U.S. Stocks S&P 500 Fixed-Point Observation Week 4 of October 2025

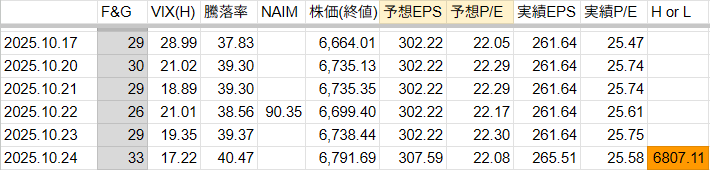

S&P 500 1-week figures

● S&P 500 latest high 6,807.11 (2025.10.24)

S&P 500 FALCON TRADE Weekly Chart October 24, 2025 (Friday)

S&P 500 FALCON TRADE Daily Chart October 24, 2025 (Friday)

The gap opened with a new high. The next bar is a phase to determine whether it will rise or fall. If it gaps down, it becomes a reversal island.

↑ ↑ ↑ The chart isTradingView.Indicators are obtained when you purchase the report below.

Buy at a crash, sell at the top: A trade strategy report to maximize profits (US stocks / Japanese stocks)

S&P 500 Daily Chart Volume October 24, 2025 (Friday)

“New high with decreasing volume” is a signal reflecting investors' caution seen in the late stage of an uptrend, indicating a phase to determine the sustainability of the rise.

↑ ↑ ↑ The chart is moomoo Securities desktop version. TradingView hides index volume, so we check it here.

S&P 500 Individual Stocks Weekly Performance

Buy at a crash, sell at the top: A trade strategy report to maximize profits (US stocks / Japanese stocks) also see

This Week's S&P 500

This week (Oct 20–25) S&P 500 (SPX) generally trended higher. The week began around 6,690 points, supported by favorable corporate earnings and rising expectations for rate cuts. In midweek it rose to the 6,738 area, but profit-taking caused a small pullback.

On Friday the 24th, after CPI data came in softer than expected, rate-cut bets strengthened, risk-on mood spread, and the index rose again, closing at 6,791.69 for the week, an all-time high.

Also, the range between 6,600 and 6,760 remained, but breaking through an important resistance line suggests further upside is possible.

Key drivers this week included expectations for rate cuts due to cooling inflation and solid earnings from tech and financial sectors. As a result, the S&P 500 rose about 2% for the week, making it a strong week overall.

Next Week's Key Economic Indicators & Events

Next week (Oct 27–Nov 1), the main focus in the US will be the FOMC policy decision and the release of the GDP advance estimate. The following are the main events scheduled.

Oct 28 (Tue)

22:00 S&P Case-Shiller Home Price Index (August, year-over-year)

The pace of home price gains is slowing, which could influence interest rates.

Oct 29 (Wed)

3:00 a.m. (Oct 30, Japan time) FOMC policy interest rate decision

Markets broadly expect a 0.25 percentage point cut, with focus on additional easing given softer hiring conditions.23:00 Pending Homes Sales (Sept)

An important indicator of housing market demand.

Oct 30 (Thu)

21:30 Third-quarter real GDP release (annualized QoQ)

Forecast: +3.1% (prev +3.8%). If growth slows, rate-cut expectations may strengthen.21:30 Initial jobless claims (week of Oct 19–25)

Oct 31 (Fri)

21:30 Personal Income and Personal Spending (Sept)

Especially the core PCE price index (Fed’s preferred inflation gauge) is important, expected +0.2%.23:00 University of Michigan Consumer Confidence Index (Final)

Attention on whether consumer sentiment improves.

As above, next week focuses on the FOMC rate decision, GDP release, and inflation-related indicators like the PCE. Markets have largely priced in a Fed rate cut, and the statements could move stocks, currencies, and bonds significantly depending on the content.

Next Week's Major Earnings

Oct 28 (Tue)

Microsoft: Growth in AI and cloud services "Azure" remains stable, with AI-related demand closely watched.

Visa: Consumer spending steady in the Americas and Europe. Cashless payments expansion and recovery in travel are favorable.

Coca-Cola: Latest results beat expectations in sales and profit; pricing power via brand strength has been effective.

GE HealthCare: Demand for imaging and medical devices remains robust; healthcare sector is expected to stay solid.

GM: Focus on progress of EV business and margin trends. Watch for impacts from strikes and price competition.

Oct 29 (Wed)

Meta Platforms: Advertising revenue recovery; AI-driven ad optimization will be key.

Boeing: Risks include delays in aircraft deliveries and rising parts costs. Progress on manufacturing efficiency is watched.

Texas Instruments: Focus is on whether the semiconductor cycle has bottomed; auto demand is expected to help.

Hilton: Global travel demand remains strong, with particular optimism for business travel returning.

ADP: Employment market data services are solid, indicating labor infrastructure health.

Oct 30 (Thu)

Amazon.com: Focus on AWS growth pace and profitability improvement in the retail segment. End-of-year outlook also in focus.

Intel: Progress in AI chips and Foundry strategy will be a key differentiator.

Mastercard: International transaction volume solid; rebound in traveler spending is a positive factor.

Mondelez International: Global demand for chocolate and snacks remains strong; regional pricing strategy is a highlight.

Southern Company: Expected to be viewed positively for electricity demand and progress in renewable investment.

Oct 31 (Fri)

Exxon Mobil: Focus on crude prices fluctuations and refining margins; energy price resilience is supportive.

Chevron: Attention to upstream costs and dividend policy; cash flow stability is key.

AbbVie: How Humira successor drugs are absorbed is a point of interest.

Colgate-Palmolive: Higher everyday product prices continue, and currency effects on overseas sales are being watched.

Bristol Myers Squibb: Focus on progress of new drug pipeline and changes in sales mix.

Next week focuses on technology, payments, and energy sectors. In particular, AI-related indicators for Microsoft and Amazon, and energy giants’ earnings outlook are expected to influence the overall market.