The blind spots of a couple’s loan. The wife goes bankrupt with “Rensei Group Credit Life Insurance”

This is an FP1 standard who operates assets of 150 million yen. In recent years, as housing prices have soared, there has been a rapid increase in "pair loans" where couples cooperate to take out a loan. Among them, "Joint Life Insurance with Survivorship (Joint Survivorship Life Insurance)" may seem like a loving system at first glance, since if one spouse dies, the loan could be wiped out in full.

However, this system hides a “worst trap” set by the National Tax Agency. If someone with no knowledge signs up easily, they will be further pursued by the tax office from the depths of grief after losing their partner.

Tax Trap That Looks Like Love

The scenario is this: the husband dies, and thanks to the survivorship life insurance, the mortgage is completely extinguished. The remaining wife, in her sorrow, might feel relieved, thinking, “At least the house loan is gone. Our living place is secure.”

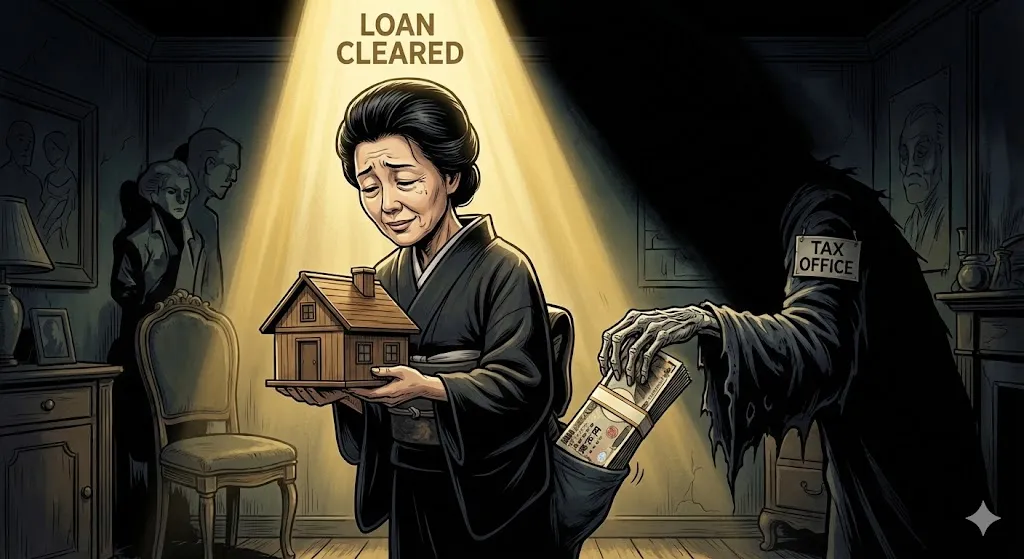

But then the tax office arrives mercilessly. “Madam, your husband’s death has also extinguished your portion of the debt, right? That is ‘income,’ so please pay income tax.”

Do you understand the meaning of this?

Income Tax When the Debt Vanishes Instantly

This is the blind spot. When the husband’s share of the loan is extinguished, it is treated as a settlement by life insurance and is usually handled within the scope of “inheritance” (or there is a tax-exempt threshold). The problem is the extinguishment of the wife’s own share of the debt.

If the wife’s debt is forgiven due to the husband’s death, from a tax perspective it is a “windfall,” treated as “economic benefit (miscellaneous income).” In other words, the wife is taxed on the benefit of “the debt being wiped out” with income tax and resident tax.

No Cash, Yet Taxes Arrive

The scariest part of this trap is that “there is not a single yen of cash on hand.” What comes in is an invisible benefit of “debt forgiveness.” But taxes must be paid in cash.

During the period when you have lost your partner and are anxious about funeral costs and future living expenses, tax hits in the hundreds of thousands of yen can come. If you cannot prepare the tax payment funds, in the worst case you may have to give up the remaining home. This is the real face of Japan’s tax system.

Conclusion

Did the bank officer explain the risks in such detail? Probably they only said, “You can be安心.” Their job is to sell loans, not to plan your tax strategy.

Lack of knowledge means being taxed even after death. Readers considering “Joint Survivorship Life Insurance” should not only consider the immediate sense of security but also calculate the tax risks behind it and stamp the contract.

▼ The safest place to keep the cash within your safe asset capacity is here.

https://www.gogojungle.co.jp/tools/ebooks/73546