Wow... Yahoo's stock price is too low... Will the expansion of the commerce business turn out to be a good omen or a bad sign?

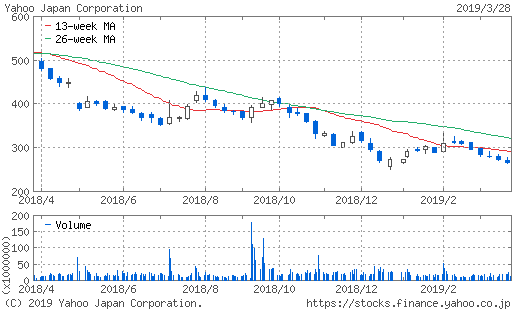

Yahoo Japan Corporation (4689) has fallen sharply in value.It has roughly halved in the past year.

Store opening fees abolished, PayPay 100 billion yen campaign, etc., leading to lower profits

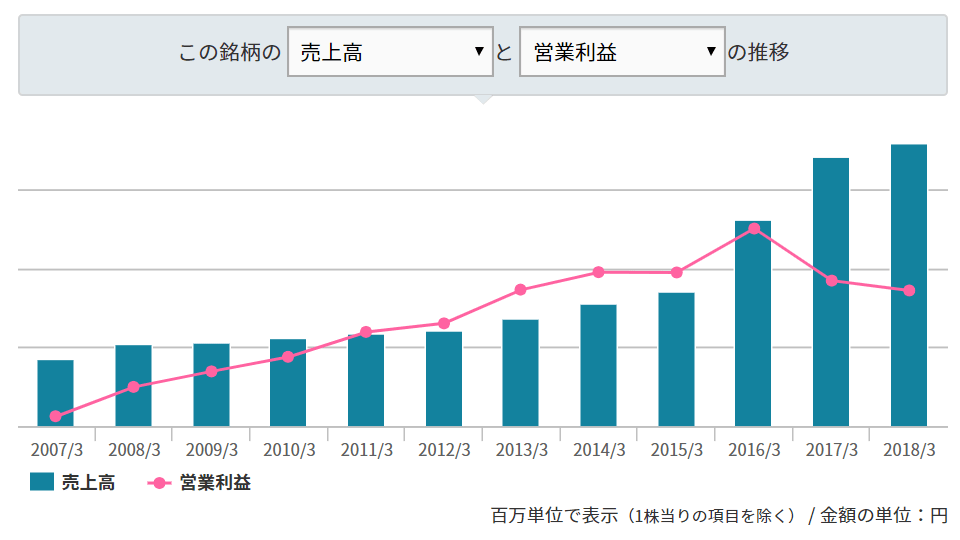

The reason for the decline is probably that profit growth has stopped. In the fiscal year ending March 2017,the 19-year streak of rising sales and profits stopped.

Sales are growing, sothe cause of the profit decline is rising costs. Yahoo! JAPAN has steered from stable operations toward expansion investments that incur costs.

The targets of investment arethe commerce fields such as shopping and payments (PayPay). They have been very generous, such as making Yahoo! Shopping store fees free and distributing 100 billion yen through PayPay campaigns.

If so much cost is spent, profits will naturally decline. The fact that this trend continued for two consecutive years has prevented a cap on the stock price decline.

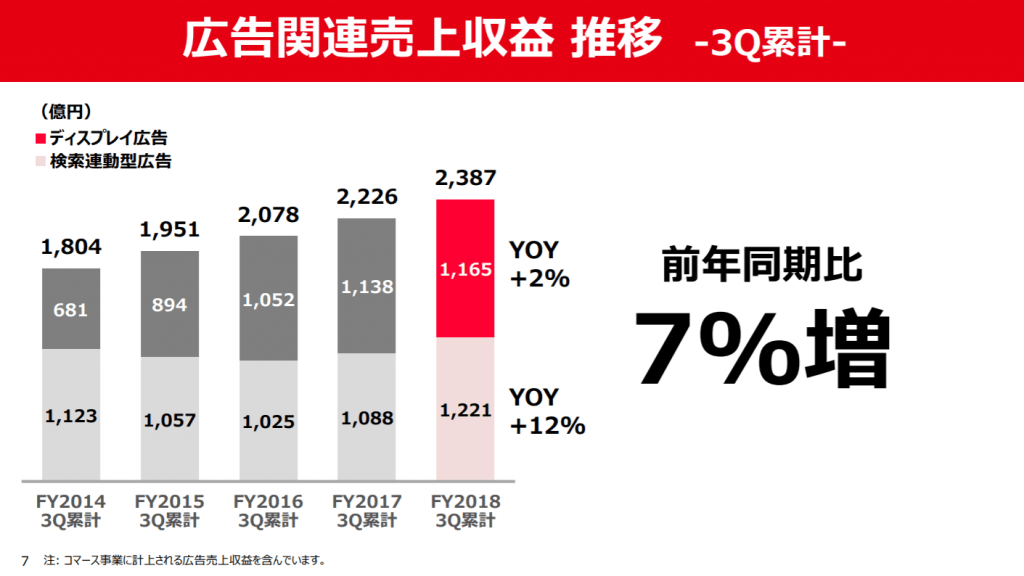

On the other hand,the traditional mainstay, the advertising business, is performing well. Even as internet viewing shifts from PC to smartphone, Yahoo! Japan has kept up smoothly without falling behind.

To allocate the profits earned from a stable advertising business to investments in future growth areas isa perfectly reasonable corporate strategy. Even if profits temporarily decrease, long-term investors should tolerate it.

Investments are good, but where will profits come from?

The future direction is concerning.

Shopping and PayPay arenot directly lucrative. Moreover, in a field crowded with competitors like Rakuten, Amazon, LINE, and Mercari, they are pursuing market share through cost leadership. Is there a clear path beyond that?

【Source】FY2019 Q3 earnings briefing

One possible scenario isstrengthening the financial business. Ant Financial, which leads mobile payments in China, manages payment data and enables small personal loans. By linking customer data with finance, it could lead to a powerful business opportunity.

However, there remains doubt as to whether this can be applied in Japan. There is sensitivity because customer data in Japan has previously been criticized when it was possible to identify individuals, so a system that ranks individuals could provoke backlash.

Furthermore, in Japan, people who want to borrow money have traditionally turned to consumer finance or bank card loans. Japan does not seem to be as gravely financially strapped as China, andRakuten is far ahead in the financial field.

In the advertising business, the stock looks cheap and could rise quickly if something hits

The future remains unclear, but the conventional advertising revenue provides support. It has succeeded in adapting to smartphones and continues to grow.

This sector is a so-called “money tree” and can continue to generate profits with minimal additional costs.

If no one threatens its position, past performance is informative. The PER based on the peak earnings achieved in the fiscal year ending March 2016 is about 9 times at the time of writing. Also, applying last year’s results yields about 12 times, which is a low level.

In short, even if new businesses do not generate profits, the stock remains very cheap.If even one new business hits, the stock price is likely to rise more than expected.

At present, the stock is highly undervalued, so I will carefully assess including the direction of new businesses.

※ is also recommended for viewing.