Two notable stocks in the nursing care industry

Caregiving Industryin Japan, where aging is progressing, is certain to expand. Companies that navigate this well have the potential to greatly increase their value.

Care businesses difficult to profit from

However, this industry is not easy. The reason is thatthe scale will grow, but profits are hard to come by. The factors are (1) the medical and nursing care insurance system and (2) a shortage of personnel.

A large share of caregivers’ sales comes fromcare benefits paid by the government. The benefit amount is determined by the user’s level of care needed. Users bear 10% of the benefit amount.

The number of users is certainly increasing, so overall volume will rise, but if it increases too much, the national finances cannot sustain it. With a fiscal situation already carrying unprecedented debt,there is constant pressure to restrain care rewards.

Operators are anxious about whether care rewards will go up or down. And for the government, to reduce fiscal burden while having them undertake care,the optimal solution is to keep operators in a state of “kept alive but not killed”.

If caregivers’ businesses start earning large profits, there will be talk of lowering care rewards. In other words,as long as revenue structure depends on the public care insurance system, large profit increases are unlikely.

Labor shortages are also severe. The effective job openings-to-applicants ratio for nursing care personnel is 3.6 times, much higher than the overall 1.4 times. Meanwhile,wages are at the lowest level across all industries, and the market principle is not functioning. This makes high turnover understandable.

The government also regards this situation as a problem and is trying to raise the wages for caregiving jobs. Recent increases in care rewards are in this context, andif businesses do not raise wages, they cannot secure talent. In such a situation, leaving profits behind is very difficult.

To find companies that can grow value in this field,a business model that does not rely on care rewards and can be rolled out nationwidemust be found. In this article, two such companies will be introduced.

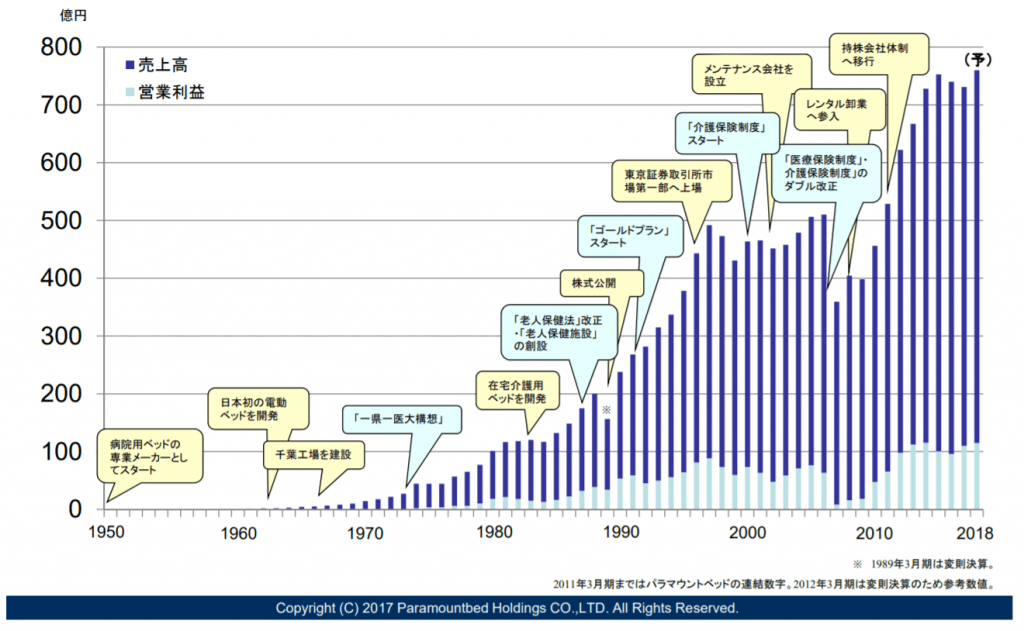

Paramount Bed HD (7817)

A company that has consistently manufactured medical and caregiving beds since its founding in 1950.Domestic market share is said to be about 60–70%, making it overwhelming.

Because it has continued to honestly produce beds suitable for caregiving,its technology and brand power are top-notch. Performance has also continued to grow steadily.

In caregiving, beds are indispensable. In facilities such as nursing homes, there is a steady demand. Recently, demand for home-care beds has also been increasing.

However, because bed rental is also covered by care insurance, it is essential to monitor policy trends. The damage if it becomes outside the system is not small.

As for future strategy, they anticipate increasing products for home use and expanding overseas, including China. However, thesecould fall into price competition. Paramount Bed is in the luxury category, and lower-priced competitors such as Nishimura (9843), Koizumi, and Platz (7813) are emerging. It is necessary to anticipate possible gradual erosion from these rivals.

PER is 18x, a somewhat high level compared to past trends. While stable earnings are expected,it is not particularly undervalued. I would like to keep an eye on it along with industry trends.

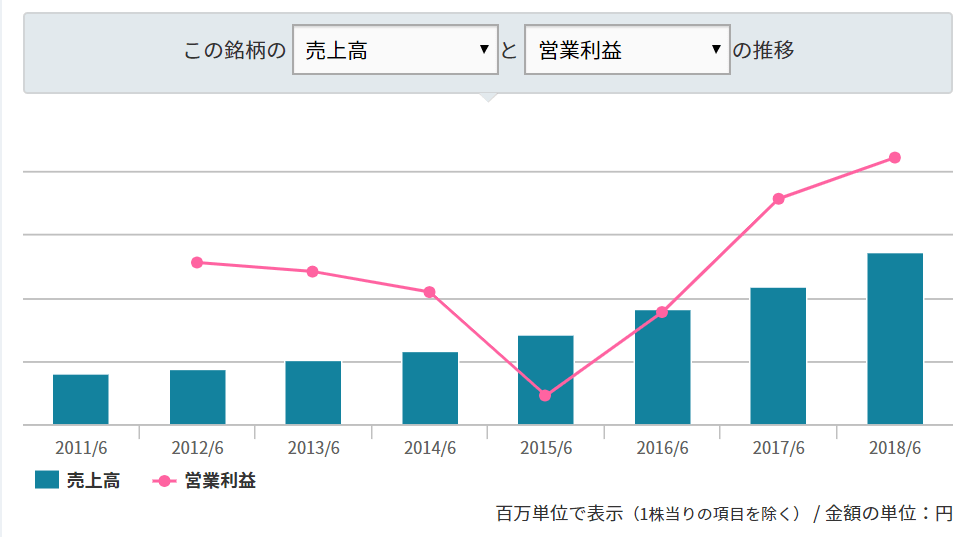

Charm Care Corporation (6062)

A company that operates paid elderly care homes in the Kansai region and the Tokyo metropolitan area. It originally belonged to the Subomura Construction group as one division, but has since become independent and is now listed on the First Section of the Tokyo Stock Exchange.

Their performance is soaring. Occupancy rates in homes exceed 97%, andthe more you build, the more sales and profits expand. The easing of lending practices and low interest rates in recent years have also likely contributed.

The characteristic here isa focus on operating homes. Many companies actively provide home-visit care, but as mentioned above, this is a business that is difficult to profit from. On the other hand, the sales of elderly homes are about half covered by nursing care insurance premiums, and the other half are rents and management fees—areas that do not depend on care insurance.

Running elderly homes has aspects of a real estate business. In other words, if you invest appropriately and maintain occupancy, it is almost certain to generate profits.

With this model, you do not need to profit from the care rewards portion. It functions as a cost center to raise occupancy, while profits come from the real estate portion.

And in the future, the company is expected to targetwealthy elderly people. By offering premium-feeling elderly homes, they can raise rents. This would reduce dependency on care rewards and improve profit margins.

Premium elderly homes appear to be a still-open market. After all, the elderly have money. Money cannot be taken to heaven, so it is not unreasonable to consider spending money on premium elder care to improve one’s retirement life.

Of course, competition will eventually intensify. The focus will be on how quickly they can establish their position by then.

PER is 23x, somewhat high, but given growth potential, there is not much overvaluation. Like real estate leasing, it offers stability, andit could be a stock to target if it falls due to some reason.