[Stock Analysis] Management Score 99! Can M3 (2143) break into the core of medical care?

When I go to the hospital, I always think, "Why is the waiting time so long?"

In this era of advanced the Internet, the only communication method with limited response time is the phone. Even after the examination is over, you must wait for the checkout, and only time is consumed. If you catch a new illness in the waiting room during that time, it’s game over.

We see headlines like "there is a shortage of doctors," but just eliminating this inefficiency should significantly improve the situation.

It is not easy to find growth industries in Japan, butthe medical industry is undoubtedly one of the few growing sectors. With an aging population increasing the need for medical care, hospitals are always overflowing with elderly patients.

Alongside medicine, IT is another growth field. With the advent of smartphones, most people now carry computers with them, and the world has changed greatly.

If there are companies that share the growth trajectory of medicine and IT, the growth potential would be substantial. However, perhaps due to regulations, there are few companies that actively tackle the core of healthcare.

Among such field, the one that can be said to be a “one-man winner” isMS& (M3) which operates a medical portal site.

Runs a site registered by 90% of doctors

A company born from Sony, with Mr. Tanimura, a McKinsey alumnus, serving as president since its founding.

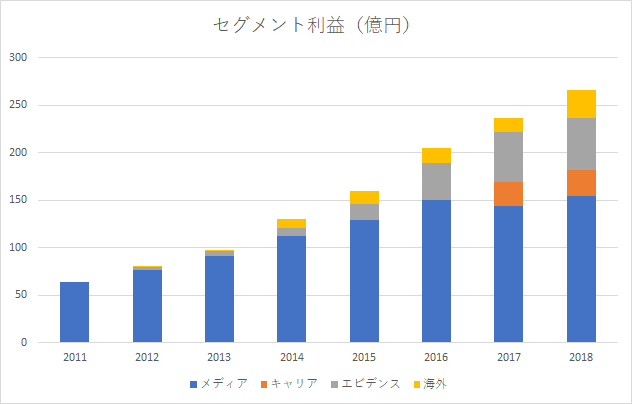

Main revenue sources include running the medical information site “m3.com,” the interaction between doctors and pharmaceutical companies via “MR-kun,” and businesses in clinical trials and medical career services.Among 290,000 doctors in Japan, 260,000 are registered on this site, demonstrating overwhelming strength.

Until now, it has mainly grown through “MR-kun”. “MR” refers to sales staff for pharmaceutical companies, but their inefficiency and the collusion between doctors and salespeople were evident. Internet technology opened a gap, reducing costs, and doctors and pharmaceutical companies found it valuable.

Growth does not stop there. The high costs in the pharmaceutical industryClinical trials (evidence) business and career-support services for doctors, nurses, and other medical professionals continue to expand to related businesses. Growth overseas, including China, is also notable.

Even if the existing businesses plateau, the company is well-positioned to expand into the next fields, maintaining a strong position and management skills learned from McKinsey, so further growth in performance is expected.Career and evidence businesses have just started and will grow further. There are several competitors, so it might not be as advantageous as the media business, but the company enjoys an edge in brand recognition within the industry.

Cloud-based electronic medical records (EMR) draw attention

Business expansion will not stop at this. I am particularly watchingthe EMR field.

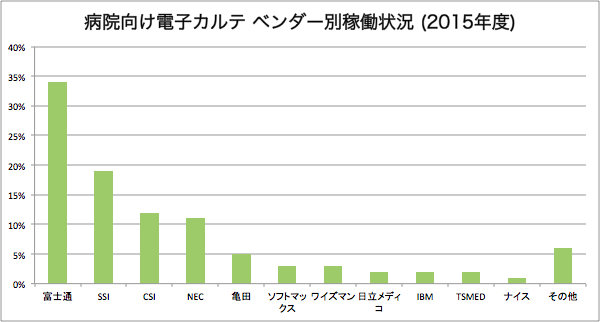

EMRs are handled by several companies, butnone stand out much. Usability and compatibility with other software seem to be the issues. Looking at the lineup of vendors, it leaves an impression similar to public services that are notoriously hard to use.

These services, in a hospital, must coordinate from reception to diagnosis, data storage, and billingto avoid becoming a collection of isolated systems. The current EMR industry seems to have fallen into exactly that situation.

In such a situation,cloudization could make a breakthrough. In the IT industry, cloud adoption has been discussed for a long time, but medicine is no exception.

Cloud reduces implementation costs and effort; as long as you are connected to the Internet, you can use it for a fixed monthly fee. Software updates are automatic, so maintenance is not required.Large-scale software will largely be replaced by cloud-based solutions.

MS& is also paying attention to this area. In 2012, it acquired S.C.M.S. to enter the EMR business and is working on cloud-based EMR “Digical.”Cloud-based EMR already holds the No. 1 share.

Hospital management shares many commonalities, andcloud-based EMR can become a platform. In the future, it may even be possible to share EMRs across different hospitals in an instant via cloud.

MS& is in a favorable position with capability and financial resilience, and could also dominate this field. A full-scale entry into EMRs suggeststhat breaking into the core of healthcare might finally be within reach.

Management gets a 99, but the stock price...

There is no obvious risk at present. Growth has been driven by acquisitions, and goodwill is 38 billion yen, but it remains below half of equity. It is unlikely to become a major problem.From a managerial standpoint, it’s a 99-point company.

Growth companies tend to have high P/E ratios.As of today (February 19, 2019), MS&’s P/E is 52, a high figure. Even if profits are growing, a high P/E means prices can fall with only slight growth deceleration.

A chart illustrates this well so far.Profit has almost doubled in four years, but stock price has hardly risen since last year’s drop. It shows the difficulty of investing in growth companies.

On the other hand, if profits rise but stock price does not, it means the P/E is decreasing. If the price remains stagnant, there may be a chance somewhere.So, there is no doubt it is a good company, and I will continue to monitor its developments.

I will keep an eye on it, as it is a high-quality company.