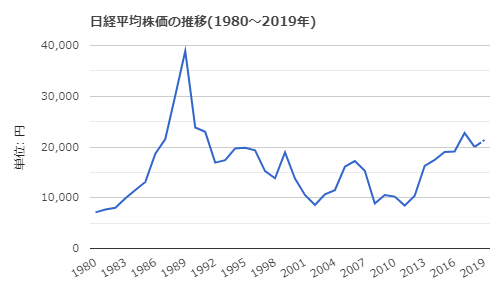

In the 30 years of the Heisei era, the Nikkei Stock Average did not grow at all. Consider the difference from U.S. stocks that have increased tenfold and the investment strategy going forward.

Annual return on stock investments is about 7%is often said. With the compounding principle of reinvesting dividends,the calculation is that it will double in 10 years.

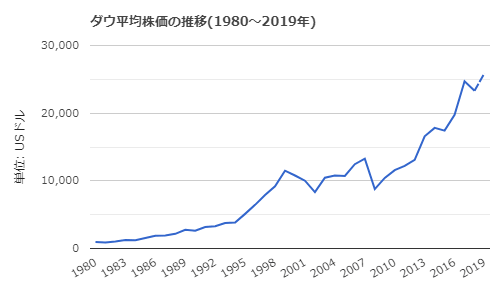

Dow Jones up 10x, Nikkei 225 unchanged

If you had invested in the Dow Jones in 1990, it would have grown about 10 times over 30 years.The annual return is 8.0%, which is almost the statistical figuresince dividends reinvestment is not included, the actual return could be higher.

So, what about the Nikkei Stock Average? If you had invested in 1990, it would be exactly at about the same level now (0%)after 30 years have passed.

You might be thinking, “Your statements contradict each other.” Yes,the 7% annual return does not apply at all to the actual Nikkei stock average. This helps explain why stock investment isn’t popular in Japan.

Reasons the Nikkei didn’t grow

There are two main factors for this.

One isthe growth engine of Japanese companies weakened.

Japanese companies grew rapidly during the high-growth era, but when the bubble burst, a backlash followed withover-investment and the drawbacks of lifelong employmentemerging.

They were forced to deal with inefficient management and legacy assets,leaving little room to invest for growth.

Meanwhile,in the United States, IT giants like Apple and Google emerged, sweeping the era. The growth of these companies pushed up US stocks.

The second factor is that, around 1990,stock prices were too high.

1990 was toward the end of the bubble economy. Prices surged, and the price-earnings ratio (PER) reached as high as80 times. A PER of about 15 times is considered appropriate, so 80 times indicated a bubble about five times higher than normal.

If the PER in 1990 had been 15 times rather than 80, stock prices at that time would have been one-fifth of what they were. In other words,if the past stock prices had moved within a reasonable range, the price today would be about five times higher.

If it were five times higher over 30 years, the annual return would be 5.5%. This would be quite close to the theoretical value, as you can see.

What investment strategy should we take?

From two factors, it can be said thatinvesting in globally growing companies is more advantageous, so look worldwide for growth, and

no matter how high the expected valueyou must never chase overvalued stocks.

If you buy growing companies at appropriate prices, over time their stock prices will rise. In a year, returns may be small or negative, butover 5 or 10 years, stock prices will steadily rise.

The price-earnings ratio of Japanese stocks is currently about 13 times. This level is by no means high, and it is clearly different from 30 years ago.

At this level, there is no need to overthink. We shouldfind the next growing stock and invest, and hold it as long as the company grows.