ディズニー好きならオリエンタルランド(4661)だけでなく、ウォルト・ディズニー(DIS)にも注目すべし!

When you think of “Disney” in stock investment, in Japan it is Oriental Land (4661), but of course the original is in the United States,Walt Disney (DIS).

A Solid Foundation as a Comprehensive Media Company

The advantage of Tokyo Disneyland (Orien tal Land) is well known. Since annual shareholder benefits include admission tickets,it is popular among individual investors.

However, this popularity translates into a high stock price,with a PER close to 50 times, which is not a level that value investors typically buy into.

So what should attract attention is the parent company Walt Disney itself.With a PER of 16 times, it is not overvalued on the numeric front. Disney enjoys global popularity beyond Japan, so there is ample “economic moat.”

However,treating Walt Disney as the same as Oriental Land in Japan would miss the point. Oriental Land specializes in operating Tokyo Disney Resort, while the parent Disney is more appropriately described as a “comprehensive media company.”

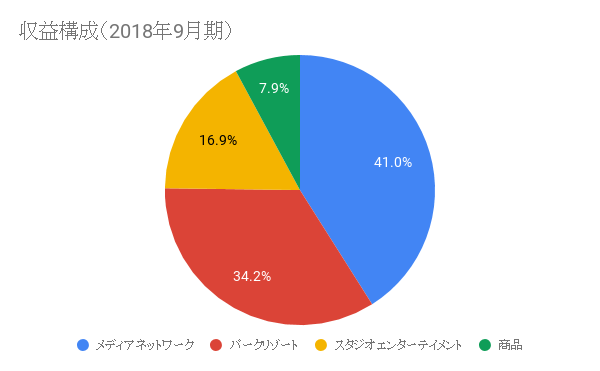

The business segments are categorized into four.

- Media Networks

- Parks, Experiences and Products

- Studio Entertainment

- Consumer Products

The first isTelevision networks operations. In the United States, paid cable TV is common, and the model is subscription-based, charging users fees. It owns stable operations with ESPN (sports channels), Disney Channel, and ABC, providing a solid foundation.

The second isthe operation of Disney Resorts in Florida and California, Paris, Hong Kong, Shanghai. This part is easy to imagine as Oriental Land’s image. Note that it only licenses Tokyo Disneyland; it is not directly involved in its management.

The third ismovie production-centered distribution, DVD sales, paid streaming, and sales to TV networks, among others. They handle both anime and live-action films broadly. Content remains a core part of the company.

The fourth islicense management of Disney goods. It is said that Disney copyrights are strict, and this division governs that aspect.

All four divisions are stable and highly profitable. In each division,operating profit margins range from 22% to 35%, solid.

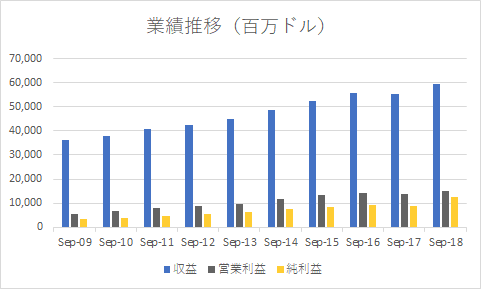

Looking at past performance,the company shows economic resilience, not flinching even during the Lehman Shock.

Industry Reorganization: Netflix in the Eye of the Storm

U.S. media is at a turning point. The eye of the storm isNetflix (NFLX), the Internet video streaming. In the United States, where paid viewing is common, the barrier to paid subscriptions is low, and it has quickly drawn customers away from traditional cable TV.

Existing media have sensed the risk. The integrated media companyTime Warner is being acquired by major telecom AT&T. By colluding between established companies, they attempt to counter the rising power of new entrants.

Disney is no exception. In the first half of 2019, it is expected to acquire21st Century Fox’s content business (movies, TV, cable) for $7.13 billion. This is the plan.

This deal was initially agreed at $52.4 billion, but then media company Comcast proposed a $65 billion acquisition, forcing Disney to raise the bid.

As a result,the acquisition price rose too high, and Disney’s stock price has struggled to gain momentum. The acquisition will be implemented via share swap, leading to new share issuance by Disney and concerns about dilution.

21st Century Fox is also a long-standing media company with solid performance. The acquisition would give Disney and Fox each a 30% stake in the video distribution Hulu, and presumably enable them tocompete with Netflix in online streaming.

Key to the Future: Content

The tension is often framed as existing media versus new media, butthe essence lies in content enrichment.

Netflix is pouring substantial funds into content creation to quickly capture viewers from established media. This trend is unlikely to subside for the time being.

On the other hand, Disney already has content such as Mickey Mouse and various Disney characters.This advantage is not easily shaken. Once released, a certain number of hits are expected, and the cost-effectiveness is immense.

Disney’s enormous revenue could be directed toward strengthening film and resort content and overseas expansion, especially in China, to sustain growth. Note that overseas earnings are still only about 20–30% of total.

Entertainment has no end in the market and is easy to expand geographically;the sweeter the industry when the world becomes more prosperous and peaceful, one can say.

A concern is that new entrants may engage in price competition, but given the enormous cost of content creation, there may not be much room for price cuts. Even if prices are lowered,there is little incentive to discount Disney’s content.

That said, if the acquisition dilutes Disney’s share, Disney could be pulled into price competition outside Disney segments.How to manage a diversified content portfolio is a test of management skills.

Although the internet brings volatility,there is a solid “economic moat,” strong resistance to downturns, and ongoing potential for expansion.It may not be a bad idea to monitor for an appropriate buying timing.