scale when favorable.If interest rates rise in the future, there could be burden from interest payments, but I think the probability is low.In a low-growth Japan where the natural interest rate is low, there is little sign of global rate increases.If debt is repaid steadily, interest costs can be reduced. Of course, given this company’s tendency, it cannot be ruled out that while rates are low it may increase borrowings to pursue expansion, but that is now the role of the parent company.That parent company still holds more than 60% of voting rights and controls management. Its intent will determine things, for better or worse.For the parent company,the mobile business is a valuable source of income. It will likely accelerate fund investments and further strengthen cash-generating power.Having secured substantial funds through the listed subsidiary’s stock sales, it will likely refrain from selling shares for a while and instead raise funds through dividends. In that regard,a high payout ratio of around 85% is likely to be maintained.Additionally, for further sales, boosting the stock price is a major objective. To that end, boosting earnings is a top priority.Therefore, earnings improvement is essential.Of course, on the other hand,concerns about supply and demand deterioration due to future equity salesremain. Therefore, a short-term large rise should not be expected. A long-term view based on ongoing earnings improvement and high dividend levels is warranted.Current dividend yield is 6% on a full-year basis. If the payout ratio of 85% is maintained and earnings improve, even higher levels can be expected. At the same time, in a downturn, dividends may also fall, but in the long run this could present a buying opportunity.A 6% yield is among the highest in Japan.Very few REITs match this. As a neglected high-dividend stock, I will continue to monitor its trajectory.※Tsubame Investment Advisory’s websitePlease also take a look.

In other words,investing in 5G is likely to be recovered through increased contracts and higher charges.

Also, the most costly part of network investment is securing locations, butsince base stations are already secured, it is sufficient to erect antennas atop them. This can significantly reduce costs compared with starting from zero.

Additionally, I am focusing oncost reduction.

SoftBank states it will greatly improve operations and reduce costs by using AI and RPA. For a company of this scale, the cost-reduction impact is immeasurable.

With 20,000 employees, for example, using RPA to halve this number is not impossible. If average annual salary is ¥7.5 million, reducing 10,000 employees would save ¥75 billion. The impact on operating income of ¥6.4 trillion would be substantial.

Of course, this will not happen overnight, but effects should gradually appear.Sustained profit growth. If that can be achieved, long-term investors have nothing to complain about.

Risks lie in net debt and parent company trends. Can earnings improve and continue high dividends?

Notable risks include3.3 trillion yen in interest-bearing debt. Historically, debt has been used to expand the scale when favorable.

If interest rates rise in the future, there could be burden from interest payments, but I think the probability is low.In a low-growth Japan where the natural interest rate is low, there is little sign of global rate increases.

If debt is repaid steadily, interest costs can be reduced. Of course, given this company’s tendency, it cannot be ruled out that while rates are low it may increase borrowings to pursue expansion, but that is now the role of the parent company.

That parent company still holds more than 60% of voting rights and controls management. Its intent will determine things, for better or worse.

For the parent company,the mobile business is a valuable source of income. It will likely accelerate fund investments and further strengthen cash-generating power.

Having secured substantial funds through the listed subsidiary’s stock sales, it will likely refrain from selling shares for a while and instead raise funds through dividends. In that regard,a high payout ratio of around 85% is likely to be maintained.

Additionally, for further sales, boosting the stock price is a major objective. To that end, boosting earnings is a top priority.Therefore, earnings improvement is essential.

Of course, on the other hand,concerns about supply and demand deterioration due to future equity salesremain. Therefore, a short-term large rise should not be expected. A long-term view based on ongoing earnings improvement and high dividend levels is warranted.

Current dividend yield is 6% on a full-year basis. If the payout ratio of 85% is maintained and earnings improve, even higher levels can be expected. At the same time, in a downturn, dividends may also fall, but in the long run this could present a buying opportunity.

A 6% yield is among the highest in Japan.Very few REITs match this. As a neglected high-dividend stock, I will continue to monitor its trajectory.

※Tsubame Investment Advisory’s websitePlease also take a look.