Today's macro correlation "The market is in a calm tension" 【February 27, 2026】

― Reallocation of funds occurring as the credit market remains quiet ―

■ Introduction: The market in a “quiet tension”

In late February 2026, while the ambiguity surrounding the Iran nuclear talks smolders, the market appears calm at first glance.

However, when looking across assets, there is a nuanced “midstate” that is neither purely risk-on nor risk-off.

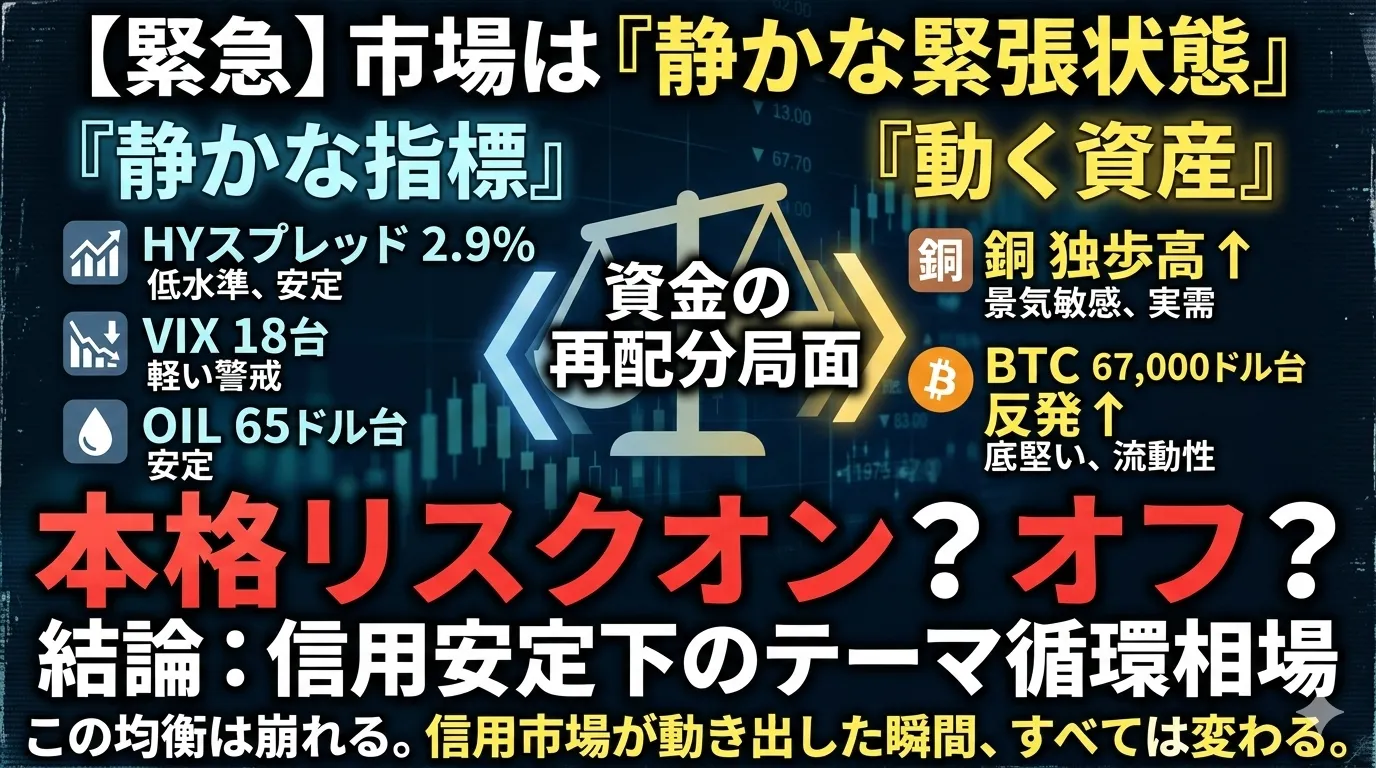

Current major indicators are as follows.

Nuclear talks: risk of breakdown existing

Gold and silver: unable to rise, capped

Copper: advancing on a solo basis

OIL: in the 65-dollar range

HY spread: 2.9%

VIX: in the 18s

SKEW: in the 140s

BTC: rebounded in the 67,000-dollar range

This combination is highly suggestive.

■ ① Will nuclear talks fail? The market deems the risk as “limited.”

Geopolitical risks around the Iran nuclear talks remain opaque, but market reactions are limited.

In a truly crisis-embedded phase,

oil would surge

gold would surge

HY spread would widen

VIX would spike

simultaneously.

However currently,

OIL is stable in the 65-dollar range (as of now).

Gold is stalling.

HY is at 2.9% at a low level.

This signals that the market has not fully priced in a comprehensive supply shock.

■ ② Reasons why gold and silver cannot rise

Typically, gold is bought when geopolitical risks rise.

But currently,

gold is capped.

silver also lacks upward momentum.

The backdrop for gold not rising includes

real yields not falling sharply

credit markets are stable

no signs of systemic crisis

in other words,

the psychology of “no need to rush to buy insurance” dominates.

■ ③ What copper’s solo rise means

Copper is considered a bellwether for the economy, known as “Dr. Copper.”

Currently, copper is rising on its own.

Possible drivers include:

AI data center demand

power infrastructure investment

China stimulus expectations

and other real-demand themes being recognized.

The combination of gold not rising and copper rising may indicate

a shift of funds from defensive assets to cyclical, economically sensitive assets.

■ ④ The stability of oil in the 65-dollar range—what it signals

Oil stabilizing in the 65-dollar range is also important.

Geopolitical tensions exist, but

supply concerns are limited.

Demand remains solid but not explosive.

Unless oil surges,

the inflation re-ignition scenario retreats.

As a result, financial conditions are unlikely to trend toward excessive tightening.

■ ⑤ HY spread 2.9%: credit markets are calm

This is the key point.

HY spreads at 2.9% are historically quite low.

Benchmarks:

Above 3.5%: warning level

4–5%: clear risk-off

6% and above: recession concerns

Thus far,

credit anxieties are hardly priced in.

This is the main reason why equities have not big-crashed.

■ ⑥ VIX in the 18s: mild vigilance remains

VIX in the 18s is not a fully safe zone.

Below 15: safe

18–20: mild vigilance

Above 25: stress level

Currently,

not fully risk-on, but not in crisis either

— in an intermediate zone.

■ ⑦ SKEW in the 140s: tail risks are moderate

SKEW indicates the concern for large drops or “black swan” events.

110–130: normal

140s: slightly cautious

150+: strong caution

Currently,

hedged to some extent, but not panicking

yet.

■ ⑧ BTC is 67,000 dollars—is it a bottom?

BTC corrected temporarily but has stopped declining around 67,000 dollars.

Key points are:

HY is stable

VIX has not spiked

Gold has not surged.

In other words,

an environment without systemic risk

BTC currently has a three-sided character:

a liquidity asset

a high-beta asset

and a partial digital gold

and as long as the credit market remains stable, it is unlikely to break down significantly.

We see a strong possibility of a bottom.

■ For now, it is an “equilibrium market”

The current market has no fear

nor excessive optimism.

Credit is stable,

spot/future rotation among commodities is occurring.

This can be interpreted as a

“funds reallocation phase.”

■ The Next Branch Point

Key points to watch are,

whether HY exceeds 3.5%

whether VIX drops below 17

whether copper highs persist

whether gold resumes an uptrend

.

The next trend will be decided here.

Current macro correlations show that

geopolitical risk is priced in only to a limited extent.

Credit markets are extremely stable.

Commodities are copper-led by real-demand themes.

Stocks have not collapsed,

BTC is holding steady.

This is a theme cycle under “credit stability.”

Even in a genuine risk-off,

it is not a full risk-on either.

A quiet equilibrium state.

However, this balance is not eternal.

The moment the credit market moves, correlations will break down all at once.

Now, is this the eve of that, or is the stability to continue?

From here, attention should also be paid to the credit markets.

× ![]()