[Premium] Death of a parent × new tax system. The "tax-free alchemy" to circulate wealth within the family only

He is a certified FP1 who manages assets of 150 million yen. This time, if conditions align, I will teach a do-cheap method of “family internal money laundering (legitimate fund circulation)” that unleashes the strongest power.

The target is a household where there is a high-income husband, a stay-at-home wife, and parents who have surplus funds (dead money) to spare. It is the ultimate wealth defense measure: pay interest to banks and taxes to the nation becomes ridiculous.

Eliminate banks and establish a “family internal bank”

First, why is this scheme necessary? The reason is obvious. If I, as a high-income earner, buy real estate in my name, rental income will be taxed at the highest rate under the “comprehensive taxation.” On the other hand, the wife with no income cannot obtain financing from banks. And the parents are being exploited by securities salespeople.

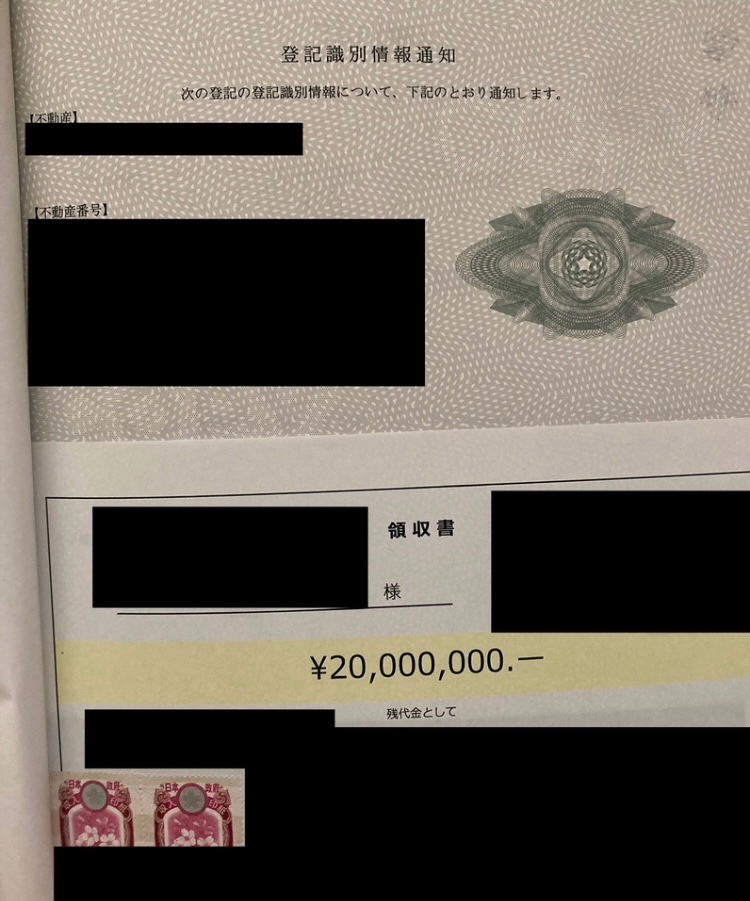

What solves these issues all at once is the establishment of a “family internal bank” that excludes others (banks). Specifically, purchase a 20 million yen income-producing property (yield 6%) in the wife’s name. Do not borrow funds from banks. I and the parents will lend 10 million yen each to the wife.

Where the money comes from and the repayment trick

The key of this scheme lies in the flow of money.

Loan terms:From me (husband) to wife: 10,000,000 yen at 0.5% interest. From parents to wife: 10,000,000 yen at 2.0% interest. The term is 10 years for both. A money loan agreement is mandatory.

Repayment to parents (income transfer):The wife will make principal-and-interest repayments to the parents from rental income (annual 1.2 million yen). The parents will receive about 200,000 yen in interest per year, which falls within the non-reportable range (below 200,000 yen).

Repayment to me (utilizing gifts):Here's the twist. The repayment to me is about 1.02 million yen per year. However, I give my wife an annual calendar-year gift of 1.1 million yen. The wife uses that gift to repay me. In effect, through actual fund movement alone, the wife’s debt is eliminated.

The destructive power of the 7th year of the Reiwa era’s new tax system

Furthermore, the 7th year tax reform strengthens the “increase in basic exemption (from 480,000 to 950,000)” which solidifies this scheme. Let’s look at the wife’s tax situation.

Rental income:1.2 million

Deduction power:Total 1.05 million (basic exemption 950,000 + blue return special deduction 100,000)

Expenses:Interest payments to parents and to me + property taxes, etc.

As a result, taxable income is zero or a large loss. No matter how you look at it, no taxes will be incurred. Naturally, the “130,000 yen wall” for social insurance is easily cleared, so there is no risk of losing dependents. The parents invest with high yields, the wife builds wealth tax-free, and future inherited assets can be compressed.

The ultimate cost cut and risk management

Even in property management, adhere to the cheapskate philosophy. I use a “lease-back” strategy, setting rents lower than market rate, while signing an agreement to “not do any repairs.” Furthermore, for properties with low building value, expensive fire insurance (building coverage) is unnecessary. If it burns down, just demolish and sell.

However, be sure to include “facility liability insurance.” If roof materials fly off and strike a passerby, the owner would be held strictly liable. Add this rider to the cheapest fire insurance. Saving a few thousand yen and bearing several tens of millions in compensation is not being frugal; it’s simply foolish.

Conclusion

All contracts should be electronic, and do not pay stamp tax. With this scheme, after 10 years, the wife will have[A device that generates 100,000 yen per month]without debt.

Fully utilize state systems to circulate wealth within the family. The obsession to not give even 1 yen to others (banks or the government) is the primary condition of a person who owns assets.