There are limits to savings. The importance of investment is something I especially want to convey to young people

Everyone, are you investing? Looking at various surveys, about 30% of Japanese have investment experience. In other words,70% of the majority lead lives with no investment at all.

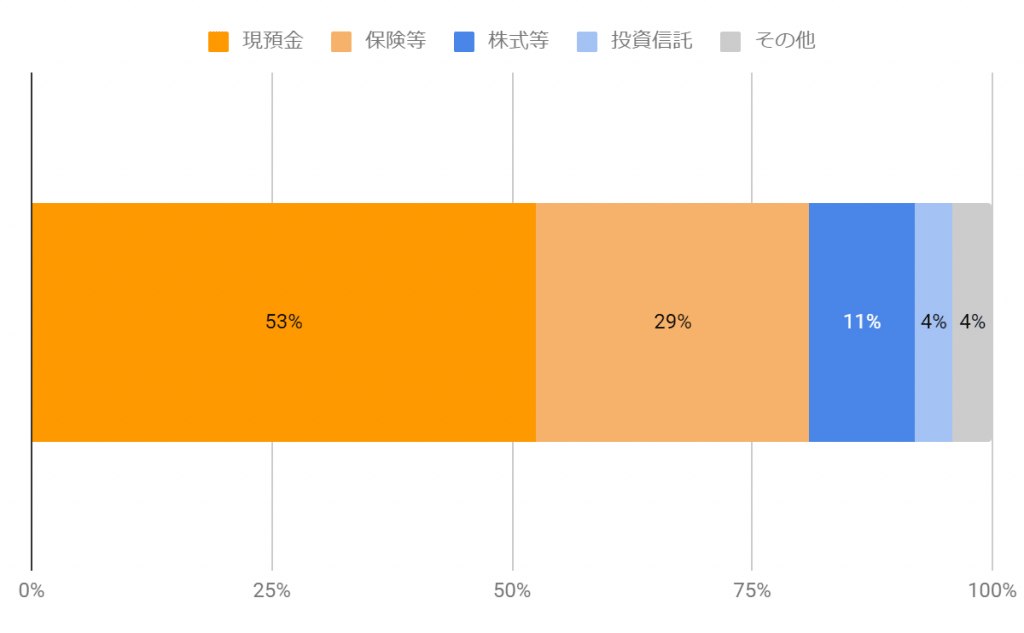

What are the limits of saving?

Among the 30% with experience, even fewer are still investing now. Excluding employee shareholding associations and defined contribution pensions, it might feel like only about 1 in 10.

For many people, the most representative method of asset formation is saving. Statistically,half of household financial assets are in cash and deposits.

Indeed, saving is an asset with a high sense of security. It never loses principal, and you can use it whenever necessary.

However, cash and deposits have a fatal flaw. That is,they will never increase. In this low interest rate environment, 1 million yen remains 1 million yen forever.

Suppose you are now 35 years old. If you save 1 million yen every year faithfully, by the time you retire at 65 you will have exactly 30 million yen. This isthe minimum financial asset level you would want to have at retirement.

What the “minimum” means isnot being able to waste. No matter how much free time you have, traveling abroad frequently may be just a dream.

Saving 1 million yen every year is quite a stretch for many people. Even continuing that for 30 years, you can only save the “minimum.”This is the limit of saving.

If you rely only on saving and pensions...

I had a colleague who worked as a public servant until retirement. He sent his three children to university and somehow paid off the mortgage on the house he bought 25 years ago.

He did not indulge excessively, saved like others. Upon retirement, there was also a path to reemployment, but he chose to pursue a freer life, left his job, received his severance, and entered pension life.

Part of the severance was used for house repairs. In these times of frequent disasters, that is necessary. The remaining money is 20 million yen.Exceeding the “minimum” level, the reliable source is only the pension. You can no longer waste money.

However,when trying to cut back in pension life, it is hard to muster resolve.

There is plenty of time, but domestic trips are once a year. We have not traveled abroad since our honeymoon. Our children have left home and live in the city. To see our newborn grandchild, we must wait for them to come home.

We live sufficiently within the range of pension, butwe cannot touch the 20 million yen “tiger cub” fund for emergencies. With life expectancy increasing, no one can be complacent. While this continues, we will join the later-stage elderly group.

Investment is a means to live a fulfilling life

There is data that Japanese leave behind an average of 30 million yen in financial assets at death. Among this, many people could not fully use the money that was saved for emergencies or to pursue things they love.

With a declining birthrate and aging population,Japan will become poorer in the future. This is not pessimism; it is a fact shown by the current situation.

Investing is,a means to live a fulfilling life while living in a poorer Japan.

In youth, you shouldmake your money work to increase the principal, and after retirement,dividends enrich life. When you start investing can greatly change your future life.

I wish for as many people as possible to live long, happy lives with accurate investment knowledge. Especially,I want to call out to the younger generation who have yet to live.